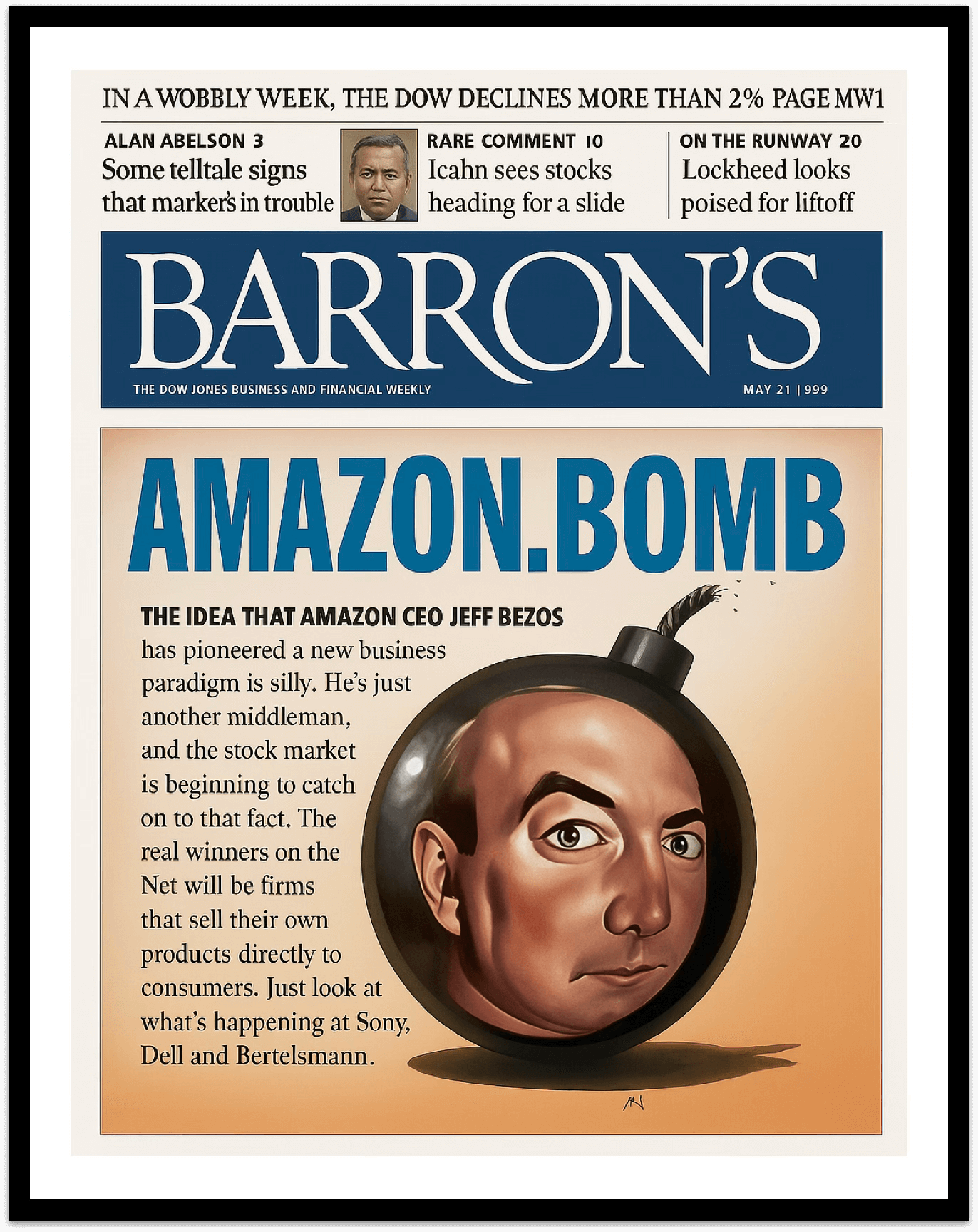

On a wall in my home office hangs the May 1999 cover of Barron’s — the foremost financial weekly — emblazoned with the headline: AMAZON.BOMB. The article confidently assured readers that “once Wal-Mart decides to go after Amazon, there’s no contest.”

Barron’s got one thing right: there was, indeed, no contest. Amazon is now worth over a trillion dollars more than Walmart. And Walmart survived the retail apocalypse better than any other incumbent. Borders, Brooks Brothers, Circuit City, J.C. Penney, Kmart, Lord & Taylor, Neiman Marcus, RadioShack, Rite Aid, Saks Fifth Avenue, Sears, and Toys “R” Us all filed for bankruptcy.

The AMAZON.BOMB fallacy is wired into our psychology. Kahneman called it WYSIATI — “What You See Is All There Is”. It leads us to focus on the visible feature (a behemoth retailer vs a mere website) while ignoring the submerged architecture of incentives, culture, and systems. WYSIATI explains why — overwhelming evidence to the contrary notwithstanding — the AMAZON.BOMB fallacy lives on. I encounter it almost daily in some variation of: “I saw a press release saying State Farm is doing something interesting with OpenAI. Surely it’s only a matter of time before Lemonade’s lead disappears?”

No, it isn’t.

The Triceratops’ Problem

Sears could launch a website. State Farm can license AI. But companies who slap technology on top of their legacy businesses are not changing their DNA: their incentives, capital allocation logic, talent mix, data architecture, distribution dependencies, brand promise, investor expectations, and legacy stacks. Those systems and processes co-evolved over many decades. They cannot be reengineered piecemeal; and untangling them is laborious and risky.

Given enough time everything is possible. An amoeba can evolve into a Triceratops. A Finnish pulp mill can evolve into Nokia, the world’s leading phone manufacturer. But when change arrives at meteoric speed, dinosaurs — literal or corporate — struggle to adapt.

For these reasons market leadership has shifted every time a substrate changed.

| Industry | Incumbent | New Dominant |

|---|---|---|

| Retail | Sears / Walmart | Amazon |

| Photography | Kodak | SanDisk |

| Mobile | Nokia / BlackBerry | Apple |

| Video | Blockbuster | Netflix |

| Music | Tower / HMV | Spotify |

| Taxis | City monopolies | Uber |

| Enterprise software | On-prem vendors | Salesforce |

In each case, the technology was visible and accessible. Incumbents invested. Analysts cheered. Press releases said all the right things. And yet leadership reordered.

It’s not that incumbents were oblivious. It’s that they were maladapted.

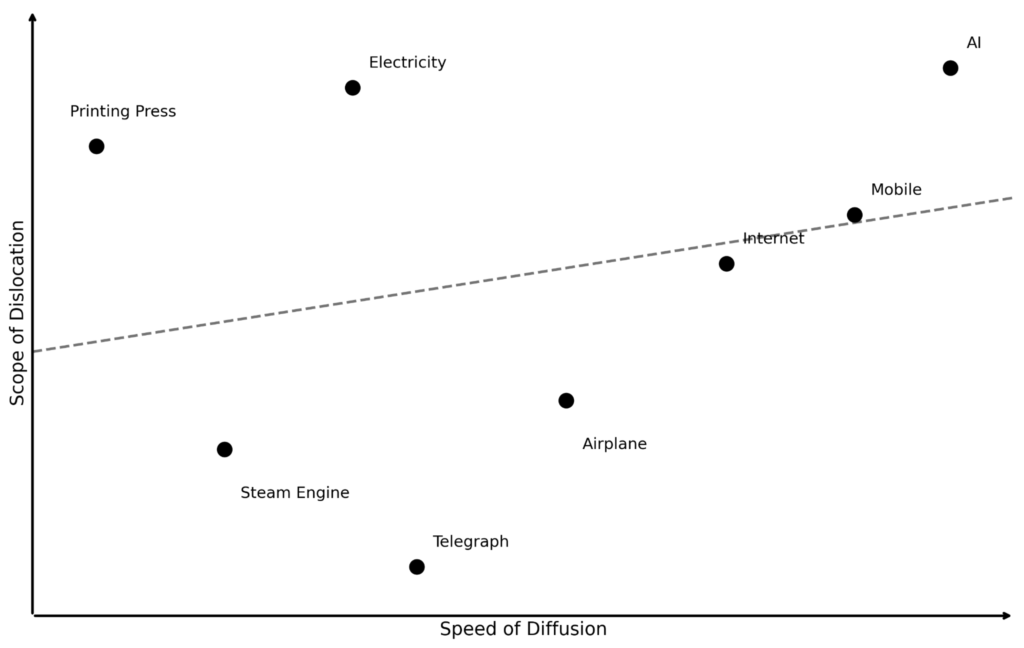

And the speed of diffusion and scope of dislocation of all prior technology revolutions, pale next to what’s coming next.

Which brings us to insurance and AI.

Optimized for Yesterday

Fourteen of the Fortune 100 are insurance companies. Their average age is over a century — far older than the Fortune 100 norm. No industry is more deeply optimized for the world as it was. And no prior technology revolution has matched AI’s combination of speed and scope. The most entrenched industry is about to meet the fastest substrate shift in history.

Lemonade did not begin as an insurance company that adopted AI. We began as an AI-native company that entered insurance. That distinction shaped every layer of our architecture — from data to expenses to talent.

The result is a different cost structure. A faster clock speed. A compounding feedback loop that continuously improves underwriting, customer experience, and efficiency.

The question, then, is not whether incumbents can “use AI.” Of course they can. And they should. The question is whether they can re-architect themselves to close the gap to Lemonade.

That seems unlikely.

For one, it’s not clear that they particularly want to. At Berkshire Hathaway’s annual meeting this year, Ajit Jain — who oversees Berkshire’s insurance operations, including GEICO — described their approach to AI as “wait and see.” The individual operations “dabble” with AI, he said, but there has been no “conscious big-time effort.”

State Farm went so far as to run a national, star-studded, TV campaign mocking claims bots, and apparently Lemonade specifically.

And these attitudes are not unusual. A Munich Re survey of global P&C executives found that most are holding back meaningful AI investment “until the ROI is clearer.”

That is the Triceratops speaking — not from the outside looking in, but from the corner office looking out.

Even once insurance CEOs start singing a different tune — and some already are — incumbents remain inherently encumbered. Adoption of new technologies is constrained by channel conflicts, cultural inertia, legacy systems, and existing commitments. Beyond ambivalence lie some hard truths: GEICO — according to Jain — operates “more than 600 legacy systems that don’t really talk to each other.”

But here’s the really crazy thing: even if they could magically transform every system, person, contract, and cultural norm in their industrial complex — and nothing short of magic would suffice — the gap between us and them would still widen rather than collapse.

It’s physics.

If two objects accelerate at the same rate but one began earlier, the leader’s lead does not shrink over time — it grows.

AI vs BS

Hoverflies have evolved to mimic wasps. They wear the same yellow-and-black livery, adopt the same silhouette, even imitate the same darting flight. But beneath the surface, their anatomy is entirely different and they have no sting.

This is Batesian mimicry. It works because it exploits the WYSIATI fallacy. When a harmless species signals, “I’m a wasp — look at my stripes,” much of the ecosystem goes along. What you see is all there is.

In nature, the predators who thrive are the ones able to look beyond the stripes. In markets, it’s the investors who look beyond the press releases. The difference between AI and BS is not found in the rhetoric. It’s reflected in the numbers.

Whether or not AI is truly powering an insurer’s operations shows up in three unhidable ways — all measurable from public filings. (Though definitions are not consistent across carriers, they are consistent across years, so trends are unambiguous.)

The first two measure whether AI is doing the work. The third measures whether the work is getting smarter. Any one result, in isolation, can be explained away — by line mix, market cycles, or cost-cutting. But when all three move in concert, the alibis cancel out. The signal is structural.

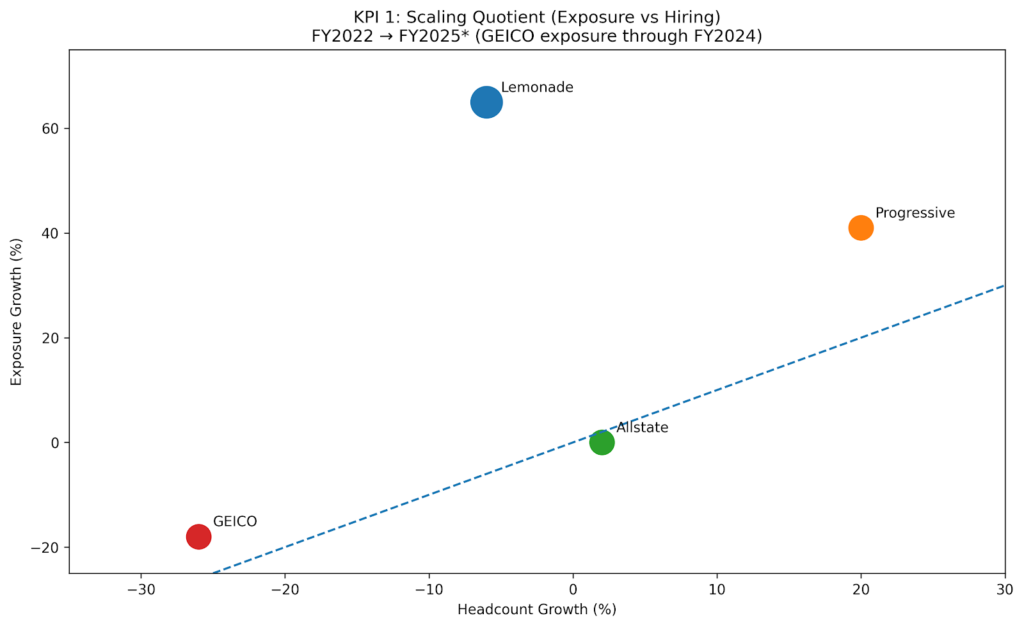

1. The Scaling Quotient

This tests whether the company can grow without adding people:

Customer (or Policy-in-Force) Growth ÷ Headcount Growth

From FY2022 — the last full year before generative AI entered the mainstream — to FY2025:

- GEICO: Exposure declined materially while headcount fell roughly 26% — retrenchment.

- Allstate: Exposure was roughly flat while headcount increased modestly — premium growth largely reflected repricing.

- Progressive: Exposure grew about 41%, while headcount rose roughly 20% — growth accompanied by material hiring.

- Lemonade: Exposure grew roughly 65% while headcount declined — scaling without hiring.

Expressed as a quotient: Lemonade’s scaling is effectively unbounded. Progressive’s is positive but finite. Allstate’s is near zero. GEICO’s is negative — retrenchment, not leverage.

The more of an operation is powered by AI, the more growth decouples from labor. If growth requires proportional hiring, AI is ornamental.

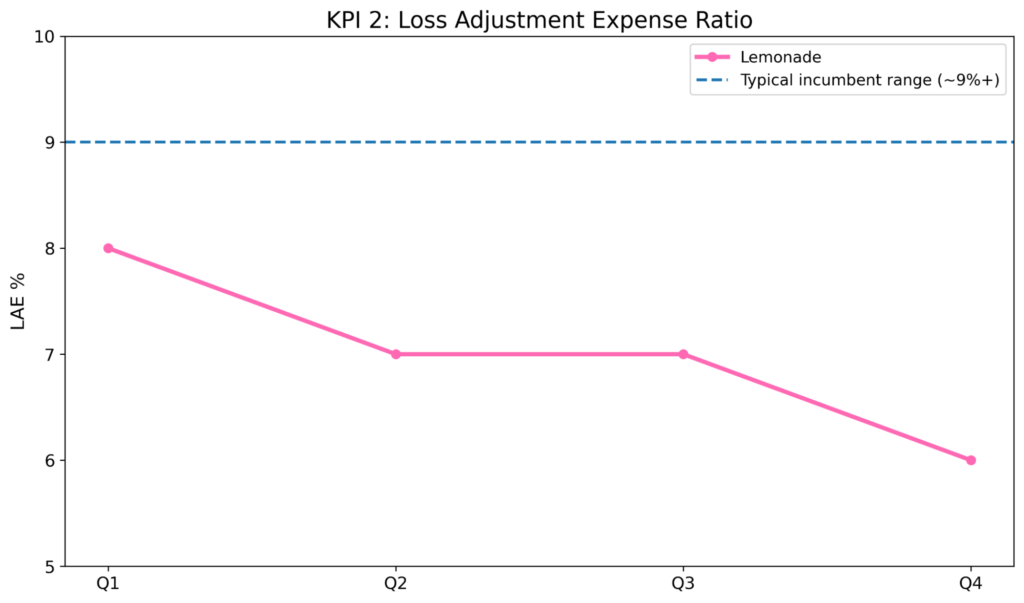

2. Loss Adjustment Expense Ratio

This tests how expensive it is to run the insurance machine:

Loss Adjustment Expense ÷ Gross Earned Premium

LAE measures the bureaucracy of claims — the mechanical heart of insurance. For large incumbents, LAE typically runs in the high single to low double digits depending on line mix.

At Lemonade it is 6% and falling – best in class and getting better – despite Lemonade being subscale.

If claims volume scales and LAE scales with it, AI is cosmetic. If claims volume scales and LAE compresses, that’s AI’s signature.

And if lower cost meant worse service, complaint rates would rise. In Texas — one of the few states publishing confirmed complaint incidence by insurer group — Lemonade’s complaint rate per policy sits materially below the largest incumbents. Cost compression without service degradation is AI.

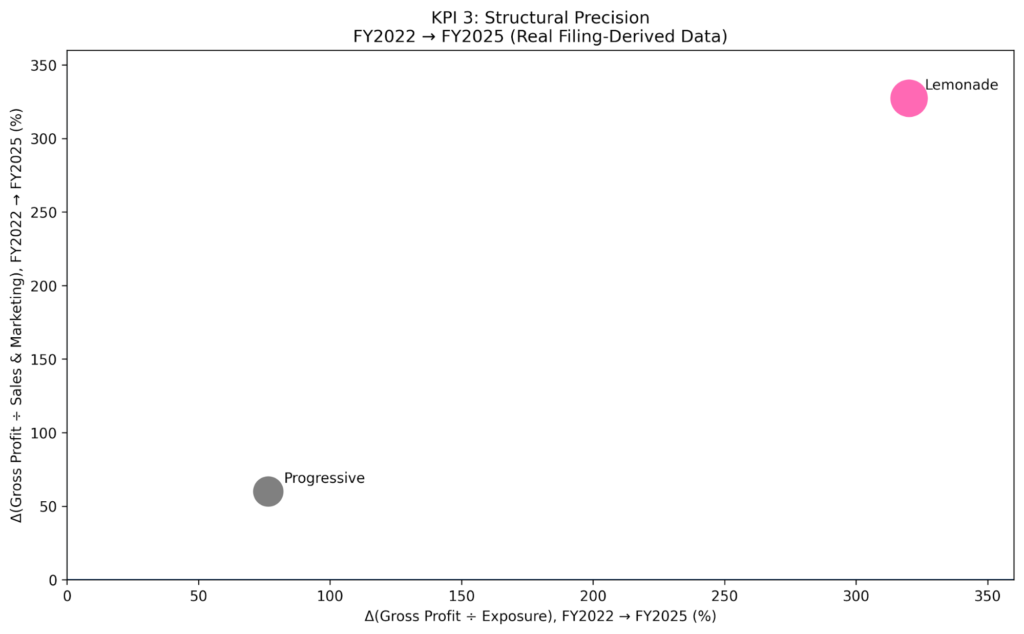

3. Structural Precision

This tests whether the business is becoming economically smarter over time:

Δ(Gross Profit ÷ Exposure) + Δ(Gross Profit ÷ Sales & Marketing)

The sum captures total economic intelligence — how much smarter the system is getting at both making and finding money. If AI improves underwriting precision — tighter segmentation, smarter elasticity management, fewer mispriced risks — gross profit per exposure should rise over time.

But precision does not require timid pricing. In segments where AI identifies mispriced opportunity, deliberate price leadership may compress gross profit per exposure temporarily. In those cases, acquisition efficiency should improve materially.

The test, therefore, is not whether both rise every period. It is whether the net effect is positive.

- If both metrics deteriorate, growth is being bought.

- If one softens but the other strengthens sufficiently, capital is being allocated intelligently. The greater the quantum of intelligence the greater the signature of AI.

From FY2022 to FY2025:

- Progressive: +76% improvement in profit per exposure, and +60% improvement in profit per acquisition dollar — roughly +137 points combined.

- Lemonade: +320% improvement in profit per exposure, and +327% improvement in profit per acquisition dollar — roughly +648 points combined.

Bottom line, look past the stripes. These three KPIs are calculable from public disclosures. Apply them to any insurer that claims AI is transforming its business — including us — and let the numbers speak for themselves.

The Singularity

On my wall, beside Barron’s AMAZON.BOMB, hangs Time’s cover from 2011, entitled 2045. That’s the year futurist Ray Kurzweil predicts the “Singularity” — the point beyond which prediction breaks down and we enter uncharted territory.

A fair question, then: does any of the above analysis survive a world where superintelligent AI can rewrite legacy systems overnight? If a country of geniuses lives in a data center, can’t they just fix GEICO’s 600 systems over a weekend?

Perhaps. AI can certainly rewrite code. But then, so could an army of engineers at any point until now. The incumbent problem was never just technology. The 600 systems exist because of the incentives, history, and organizational dynamics that created them. AI cannot rewrite a board, a distribution network of captive agents whose livelihoods depend on the old model, or a CEO’s risk appetite. The immune system of a large organization will resist transformation even as AI gets more powerful — especially as it gets more powerful, because the disruption to existing humans and structures becomes more threatening, not less.

Things will get frenetic as we approach the Singularity. That’s fine by us. As we wrote in our Founders’ Letter, “We wouldn’t know how to shepherd incumbents through these momentous changes; nor do we know of a technological solution to their innovator’s dilemma.” Lemonade, on the other hand, was engineered for “uncharted territory…we have state-of-the-art kit, an intrepid team, an ambitious destination, but no map.”

Confidently predicting what happens after predictions break down is a fool’s errand. But ignoring the historical record and today’s structural asymmetry is foolish too.

Incumbents were designed for the world as it was. We were designed for the world as it’s becoming. That’s not a boast. We’re no smarter or more worthy. But it is a load-bearing fact.

LEMONADE.BOMB