Jewellery Insurance: How to Guard Your Gems

From engagement rings to luxury watches, here's everything you need to know about jewellery insurance.

From engagement rings to luxury watches, here's everything you need to know about jewellery insurance.

Jewellery insurance protects your valuable items, from engagement rings and wedding rings to luxury watches and family heirlooms, against theft, loss, and damage. Whether it’s through your existing home insurance policy or standalone jewellery insurance, the right cover ensures you won’t be left out of pocket if something happens to your most treasured pieces.

At a glance

At a glance

If you own diamond rings, earrings, pearl necklaces, or precious family heirlooms, jewellery insurance is worth serious consideration. For most people, the starting point is their home insurance policy, which covers jewellery as part of your contents insurance up to £2,000 per single item.

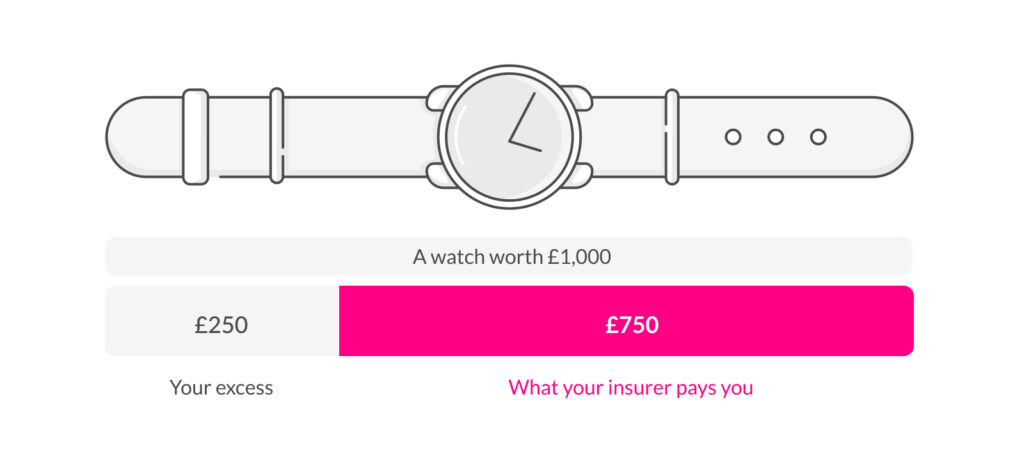

Here’s how the single-item limit works in practice:

If your luxury watch is worth £1,000 and you have a £250 excess, your insurer will pay you £750 (the replacement value minus your excess). But if your watch is worth more than the £2,000 single-item limit, you’d be left covering the shortfall yourself.

If your pieces are worth more than that, you can add high-value items to your existing home insurance policy for fuller protection. And if you own an extensive jewellery collection or multiple high-value pieces, a standalone jewellery insurance policy from a specialist insurance provider may be the better option.

Consider the sentimental value too. Whilst insurance companies can replace the financial value, they can’t replace the memories attached to a treasured bracelet or a carefully chosen engagement ring. Having proper jewellery insurance cover means you can afford to replace what’s lost without the added financial stress.

Jewellery insurance covers virtually any valuable items, including:

Watch insurance is particularly important for luxury watches, which can be expensive to repair or replace. Some insurance providers offer specialist watch insurance as part of broader jewellery insurance cover.

The cover you get depends on which route you take. Here’s a breakdown of both:

| Home insurance policy | Standalone jewellery insurance | |

|---|---|---|

| Theft and burglary | ✓ | ✓ |

| Fire and smoke damage | ✓ | ✓ |

| Flood and water damage | ✓ | ✓ |

| Accidental damage | ✓ With add-on | ✓ |

| Accidental loss | ✓ With add-on | ✓ |

| Worldwide cover | ✓ With add-on | as standard |

| Single-item limit | Up to £2,000 | No limit |

| High-value items cover | ✓ With add-on | as standard |

Most jewellery insurance policies, whether through your home insurance policy or a standalone jewellery insurance provider won’t cover:

The exact level of cover depends on whether you choose to add jewellery insurance to your home insurance policy or opt for specialist insurance from a dedicated provider.

For most people with one or two valuable pieces, adding high-value items to an existing home insurance policy is the most straightforward option. Standalone jewellery insurance from a specialist insurance provider is worth considering if you own multiple high-value pieces or an extensive jewellery collection.

Contents insurance starts at £4/mo, but your price will vary depending on several factors, including:

As a rough guide, jewellery insurance typically costs between 1-3% of the value of the item annually. So insuring engagement rings worth £3,000 might cost £30-90 per year. When getting an insurance quote, insurance companies will consider the replacement value of each piece of jewellery. Luxury watches and high-value jewellery will naturally cost more to insure than everyday pieces.

For high-value items worth over £2,000, most insurance companies require a professional jewellery valuation. Here’s what you need to know:

A professional jewellery valuation should contain:

Visit a qualified jeweller or professional valuer for your jewellery valuation. Avoid getting valuations from the same jeweller who sold you the piece, as they may overestimate the value of the item.

Coverage typically extends to:

If you live with a partner who isn’t your spouse, you may need to add them as an additional insured person or they should get their own jewellery insurance policy.

Download the Lemonade app, answer a few quick questions from AI Maya, and you’re covered. Your contents insurance automatically includes personal possessions like jewellery up to the single-item limit.

Lemonade also offers 14 days of temporary cover whilst you gather your documentation, so you’re not left exposed whilst the paperwork is being sorted.

The claims process with Lemonade is straightforward. If something happens to your jewellery:

Most Lemonade claims are assessed quickly, and if approved, payment goes straight to your bank account. Insurance companies will either replace your piece of jewellery with an equivalent item or pay out the replacement value in cash, minus any excess.

Your standard home insurance policy covers jewellery up to the single-item limit — which means expensive engagement rings, luxury watches, and heirlooms may not be fully protected. For most people, adding high-value items cover to an existing policy does the job. For larger jewellery collections, standalone jewellery insurance from a specialist insurance provider is worth exploring.

Whatever route you choose, make sure you have a current jewellery valuation, and consider adding worldwide cover and accidental loss protection if you wear your pieces regularly.

Ready to protect your precious pieces? With Lemonade, you can get a quote in as little as 90 seconds.

Standard travel insurance typically includes limited cover for valuable items. For expensive jewellery collections, worldwide cover through your main jewellery insurance policy is usually better.

Yes, heirlooms and antique items of jewellery can be insured. You’ll need a professional valuation to establish the current replacement value, as sentimental value isn’t covered by insurance companies.

Home insurance includes basic contents cover for personal possessions, but there’s usually a single-item limit of £1,000-£2,500. High-value jewellery needs additional high-value items cover.

Most insurance providers require jewellery valuations to be updated every 2-3 years to reflect current market values.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.