What do student loans have to do with national defense? Everything.

Student loans were initially created to bulk up the number of American math and science experts after Russia orbited a satellite in the sky before the US.

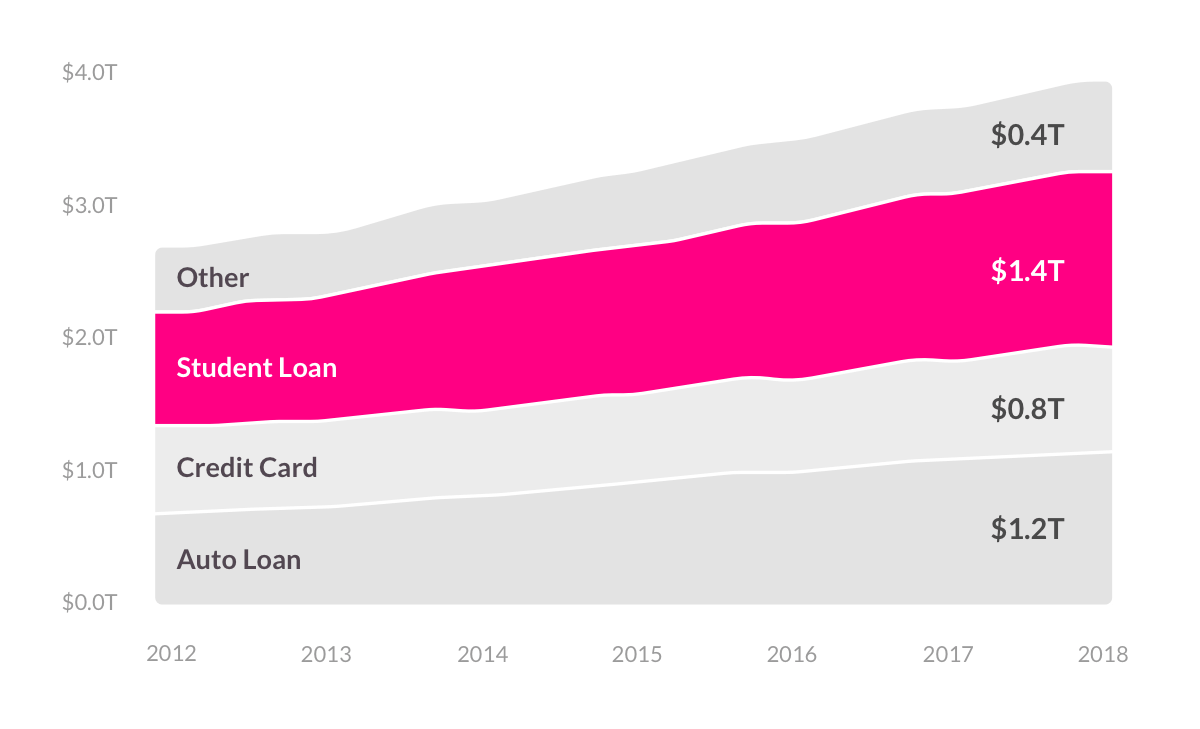

Several moon landings later, things with Russia are still pretty tense, but the amount of student debt has become nothing short of astronomical. It’s gotten so bad that in 2019, the Federal Reserve reported that national student loan debt had crept up to nearly $1.6 trillion!

Student loans are crippling millions of Americans as they try to build their lives, and are increasingly a problem for our national economy. Student debt is the main concern for young voters, according to Business Insider, so we decided to dig deeper to find out where this crisis came from, and how it impacts us all.

Why does the government give out loans to students?

Student loans have a pretty political history. They first hit the scene in 1958 as part of the National Defense Education Act, which was designed to keep the United States from falling behind Russia as the most dominant world power. Since the point of these loans was to compete with Russia in the space race, they were mostly available for college degrees like math, science, and foreign languages.

It’s pretty crazy to think student loans started out to develop defense efforts, but by 1964, new legislation refocused these loans to create educational opportunities for more Americans.

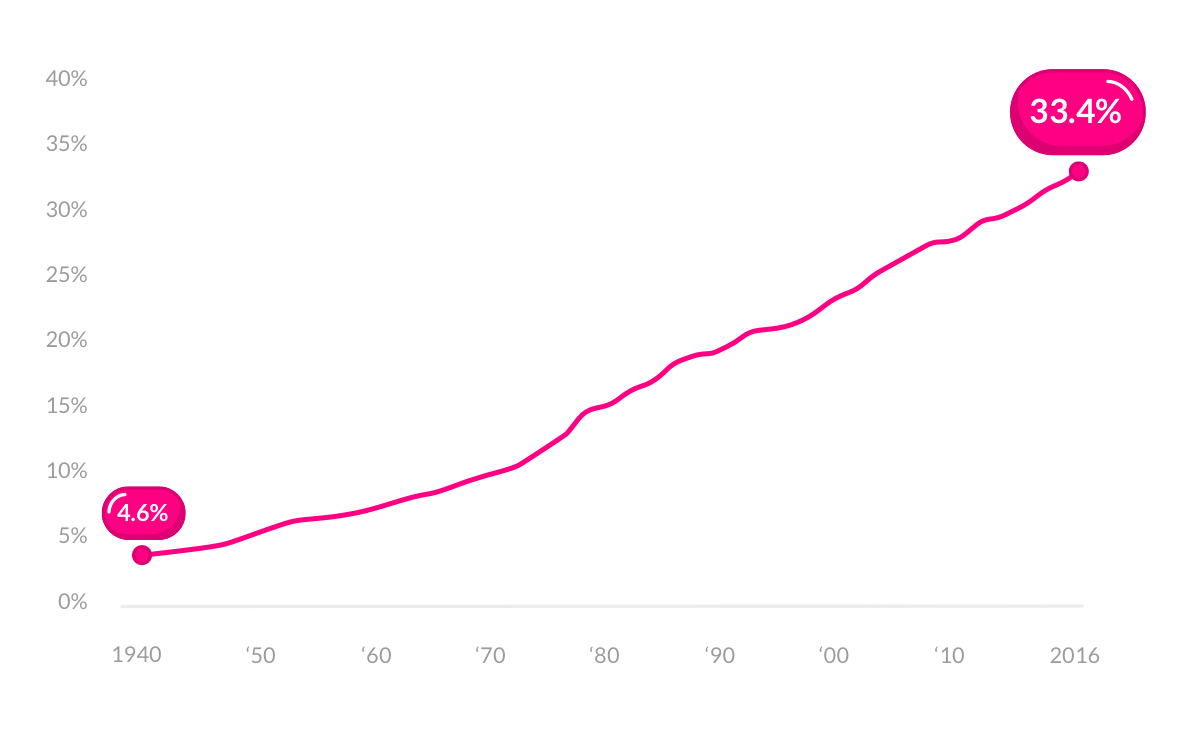

The easier it became to qualify for a student loan, the more people started going to college. According to the U.S. Census Bureau, only 4.6% of adults had a college degree in 1940. By 2017 that percentage climbed up to 33.4%! And, that growing demand for higher education led to increased tuition. By a lot.

How has tuition impacted student loans?

Over the last 30 years, the cost of higher education has spiraled out of control. The College Board reports that tuition and fees have tripled, and believe it or not, that’s after adjusting for inflation. Yes, really… Investopedia says education costs have inflated at twice the rate of normal inflation.

Why has this happened? The financial crisis of 2008 led to less government spending on universities, which meant students had to foot more of the bill. Plus, millions of Americans who lost jobs in the crisis went back to school to pursue more competitive careers. As the job market became more competitive and colleges had less government money, tuition crept higher and higher.

When tuition increases, the number of loans taken out does too, as do the size of those loans. It’s easy to see how increased tuition boosts demand for loans, but it’s much harder to understand how anyone settled for a system that has left so many Americans with so much debt. ‘Student Debt Relief,’ a resource that helps borrowers navigate their debt, questions whether or not these loans have helped society at all:

“While the U.S Government has made it easier for anyone to attend college with the various student loan programs currently available, they have also helped fuel the rising cost of higher education by lending too easily. That degree that was once sought after and had a great impact on someone’s financial life, is now less valuable due to such a high number of college graduates, yet more expensive to attain.”

University enrollment rates have been declining for the past few years, but concerns of an impending financial crisis seem to be on the rise.

Is student debt a national financial crisis?

The Chair of the Federal Reserve has started warning about the way student debt will prevent the economy from growing, and many, many others are raising the ‘crisis’ flag.

In 2018, 69% of undergraduates took out loans and graduated with an average debt of $29k, according to MSNBC. The numbers climb for students pursuing second and third degrees: ‘the average debt for medical school graduates is over $190k, and dental school graduates have it even worse with an average debt of more than $285k’ (Nerd Wallet). That’s a lot of people with a lot of debt. But with a competitive degree, how hard will it be for these graduates to pay back their debt? In most cases… pretty hard.

Once these graduates enter the workforce, they’ll earn salaries that won’t see the same kind of financial growth their parents expected 30 years ago, especially those with only one degree. According to Forbes, the cost to attend a university has increased nearly eight times faster than wages have since 1989, so more and more people are failing to pay their loans.

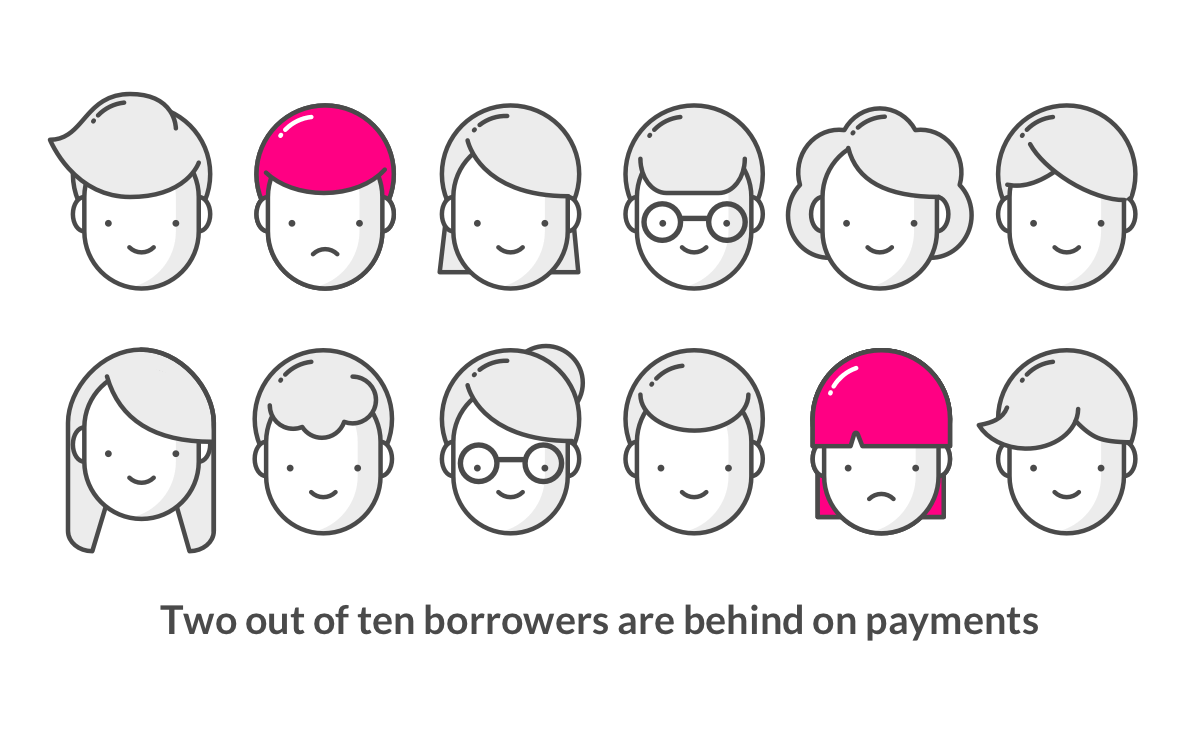

SoFi, an online personal finance company, reports that two out of ten borrowers are behind on payments. What’s worse? After 270 days of delayed payment, loans go into default, which means the borrower can’t get tax refunds, federal student aid, or deferments on their loan, which means even less money in their pocket. Plus, their lender can deduct funds directly from their paycheck, and even sue. And as if that wasn’t bad enough, a borrower’s credit will likely be damaged (btw, this will affect a co-signer’s credit too).

With the consequences of unpaid student loans so high, it’s pretty troubling to think that over 10% of borrowers are defaulting.

What about the 90% of borrowers who aren’t defaulting? Well, student debt limits their buying power for pretty much every other cog in the wheel of our economy. According to NBC, student debt is keeping borrowers from buying homes, buying cars, and saving for retirement. All of that has serious consequences for the economy, and if 10% of borrowers don’t have the ability to repay the government at all, things could get pretty desperate.

What makes the student debt situation even worse is how hard it is to be relieved of loans. While declaring bankruptcy will get rid of many kinds of debt, student loans won’t be written off in bankruptcy proceedings. That means someone could lose their job, lose their home, and still be legally required to make monthly payments on their student debt.

‘Investopedia’ reports that bankruptcy lawyers are arguing student debt should be discharged in a bankruptcy filing, but is that really the best solution we can offer borrowers?

Student debt and consumer protection

It looks like both sides of the aisle are getting serious about student debt and how it impacts the economy. Last month, the House Financial Services Committee held the first of many hearings on student lending, where advocates across the political spectrum criticized how difficult it is for borrowers to understand the terms of their loan and options for refinancing.

With the 2020 elections right around the corner, what comes next for the student debt crisis is undecided, but it may be a relief to know that everyone views this as a problem, and consumer protections are becoming a more important part of political discourse on student debt.

What can I do about the student debt crisis?

Student loans are the fastest-growing kind of debt in the US, and, according to Bloomberg, they also have the highest delinquency rate of all household debt (including mortgages, credit cards, and car loans).

Oddly enough, Russia and student loans are both common topics in political debates, but these days they have little to do with one another. So what can we do about student debt while the state department confronts Russian interference?

That magical four-letter word you keep hearing is important in solving the student debt crisis: VOTE! The issue of student debt is creeping into center stage, so make sure your voice is heard in deciding who will control the next chapter in the student debt saga.

So can you adult with student debt? Despite the confusing paperwork, hold music, and policy manipulation student loan servicers may throw at you, you have the ability to manage your student debt.

Increased political attention is a start, and advocates, like former Consumer Financial Protection Bureau Student Loan Ombudsman Seth Frotman, are working to make student loans more consumer-friendly. While it may not help those of us who’ve already taken out loans, companies like Frank, a super fast and free FAFSA tool with premium membership add-ons, are using tech to make student loans easier to understand and obtain.

There’s no sugarcoating the desperate state of the student debt crisis, but there’s good reason to be hopeful about the future of student loans. If you want to take a deeper (and funny/depressing) dive into the student debt crisis, you can watch Hassan Minaj’s take in this clip from his show Patriot Act. If you want to feel hopeful about your financial future, check out our article about millennials buying homes.