When no witnesses are within earshot, insurance executives confess that pooling people into meaningful communities, instead of meaningless masses, is better for consumers. They acknowledge the power of affinity to reduce fraud, bureaucracy, and premiums. But, they confide, they made a pact with the devil: they traded affinity for growth. You see, in the traditional insurance model, you can have affinity or you can have growth. You cannot have both.

The tale of USAA, one of America’s most respected insurers, illustrates this trade-off. Founded in 1922, when 25 officers pooled their risk, USAA had great affinity, great trust, and a great product. But they wanted to grow. So two years later they opened to all officers (hundreds of thousands), then to all enlisted personnel (millions), and then to all veterans (tens of millions).

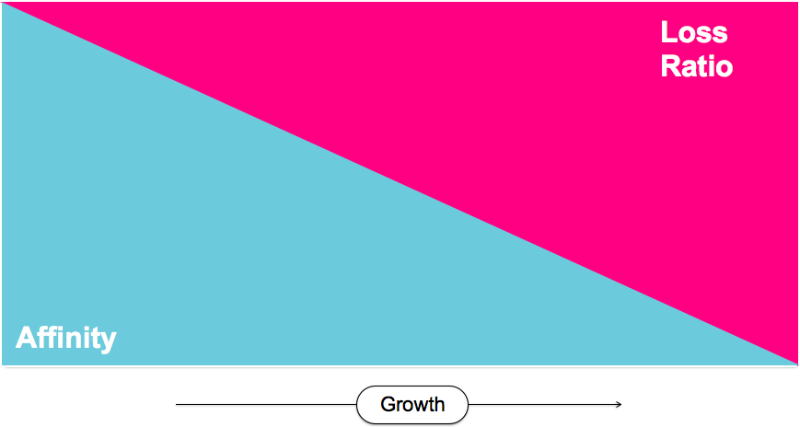

Every time they opened that aperture, their ‘loss ratio’ – the percentage of premiums paid out in claims – grew. A rising loss ratio is a bad omen.

Growth dilutes affinity and that means damaging the product. People become estranged and distrust reigns. Consumers typically experience the blowback as rate hikes and claim denials.

As open as USAA has become, it has not abandoned its communal core. This makes it an exception. In pursuit of growth, the industry has forsaken affinity almost entirely. GEICO is an acronym for ‘Government Employees Insurance Company’, but that’s distant history. GEICO has more affinity with a cockney-accented-lizard than with government employees.

The downward spiral is easy to chart but hard to reverse: growth quashes affinity, alienation fosters fraud, and heavy-handed claims adjusters replace trust. Before you know it, premiums go up, while getting paid becomes a nightmare. In this industry, the pursuit of growth is a race to the bottom.

Fortunately, the tradeoff between affinity and growth exists only in the old economy. Facebook has 1.6 billion users, but it didn’t dilute affinity even as it grew exponentially. Your experience on Facebook is intimate, and you know the people on your network.

Setting up a traditional insurance company is a huge undertaking. They’re never going to make one just for you and your friends – so they pool you with millions of strangers instead. But in software, the cost of spawning a new social group is zero, so Facebook was able to grow its memberships without sacrificing cohesion. In the digital economy, affinity doesn’t stall growth, it propels growth.

Insurance built on the paradigm of social networks would combine true affinity with universal eligibility. It holds the promise of insurance that’s far less conflicted, costly, and bureaucratic.

The good news is, that’s exactly what we’re doing.