What is Contents Insurance?

From theft to personal liability, get to grips with your policy.

From theft to personal liability, get to grips with your policy.

Contents insurance offers you financial help if your belongings are stolen, damaged, or lost. It provides financial protection for your possessions, giving you peace of mind if an unexpected event happens.

We’ll walk you through how contents insurance works, what it does (and doesn’t) cover, and how to determine if it’s right for you.

At a glance

At a glance

If your belongings get nicked, damaged, or ruined by something like a fire or burst pipes, you can make a claim on your contents insurance. Your insurer will check if what’s happened is covered by your policy and sort out how much they’ll pay to fix or replace your things.

You’ll usually have to chip in a bit towards the claim, known as your insurance excess. This is an amount you decide when you take out the insurance-usually somewhere between £100 and £500-that will be subtracted from any future claim payouts.

BTW: Home insurance is the term for both contents insurance and buildings insurance together-but they’re always sold as separate cover. So, contents insurance can protect you as a renter and as a homeowner.

A typical contents insurance policy (also sometimes known as home contents insurance) has three main categories of cover:

Let’s take a close look at each.

The main sub-category of your contents insurance policy, is also called contents. This first part of your cover helps you recover the cost of damaged or stolen property if various unpleasant or unexpected things happen. That includes nearly all of your personal belongings including:

If covered perils (like fire, water damage, burglary, etc.) cause your place to become unliveable, your contents insurance policy will cover the cost of alternative accommodations, like a hotel stay, and other expenses, possibly including any extra cash you need to spend on your own food and laundry.

Contents insurance cover extends to instances in which you are liable for causing damage or injury to someone else-called personal liability cover, whether that means repairing or replacing a damaged item, or covering hospital bills or legal expenses from a lawsuit.

It also extends to certain damages that you may cause when you’re abroad for trips or away from home (of up to three months)-such as if you accidentally injure your mate while on holiday. We also cover damage you may cause to your rental home and your landlord’s stuff, but this doesn’t extend to normal wear and tear like scratches or stains. Remember, if you want to really extend your personal liability you can supercharge your policy with Legal Protection cover. (More on this later)

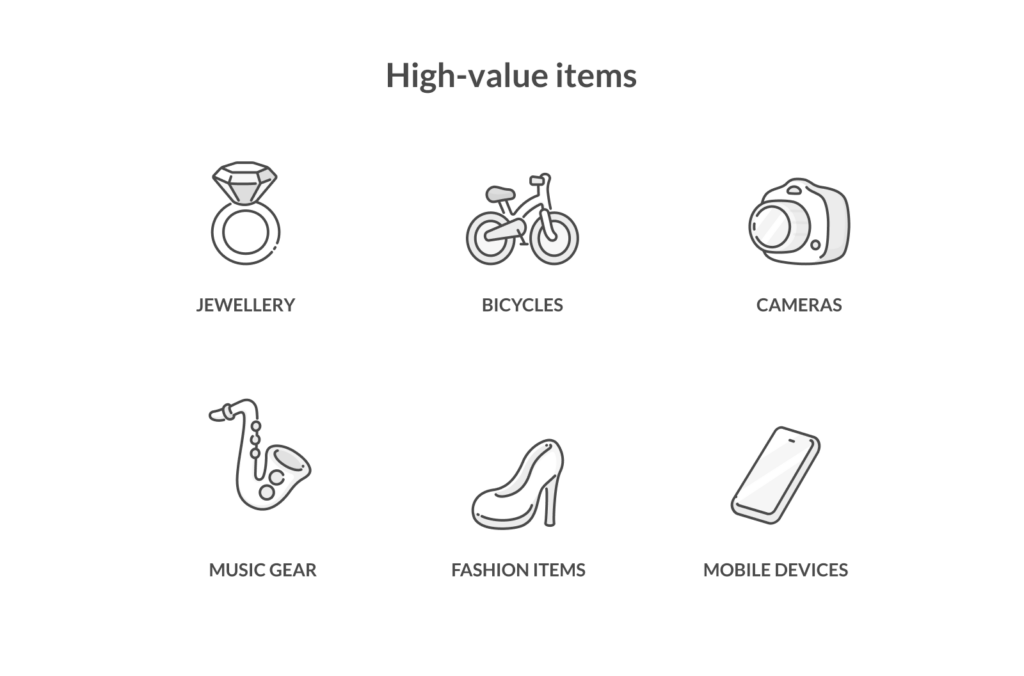

If you own valuable items worth over £2,000 each, they’re also covered by your contents insurance-but you’ll need to add some additional cover for your high-value items to make sure they’re covered for their full value. In insurance terms, that’s known as adding scheduled personal possessions cover.

For a slightly extra cost, you can add additional cover for your high-value items, including:

A lot of these items might already have a cover of £2K on your base policy-but scheduling your high-value items increases the amount of cover above £2K, up to the full worth of the item.

Adding this additional cover is simple, and can be done via the Lemonade app. High-value items can be added to your policy for an additional cost, though they may require appraisals or proof of purchase.

But don’t forget, if you want to protect them for most eventualities you’ll need to bolster your coverage with optional extras.

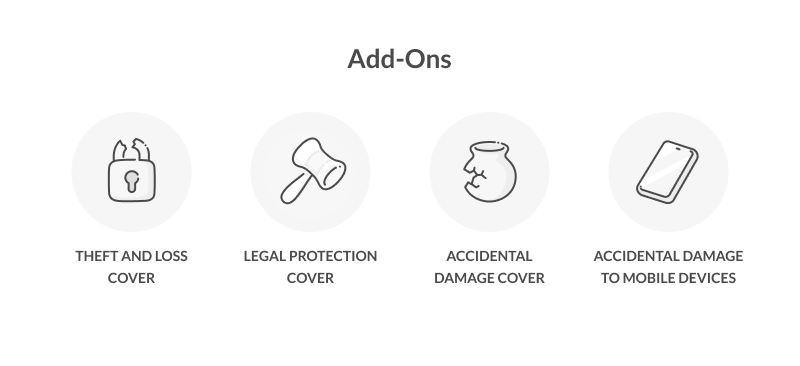

Add-ons are optional extras that can be applied to your base policy, giving you extra cover in the event of specific circumstances. At Lemonade, we offer four available add-ons for tenants:

On your base policy you’re covered for straightforward cases of robbery or burglary inside your home. But with Theft & Loss cover your stuff is also covered against theft and accidental loss inside and outside your home, as long as you’ve taken reasonable care to protect it.

So, if your mobile phone or your bicycle gets stolen or lost outside your home, you’re covered. (Just remember not to leave your phone unattended, and to lock up your bicycle with a high quality chain or U-lock, otherwise your claim might not be covered).

Another great perk of this cover is you’re also covered if your house keys are lost or stolen. If this happens, we’ll cover the necessary costs to replace the locks or keys.

Adding Legal Protection cover gives your policy an extra layer of security, going beyond the personal liability coverage in your base policy. For instance, we’ll provide legal protection in case of disputes related to personal injury, your home, your employment, consumer agreements and clinical negligence causing you injury.

Adding Legal Protection cover gives your policy an extra layer of security, going beyond the personal liability coverage in your base plan.

The accidental damage add-on covers your stuff against damage that is sudden and unexpected, even if it’s your fault. So let’s say you accidentally spill coffee on your brand new rug or knock over your TV-you’d be covered. The only catch is this cover doesn’t apply to your mobile devices or gadgets, like your smartphone, laptop or tablet.

We partner with BeValued, who will actually come pick up your damaged mobile device and repair it using only original parts. What if your device needs to be replaced? Smartphones will be replaced with a refurbished, Grade A (mint condition) mobile. All other devices will be replaced as-new.

Homeowners with a contents-only insurance policy from Lemonade can enhance their coverage by adding our home emergency cover. This cover provides a 24/7 emergency helpline to assist with urgent issues like a broken boiler, electrical failures, or even if you’ve lost your house key. Keep in mind, that this cover is not available for tenants.

The price of contents insurance is more affordable than you might expect, with policies starting at just £4 a month. Your premium depends on factors like the value of your belongings, the coverage amount you choose, the excess you choose, and any optional extras you add, such as Accidental Damage or Legal Protection.

Determining how much contents insurance you need depends on the value of your belongings. Follow these steps to calculate:

Every insurance policy has its exclusions, so it’s essential to read the fine print. Here’s what’s typically not covered:

Always confirm policy exclusions listed in your policy documents.

No, contents insurance is not legally-mandated, but it’s highly recommended for most households. Here’s some scenarios:

If you own your home, you may already have home insurance, which typically combines buildings and contents insurance. While buildings insurance covers the structure of your home, contents insurance protects your belongings inside.

Since renters don’t need buildings insurance (that’s the responsibility of your landlord), contents insurance for renters ensures your possessions, like furniture and gadgets, are protected.

For those living in shared accommodation, a typical policy may not cover belongings owned by other housemates. You’ll need individual policies or a special clause that covers everyone’s belongings.

Insurance may not stop fires or theft, but it provides a financial cushion if the worst happens. By getting contents insurance tailored to your needs, you can rest easy knowing your belongings are protected.

Take the first step, and get a quote with Lemonade today.

If you fail to declare items worth more than your policy’s single-item limit, they may not be fully covered in the event of a claim. It’s a good idea to always schedule your high-value items to ensure adequate protection.

Contents insurance usually covers you, your partner, and anyone living with you, such as children or close relatives, as long as they’re named on your policy. Housemates can be included too, but many policies limit this to four people in total.

If your kids go off to uni but lived at home beforehand, their belongings might still be covered under your policy if they’re still registered at home, and living in student halls of residence. For others, like cousins or friends, getting separate insurance is often a better choice to ensure everyone’s things are properly protected.

No, most contents policies do not cover damage caused by pets, such as scratches on furniture or chewed items.

No, contents insurance typically does not cover items you’ve borrowed from friends or rented. These items remain the responsibility of their owner or may require separate insurance.

If you underestimate the value of your possessions, your insurer won’t pay the full replacement cost in the event of a claim. For instance, if your items are worth £20,000 but your policy covers £10,000, the maximum payout you could receive in the event of a claim is £10,000.

It’s important to accurately calculate the value of your items to avoid being underinsured.

Yes, most providers allow you to declare and add high-value items to your policy as your belongings change. At Lemonade, you can manage your cover at any time on the Lemonade app.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.