What Does Home Insurance Cover?

Keeping your home and belongings covered from disaster.

Keeping your home and belongings covered from disaster.

Home insurance covers your home, belongings and even liabilities, protecting you from unexpected events like fire, flooding, theft, and storm damage. It’s designed to give you peace of mind, knowing that your property and possessions are safeguarded.

Let’s break down exactly what home insurance covers, and which type of cover you need.

TL;DR

TL;DR

Home insurance policies typically have 4 main categories of cover.

Both buildings and contents insurance are the two main types of cover on a home building insurance policy, and protect you against specific circumstances, known as designated perils, which include theft, fire, vandalism, certain types of water damage, and many other inconvenient incidents and circumstances.

The key difference lies in what each policy is designed to cover.

| Buildings insurance | Contents Insurance |

|---|---|

| Walls, roofs, and floors | Furniture, clothing, and jewellery |

| Fixed installations like bathrooms and kitchens | Home electronics like TVs, laptops, and mobiles |

| The structure of outbuildings such as sheds and garages | Items stored in outbuildings like tools and gardening supplies |

If covered perils (like fire, water damage, burglary, etc.) cause your home to become unlivable, your home building insurance policy will cover the cost of alternative accommodations, like a hotel stay, and other expenses, possibly including any extra cash you need to spend on your own food and laundry.

Home building insurance covers both personal liability and property liability.

Remember, if you want to really extend your personal liability cover, you can supercharge your policy with Legal Protection cover. (More on this later)

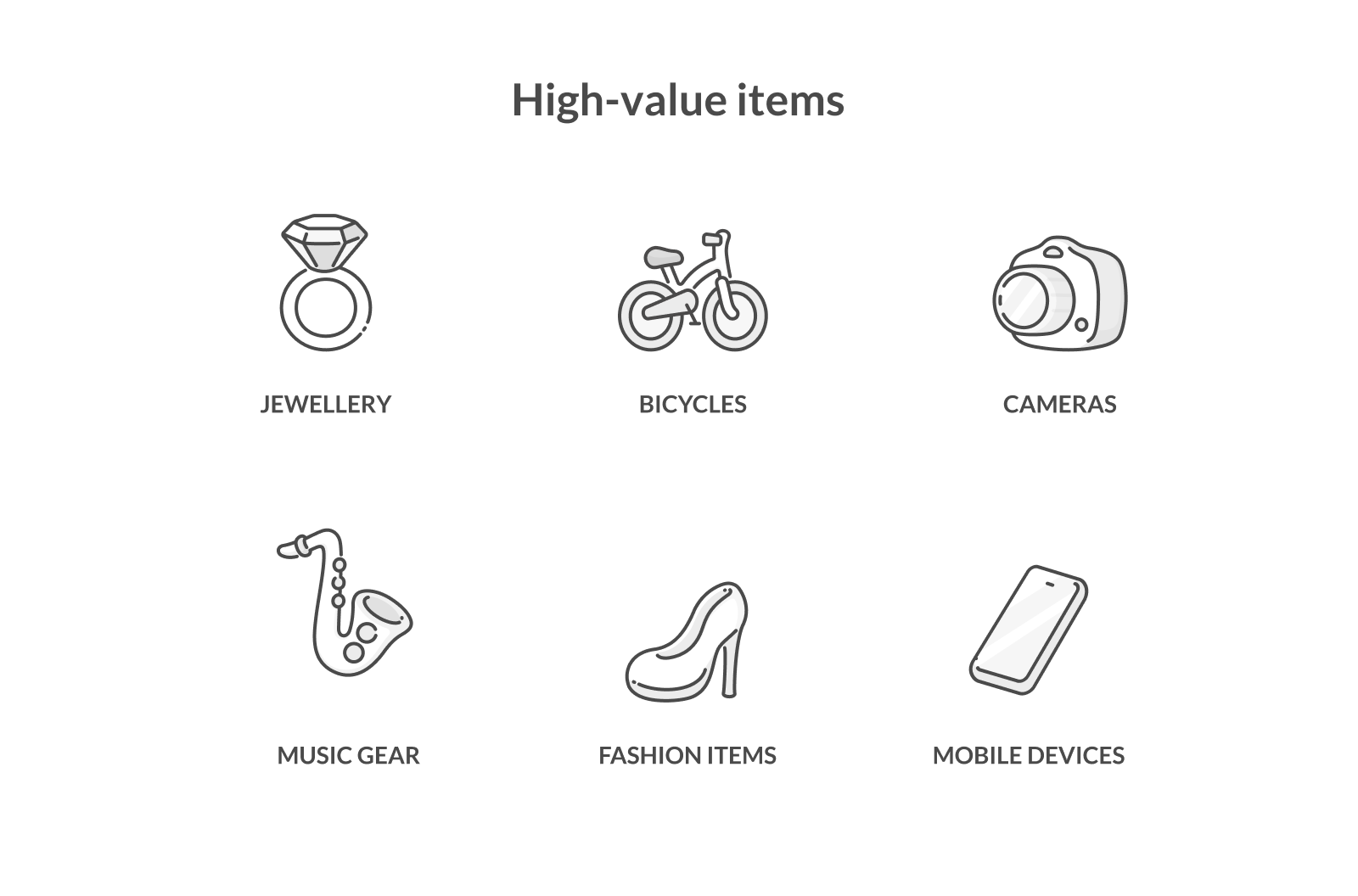

If you own valuable items worth over £2,000 each, they’re also covered by your contents insurance—but you’ll need to add some additional cover for your high-value items in your insurance policy to make sure they’re protected for their full value. In insurance terms, that’s known as adding scheduled personal possessions cover.

For a slightly extra cost, you can add additional cover for your high-value items, including:

A lot of these items might already have a cover of £2K on your base policy—but scheduling your high-value items increases the amount of cover above £2K, up to the full worth of the item. If you want to protect your high-value items for most eventualities, you’ll want to increase your cover with some optional extras.

Some home insurance policies allow you to include add-ons for a more tailored level of protection. At Lemonade, the following optional extras are available for all customers:

Homeowners enjoy the same add-on cover options as tenants, with the added benefit of two additional cover choices:

Remember, these add-ons often incur extra costs, but they can deliver unparalleled peace of mind.

Most home insurance policies will not cover any damages caused by these common exclusions:

Some policies also have a single-item limit, meaning extraordinarily valuable items (like heirloom jewellery or art) might require separate insurance. Always check your policy documents for exclusions and limits to avoid surprises.

The type of home insurance you need depends largely on whether you own or rent your home.

If you own your home, buildings insurance is highly recommended—and often mandatory if you have a mortgage. Adding contents insurance to the mix by purchasing a home building insurance policy will provide full protection for both your property and possessions.

If you’re a tenant, you don’t need buildings insurance, as that’s your landlord’s responsibility. However, contents insurance is ideal for protecting your personal belongings. Some providers even offer renters-specific insurance policies tailored for tenants.

Home insurance provides not just financial protection, but also invaluable peace of mind. Knowing that you’re covered when life happens can make all the difference. By choosing the right combination of contents insurance, buildings insurance, and add-ons, you create a safety net tailored to your needs.

If you’re ready to simplify the process, get a home insurance quote today.

Most home insurance policies cover specific natural disaster events like storms, flooding, and earthquakes, but cover can depend on your location and policy terms.

For example, if you live in a high-risk flood area, you may need to pay higher premiums or purchase additional cover. It’s important to review what’s defined as a “covered event” in your policy to avoid surprises.

Home insurance generally covers water damage caused by sudden and unexpected events, such as burst pipes, heavy rain, or accidental leaks. However, it usually won’t cover damage resulting from neglect, gradual wear and tear, or unresolved maintenance issues like long-term dampness. Always check your policy details as cover can vary by provider and policy type.

To claim on your home insurance policy, contact your insurer as soon as an incident occurs. Provide details of the damage or loss, along with any supporting evidence like photos, receipts, or a police report if applicable. Your provider will guide you through the claims process and may send an assessor to evaluate the damages.

Home liability insurance covers the costs if someone is injured or their property is damaged while on your premises, and you are found legally responsible.

This could include medical bills, legal fees, or repair costs for incidents like a guest’s injury from a fall. Check your policy to see the limits and specific situations it covers.

Standard home insurance doesn’t cover damages caused by lodgers or their belongings. You may need to inform your insurer and adjust your policy to account for having a lodger, as it could involve additional risks. Failing to notify your provider may invalidate your cover, so it’s essential to discuss this with them in advance.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.