Picture this: it’s the end of the month, which means it’s time to take a look at what you spent this month. You sit down with your computer and your cup of coffee, and anxiously begin to pull up your credit card statement.

You suddenly feel a sense of dread, as you think back to that expensive sushi dinner and your impulsive shoe purchase at the beginning of the month. No matter how well you try to budget each month, you almost never manage to feel confident about reaching your financial goals.

Let’s be real: even if you set a budget, it’s pretty hard to control spending when the impulse to buy hits. In fact, millennials are 52% more likely than any other generation to make impulse purchases. (Time) How can we improve our spending in a way that actually works? We’ve gathered 4 tips and tricks to boost your spending habits, backed by our favorite behavioral economists.

1. Know the worth of a dollar

Picture this: you’re waiting in line at the supermarket with your cereal and bananas in hand. Suddenly, a sale catches your eye – two bottles of wine for the price of one! It seems like a pretty good deal, but then you remember it doesn’t fit into your budget.

In other words, it’s hard to understand the opportunity cost, in behavioral economics speak. In the moment, you probably won’t realize that buying two bottles of wine means less money to spend on going out with friends later.

So how do we trick our minds into recognizing the consequences of our spending?

Goals and anti-goals

“There’s a trick we call goals, and anti-goals,” explains our Chief Behavioral Officer Dan Ariely. “Take two domains of life, let’s say grocery shopping and dinner out with friends. Tie them together. … If you spend more on one, you spend less on the other.”

Let’s put this into practice. Say you decide on a $500 budget to cover your apartment groceries and dinner out each month. Towards the end of the month, you get an invite for dinner and drinks with some college friends. Will that fit into your monthly budget?

To decide, take a look in your fridge. If it looks like the arctic, you should probably pass on dinner this time. But if seems like you’ll have enough grub to hold you over until your next paycheck, go for it!

Now, imagine yourself back at the grocery store, with your cereal, bananas, and your eyes on this exciting wine sale. But this time, you’ll know the money you spend on the wine will mean one less sushi dinner out with your roommate. Will you be just as tempted to buy the wine? Probably not. By pairing domains together, you can trick your brain into remembering the opportunity cost of each additional purchase.

2. Cut back on one category or activity

Here’s another trick: “If you need to cut back on your lifestyle, we find that in general it’s easier for people to just cut things off as a category,” advises Professor Ariely. (Slate) Telling yourself you’ll stop spending money on one category entirely will eliminate your need to choose on a daily basis, because the decision will have already been made for you. But how will you decide which domain to eliminate?

The best approach is to understand which activity you can give up that will have the smallest impact on your happiness. Is it shoe shopping, going out to dinner, or taking Lyfts?

Dan Ariely wanted to get to the bottom of it, so he conducted a study. He went into people’s bank accounts, pulled 40 transactions, and asked each person: “To what extent do you regret paying for this? Do you think this purchase was a good decision, or a bad decision?”

He tallied up the numbers, and found that participants mostly ended up regretting the money they spent while going out. Why? Because going out is expensive, and we often wake up the next day regretting how much we ate or drank.

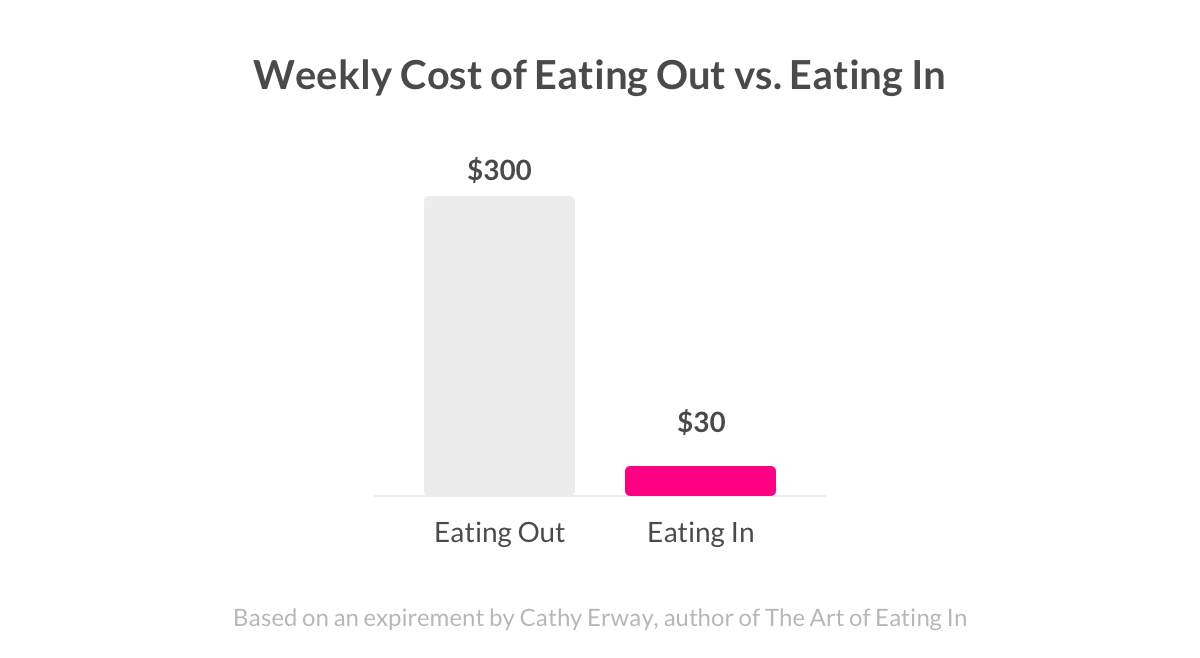

Cathy Erway, author of The Art of Eating In, did an experiment of her own: she went out for every meal for a week to compare how her expenses looked when she ate out versus when she ate in. Turns out, she spent over $300 a week when she ate out, and only $30 a week when she ate in. So if you eliminate the option of going out, that’s 10x more money you can have in your account each week.

Choose your own domain

Bottom line: cutting back on just one area of your life can make a serious impact on your budgeting efforts. But everyone’s different. For some, cutting back on dining out is the best solution, and for others, going out for dinner is a highlight of their week.

To figure out what makes most sense for you, replicate Dan Ariely’s experiment for yourself:

1. Look at your most recent bank statement – go over each transaction over the last month or two

2. Categorize your purchases (ex. coffee, restaurant, shoe shopping)

3. Rate each purchase on a scale of 1 – 10 in terms of how much you regret the purchase (1 being ‘totally worth it,’ 10 being ‘I wish I could turn back time!’)

4. Tally up each category, and see which one has led to the highest amount of regret

Voilà! You’ve found that sweet spot of where you can save money each month. Now get saving.

3. Minimize your credit card usage

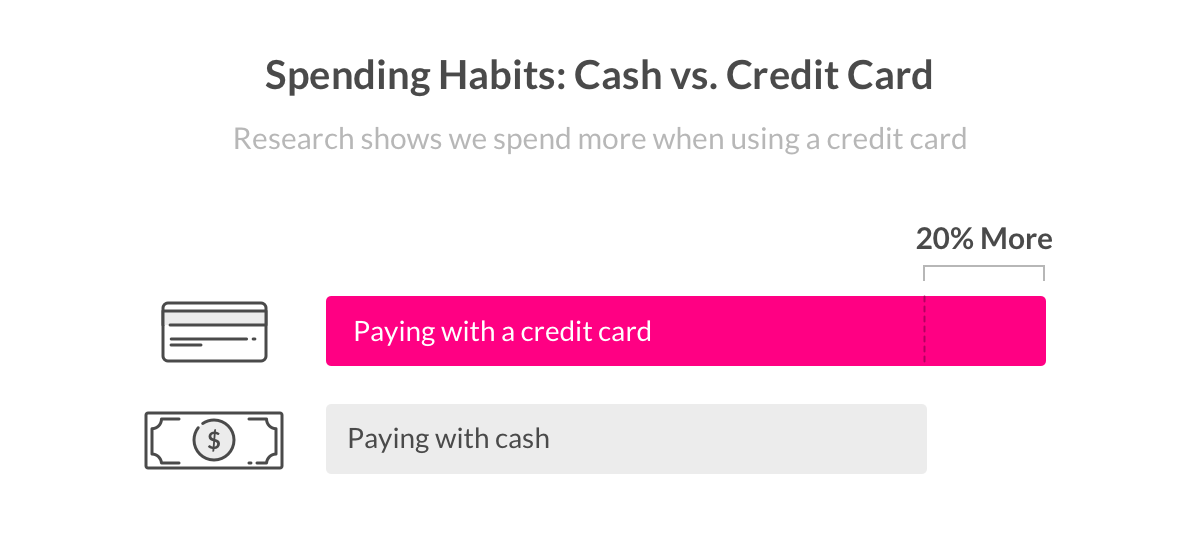

When’s the last time you paid cash, not credit? For most, it’s been a little while. Studies show 75% of US consumers prefer paying with a credit card, while only 11% prefer paying with cash.

Credit cards offer a ton of benefits: they’re slim, convenient, and more recoverable than stolen cash. But there’s a downside – people who use credit cards are likely to spend more money on purchases than people who use cash. For example, participants in a study on spending behavior were willing to spend $175 to throw a Thanksgiving party when using a credit card, but only $145 when paying in cash. (APA) Why is that?

The less transparent your spending is, the lower your ‘pain of paying’ will be, according to researchers Priya Raghubir and Joydeep Srivastava. Credit cards create a separation between the moment you buy and the moment you pay your bill, which can mask a feeling of loss. Credit cards also allow different purchases to be mixed together. So when you pay your bill, you don’t associate what you owe with any single purchase (i.e. you focus on paying a total of $645 rather than $120 for new running shoes, $50 for a nice dinner out, and $475 for a flight home for the holidays).

Put an end to mindless purchases

So does this mean we have to use cash for all of our purchases? Truth be told, that would be unrealistic. Credit cards are just too convenient. Instead, Dan Ariely suggests “we take all of our discretionary spending – on coffee, going out, and theater – and put that amount on a prepaid debit card on a weekly basis.” Now that’s better than a cash-only cleanse!

This tiny trick will prevent you from falling into the trap of mindlessly purchasing things you don’t even really need. If you create a limit on our swipes, you’ll think twice before throwing that extra snack into your shopping cart, especially if you have to whip out an entirely new card to pay for it.

4. Break bad habits

We all have that one bad spending habit we just can’t shake. Whether you always have to buy the latest gadget on Amazon Prime, or can’t help but purchase that expensive stinky cheese at the grocery store each week, these bad habits can set back even the healthiest of budgets.

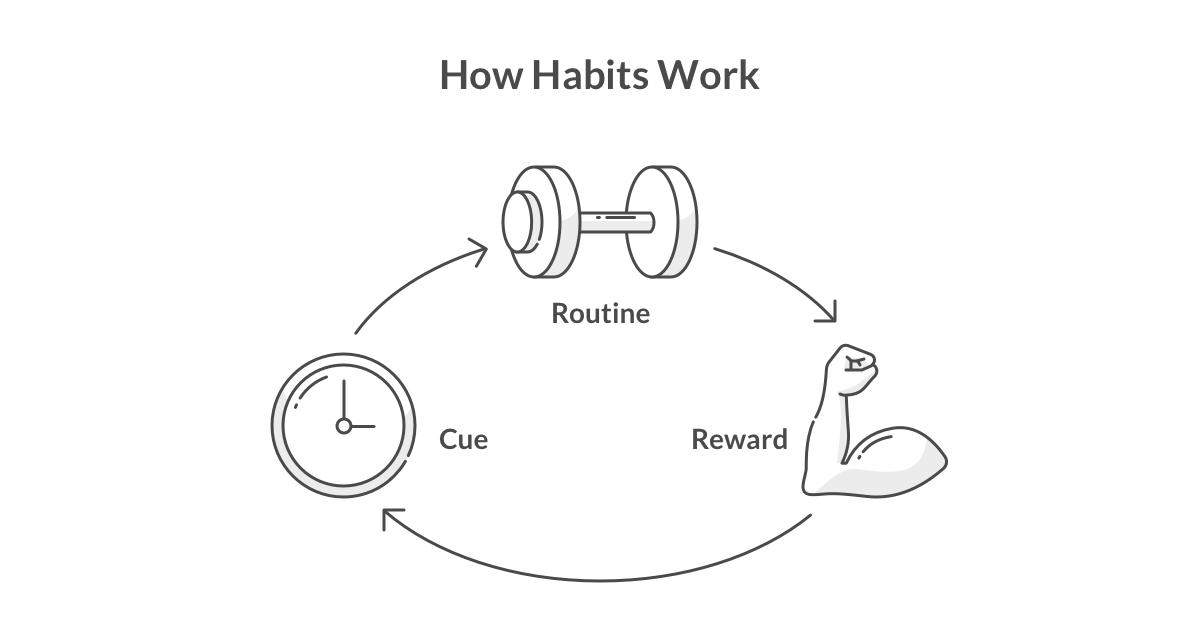

But sometimes, these habits are so ingrained that they feel impossible to break. Luckily, best-selling author Charles Duhigg laid out a scientific process to help you overcome basically any habit. In his bestselling book Habit, he explains:

“There’s a simple neurological loop at the core of every habit, a loop that consists of three parts: a cue, a routine, and a reward… To understand your own habits, you need to identify the components of your loops. Once you have diagnosed the habit loop of a particular behavior, you can look to supplant old vices with new routines.”

How to break a habit

Let’s try it: imagine you have a habit of buying a large, double shot latte every day on your way to work. While the latte is the perfect morning boost, spending that extra $5 every day is getting in the way of your spending goals. You want to cut the routine, but just can’t muster up the motivation. Where do you start?

First, identify the behavior you’d like to change. In this case, it’s that you pass by the coffee shop, walk in, order the latte, pay, and then enjoy it on your way to work.

That was easy. Now, identify what that triggers this habit. Is it thirst? Being bored? Low energy? Time of day? Location?

To figure it out, you’ll need to experiment. Here’s how: Try slightly changing your routine every morning so it brings a different reward. Instead of stopping by the coffee shop, bring a shake that you made at home. When you get to work, see if you still have a craving for that latte. If you still feel the urge, you know your habit isn’t motivated by thirst. But if you feel satisfied after drinking a caffeinated soda, you’ve identified the reward – caffeine – that your habit sought to satisfy.

The last step is figuring out the cue. According to Duhigg, almost all habits are triggered by one of these five things: location, time, emotional state, other people, or the activity immediately preceding action. To figure out the cue for your bad habit, answer these five questions the moment the craving hits:

1. Where are you? Outside the coffeeshop

2. What time is it? 8:45am

3. What’s your emotional state? Tired

4. Who else is around? No one

5. What action preceded this urge? Walking

Continue this process for a few days, and notice which condition is consistent when you start craving coffee. For example, you may find that no matter the time of day, and regardless of your mood, you walk into the coffee shop every time you pass by it. In other words, your location is the trigger.

Create a new behavior

Once you figure out your habit loop, you can begin to shift your behavior by planning for the cue, and choosing a better routine that delivers the reward you are craving.

For example, if you know you crave a caffeine boost every time you pass by the coffee shop, find a different route to work, or plan to bring a caffeine boost along your walk so you’re prepared once you pass by the shop and the craving hits.

If one small fix can save you a few dollars every few days, you’ll see the results add up pretty quickly. Correcting a bad habit will help you take better control of your spending, and will allow you to splurge on what you love out of novelty, not routine.

Go forth!

With these methods, you’ll get rid of that sense of dread when opening your bank statement! Phewf. The secret to better budgeting is to simply trick your mind into feeling the impact of your spending each day.

It may be tricky at first, but when you make a habit out of these spending hacks, we promise it’ll feel effortless. Pretty soon, saving more money each month will be a walk in the park.