If you’re interested in how Lemonade is functioning from an insurance perspective, read on. I hope it will be less painful, and more revealing, than rummaging through regulatory filings.

A word to the wise

We launched three months ago, and as anyone with a feel for statistics will tell you, 100 days of data isn’t that meaningful in insurance. So I don’t want to create the impression that the results I’m sharing establish a predictable trend. They don’t. We’re here for the long term, and long term results are what matters. Our story will evolve – transparently – over time.

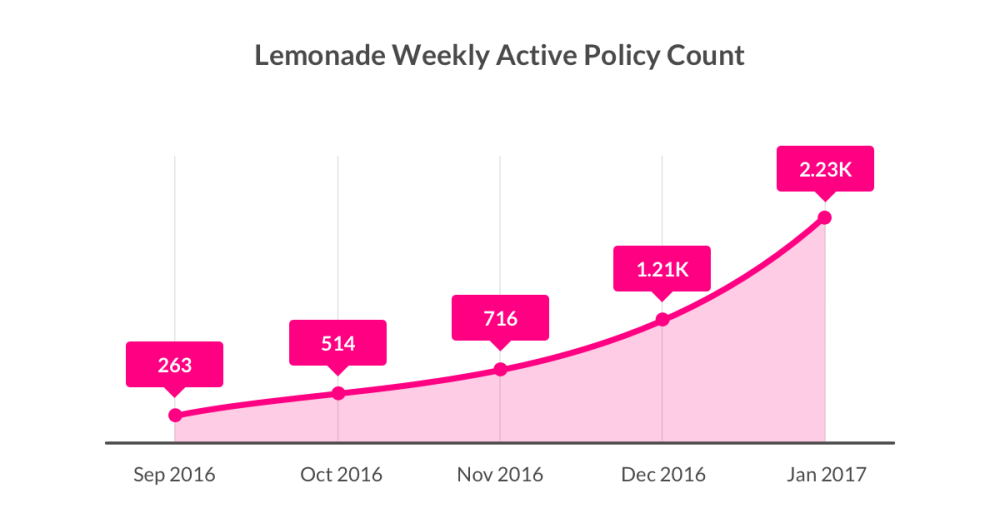

Lemonade’s growth got off to a strong start.

Premium growth is important (see analysis in a report on our Q4 – 2016 performance), though in this update I’m going to focus more on insurance metrics, with commentary on the quality and diversity of our customers and claims. On those fronts too, I’m happy to report: so far so great.

Our customers, through an insurance lens

1. Our customers are new to insurance

More and more people are switching to Lemonade every day, coming from very well-known insurance companies. At the very least, this is a good early sign. But, more importantly, we’re bringing in a new breed of customers – the underserved. The majority of customers insured with Lemonade are actually new to insurance. They had never found an insurance company that they liked, trusted, or interacted with, the way they wanted – until now. We love that.

Insurance is something everybody needs, and we are not competing just on price, but on simplicity, speed, value and values.

2. Our customers are thoughtful

Although the basic $5/month policies are sufficient for some, a lot of our customers are asking us not only to protect them, their homes, and their basic stuff, but to add valuables to their policies and insure their jewelry, artwork, musical instruments, bikes or laptops.

It’s thrilling when customers buy the basic, and then add extra coverage for all of things they value. Some of the requests have been quite surprising! While we can’t add everything immediately, we’re accommodating as fast as we can.

3. Our customers are diverse

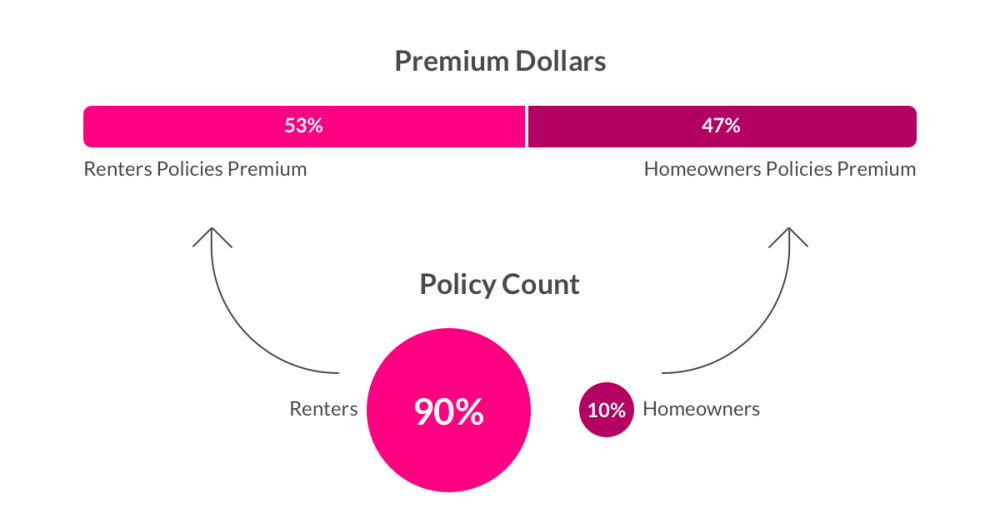

In insurance, you never want just one type of customer. Since our goal is to share risk across customers, too much concentration isn’t ideal. While we have a lot of renters, almost 50% of our premium came from homeowners – many with over $500K and up to $1.5m of coverage.

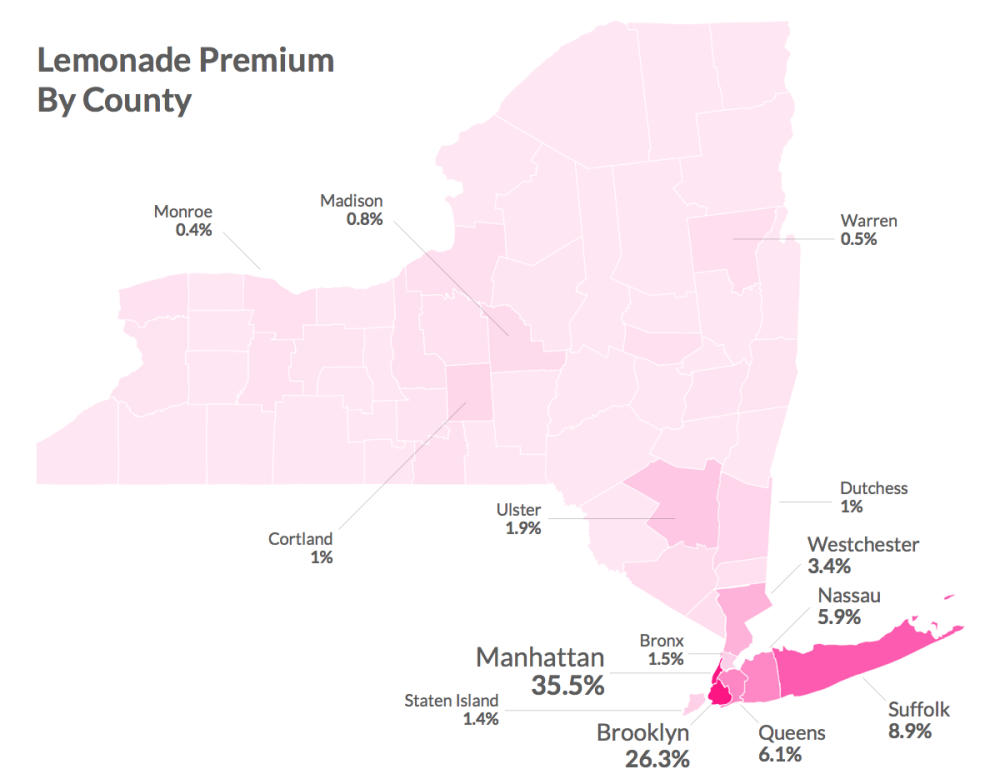

Our customers are geographically diverse as well.

While 35% of our premium is from Manhattan, the rest is spread across the NY metropolitan area, and across the state. Lemonade is no one trick pony.

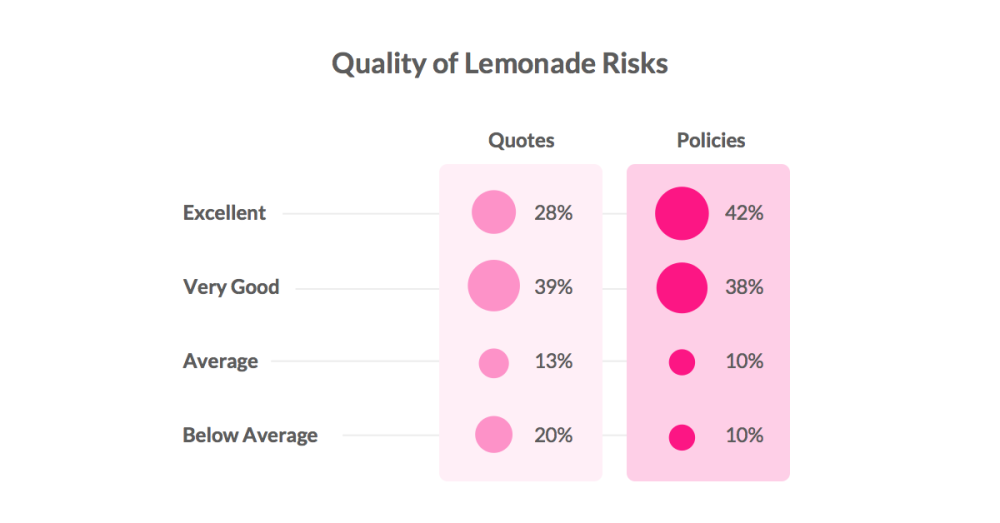

4. Our customers represent ‘high quality’ risks

Perhaps the most important part of underwriting is ensuring we don’t have ‘adverse selection.’ This means insuring someone only because our prices are (too) low, or because we attract the riskiest policies. We use a series of factors to help predict if a risk is better or worse than average, and to price it as accurately as possible.

Two bits of good news in this regard:

- Potential customers that come to Lemonade for insurance score above average as ‘risks’

- Even more important, the best risks tend to end up buying Lemonade!

Having said that, there’s a lot we can improve on the underwriting side, and we’re working hard to train our algorithms to make better decisions. The more data we gather, the better our algorithms get.

5. Our customers are helping us to make insurance into a social good

We celebrate claims when they come in. We’ve had a few (6 in 2016, to be precise) – exactly the number we expected based on industry statistics. What is different is that our claims have all been small – way smaller than industry averages. It’s too early to mean much, but right now our loss ratio is much better than the rest of the industry, and I’m hoping this hints that the Lemonade Giveback will be strong this year.

The nitty gritty insurance numbers

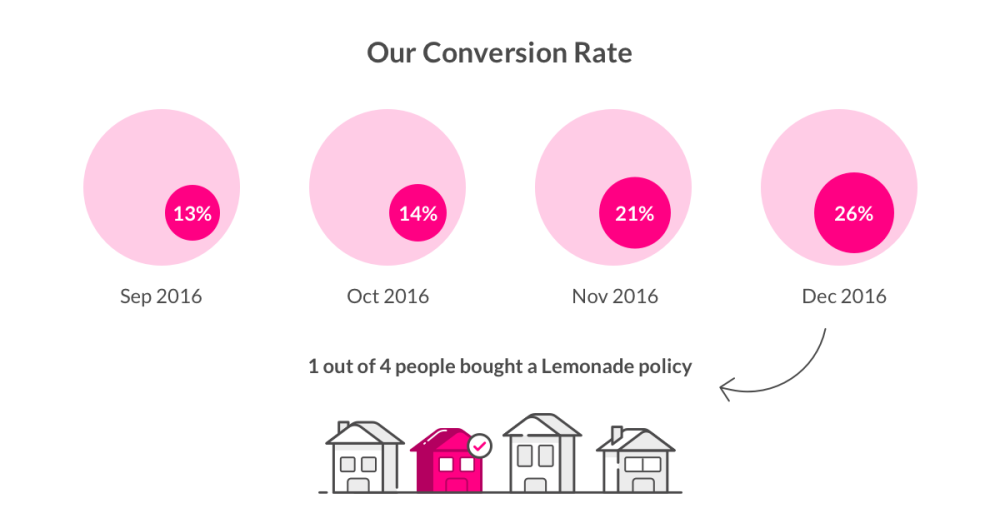

Right now, over 25% of people that get a price, buy. This is high by any standard, both in insurance and tech. What is extraordinary, however, is the trend.

The percentage of people buying when they get a quote is increasing every single month. In December, we were up to 36% for renters, and 26% overall. In insurance, you want to buy from someone you trust.

We’re ecstatic that our customers trust us to protect them, and we look forward to living up to that promise.

Our ‘written premium’ (basically how much insurance we sold) in 2016 (the last 100 days of the year, really) was $179,855. Our ‘gross loss ratio’ (or claims we received in 2016 divided by ‘earned’ premium) was 20%; a portion of that should be recovered from another insurance company, so we expect our final loss ratio for 2016 to end up at about 12%.

While our reinsurers are standing by to help pay losses, we have not needed them yet.

What we need to work on

While it all sounds great, some things did not work as we expected, and we had to adjust accordingly:

1. Get more data in

There is a ton of information out there that can help sign customers up faster and ensure the coverage is right. While we gather and implement a lot of data, we’re only scratching the surface. For some homes, we need to ask you the square footage, which is kind of lame in this day and age. We’ve made it a priority to seek out and incorporate new and different data every day to make sure policies are appropriate, and our customers are protected.

2. Innovating in… language!

When we started selling policies back in September, we wanted to make sure regulators and customers were comfortable, so we launched Lemonade with the industry standard insurance policy contract. We know that it is poorly written, and unless you have a law degree – frankly even if you have a law degree – it can become confusing.

Who knew your liability coverage actually changes depending on whether or not you are also an insured under a policy written by the Nuclear Insurance Association of Canada (Section II.F.5.a.(3)). I assume most of our policyholders do not.

We’re going to improve the policy so you can actually read it and understand what is covered and what is not. It will take time, but we will do it – I promise.

3. Improving our coverages

Our policy is great for most people, but isn’t as customizable as we want it to be. For example, at launch we could not add fine art – now we can. Need your landlord listed on the policy? We added that a few weeks ago. Identity theft coverage? Still no, but that will be here in a week or two. Kidnap and Ransom coverage – that one is a little farther off.

If we can’t protect it yet, we will tell you… and know we are adding options every day.

A lot of the incentive behind the Lemonade Transparency Chronicles was about trust. As Daniel wrote in his post, trust can’t be demanded, it has to be earned. We have the good fortune of having a strong, rapidly growing base of customers who trust us, and who we trust too. Together we are building a company for the long haul, and the early metrics make me feel like we are on the right path.

Stay tuned for Prof. Dan Ariely’s report next week, revealing Lemonade’s social impact in its first 100 days of business.