Getting A New Car After a Total Loss Declaration: A Comprehensive Guide

Practical steps to get behind the wheel again with confidence.

Practical steps to get behind the wheel again with confidence.

There’s a lot to process when your car insurance company declares your car a total loss.

Your trusted means of transportation is gone, you may be looking for support in navigating life after a car accident, and you might be faced with a lot of insurance jargon and financial decisions that is enough to make your head spin. Plus you’ll simultaneously be figuring out how to get a new car and get back on the road.

When you drive with Lemonade car insurance, we’re here to help you on your journey after total loss.

Insurance jargon can be confusing. And when your car is declared a total loss, you’ll want to be familiar with some terminology. Let’s break down some of the most common terms around total loss, in plain English.

If your car is deemed a total loss, your insurance company will complete an assessment of your car to determine its actual cash value (ACV).

Your insurance company would likely conduct research based on several factors about your car, which may include:

These details help determine a fair value for your totaled car, compared to similar cars in your area. From there, you’d be presented with your car’s ACV and a copy of the market evaluation.

Before you can receive a payout for your totaled car, you’ll most likely have to release your car to your insurance company, remove any personal items from the car, and sign any necessary paperwork.

If you have a loan on your car, let your lender know that your insurance company will be contacting them.

The lender will transfer the title into their name, convert it to a salvage title, and probably sell the totaled vehicle to a salvage yard.

Your car insurance company may request details about your car’s lienholder to help ease this process.

If you own your vehicle outright, without a loan or lien, you may be able to keep your totaled car and repair it yourself (if you really want to). Your insurer would just deduct the salvage value from your settlement.

Keep in mind that in some states you may not be allowed to keep a totaled car, and even if you can, there may be specific requirements in place that you need to follow closely in order to keep and repair it. So if you do decide to keep your totaled car, make sure to share proof of all the repairs with your car insurer.

Relevant state laws can vary here, so check with your claims adjuster before going down this route. If the DMV converts your title into a salvage title it could be difficult to sell the vehicle or get insurance for it again after you’ve gotten it roadworthy-and you definitely don’t want to wind up with a lapse in your car insurance, or drive uninsured.

If your car is taken directly to the salvage facility, you’ll need to reach out to your adjuster to discuss temporary transportation.

But let’s say your damaged car is brought to the repair shop first, since your insurance company believes it can still be fixed. You rent a car, or start using rideshare services like Lyft. Two days later, the garage calls with some bummer news: Your ride is totalled.

Thankfully, most policies allow for a few days of rental car coverage even after the car is declared a total loss and you are paid the settlement for the amount the car was worth. But it’s best to check with your insurer if you’re eligible for coverage on temporary transportation after a total loss declaration based on your policy’s unique details.

Navigating the car market after a total loss can feel overwhelming. Here are some steps to help you find the best set of wheels for your needs.

Here are some questions to ask yourself when making a list of what you need (and want) for your next vehicle:

Here are some things to consider when you’re navigating the financial landscape of buying a new car after total loss:

Take the time to research, compare, and test-drive potential vehicles to make an informed decision and ensure that your new car meets your needs, and fits your budget.

Depending on your insurance company and the terms of your insurance policy, you might need to cancel your current policy or simply update it with the details of your new car.

If you’re driving a rental car while shopping around for a new ride after a total loss, continue covering your totaled car on your policy until you’ve returned your rental-or contact your car insurance provider-to make sure you don’t wind up in a coverage lapse.

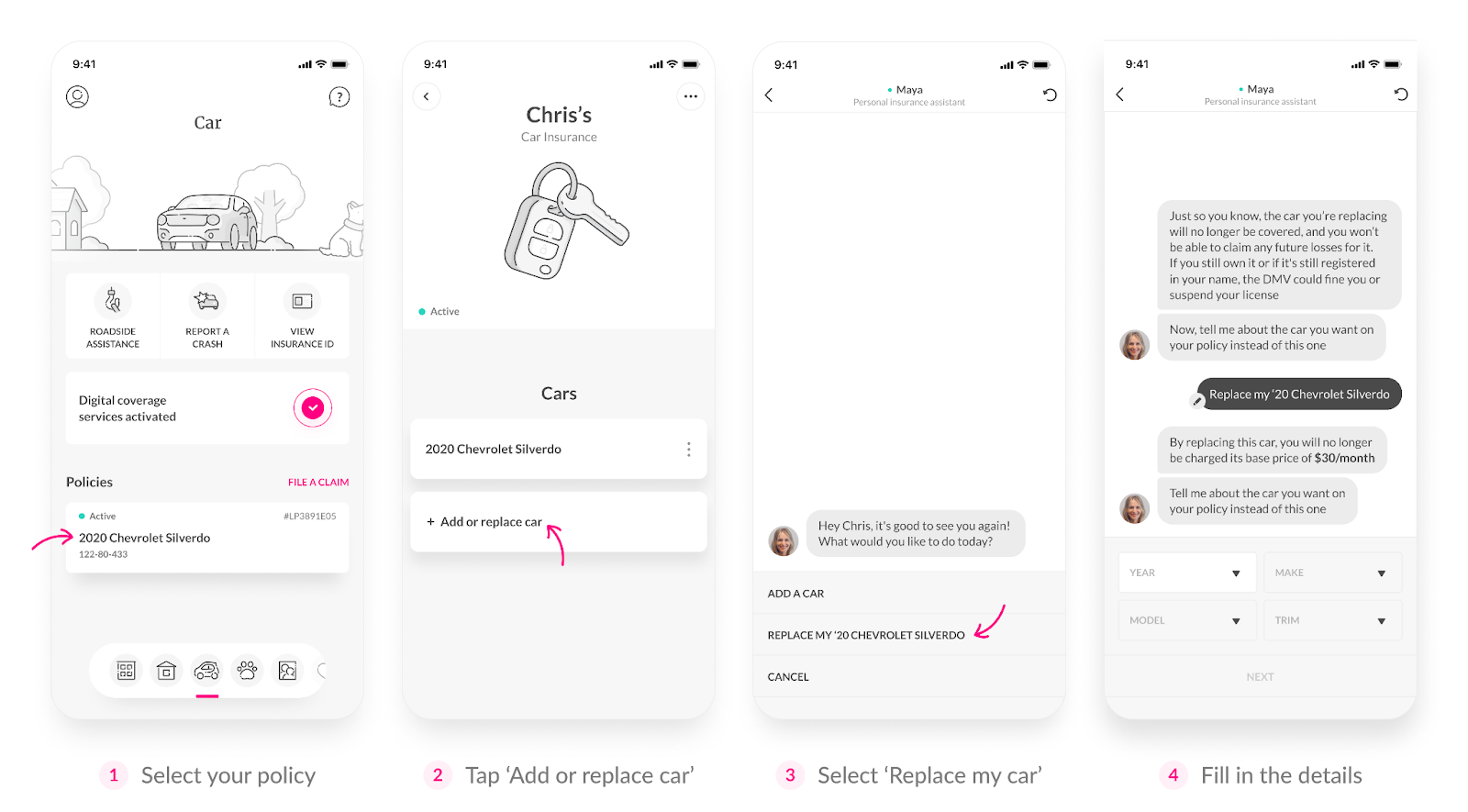

Just bought a new car after a total loss declaration? Don’t assume that your insurer will automatically remove your totaled car from your policy. At Lemonade Car, we make it easy to manage your car insurance policy-like replacing a car-all on the Lemonade app.

To get started, head over to the Car tab on the app and select your policy. Then scroll down to the ‘Cars’ section. Here you’ll see a list of your covered vehicles, followed by an option that reads ‘+Add or Replace car’.

From there, our trusty chatbot AI Maya will help you navigate through the rest of the process. You’ll have the option to remove the totaled car from your policy and replace it with another car-and you’ll be able to see how these changes affect your pricing.

Don’t forget: You can cover up to four cars on a single Lemonade Car policy, but any car that you include on your policy needs to be registered under your or your spouse’s name. Adding or replacing cars on your policy can impact your policy price.

A total loss refers to a situation where a car is damaged to the point that the cost to repair exceeds the actual cash value (ACV) of the car, it’s unsafe to repair, or it can’t be returned to its pre-accident condition. This could be determined at the accident scene, or after a detailed estimate of the repairs by an insurance adjuster. A total loss can also be declared if a vehicle is stolen and not recovered after 30 days, or if it has unrepairable structural or flood damage.

The value of your car is determined through a process of appraisal by your insurance company. They will inspect the vehicle for any pre-existing damage and consider factors such as the car’s age, interior condition, and market value. Any aftermarket upgrades to your car that weren’t included by your car’s manufacturer-like hot pink leather seats, or alloy wheels-likely won’t be factored into the value at all, or beyond a limit that’s outlined in your policy. Finally, will take into consideration the salvage value to determine your car’s actual cash value.

Your insurance company may offer you a payout based on the actual cash value of your totaled car, minus your deductible, if your car was totaled in a covered incident. If you still owe money on a car loan, your insurance company will pay the lender first, and then issue you any remaining funds. This payout may not fully cover the cost of a new vehicle, especially if the car’s value was less than the amount remaining on the loan. In this case, gap coverage could potentially cover the difference.

You generally need collision insurance coverage and comprehensive insurance coverage as part of your car insurance policy to be eligible for reimbursement after a total loss. Collision coverage helps pay for damage to your car from accidents with other vehicles or objects, while comprehensive coverage helps pay for damage from other incidents-like theft, or natural disasters. Learn more about the differences between collision and comprehensive coverage here.

We’re live in the following states: Arizona, Colorado, Illinois, Indiana, Ohio, Oregon, Tennessee, Texas, and Washington.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.