How Much Is Pet Insurance?

Let’s dig into the factors that impact how much your pet insurance costs.

Let’s dig into the factors that impact how much your pet insurance costs.

At Lemonade, a policy for a dog or a cat starts at $10/month. (Plus our affordable pet insurance has won the approval of authorities like Money.com).

But the cost of pet insurance coverage can vary depending on several factors, including the amount and type of coverage you choose, the breed and age of your furry family member, and where you live. It’s a small price to pay to be prepared for the unexpected.

Let’s skip the complicated insurance jargon, and look at how much pet insurance actually costs.

The prices of pet insurance plans can vary significantly, depending on a bunch of different factors, so we decided to check rates for a typical cat and a typical dog at six different insurance companies.

Let’s look at an example: If you have a 4-year-old Goldendoodle in Chicago enrolled in a plan with 80% co-insurance, the maximum annual limit available, and an annual deductible of $250, you’ll pay an average of $61/month.

| Insurance Provider | Average Monthly Cost |

|---|---|

| Trupanion | $336 |

| Healthy Paws | $85 |

| Pets Best | $77 |

| Many Pets | $73 |

| Fetch | $99 |

| Lemonade | $61 |

On average, across different ages, breeds, and locations, Lemonade pet parents pay around $48/month to keep their pups covered.

We got a pet insurance quote for a 1-year-old, short-haired cat in Danbury, Connecticut. We picked the base policy offered by six different pet insurance companies, and adjusted the coverages as much as we could to include a $250 deductible, 80% co-insurance, and the maximum annual limit available, with no add-ons or discounts. With this kitty and these policy details, you’ll pay an average premium of about $34/month.

Please note: we built these quotes to be as identical as possible, but there are a few coverage differences to note. For example, Trupanion only offered a 90% co-insurance option. We standardized the offerings as much as possible.

| Insurance Provider | Average Monthly Cost |

|---|---|

| Trupanion | $58 |

| Pets Best | $35 |

| Many Pets | $44 |

| Fetch | $36 |

| Lemonade | $29 |

On average, across different ages, breeds, and locations, Lemonade cat parents pay around $27/month to keep their kitties covered.

Curious how your location affects the cost of pet insurance? Check out the average monthly cost of Lemonade pet insurance for both dogs and cats, so you can get a quick sense of what to expect.

| State | Average monthly cost of pet insurance* |

|---|---|

| Alabama | $30 to $34 |

| Arizona | $35 to $39 |

| Arkansas | $30 to $34 |

| California | $45 to $49 |

| Colorado | $40 to $44 |

| Connecticut | $45 to $49 |

| DC | $40 to $44 |

| Florida | $35 to $39 |

| Georgia | $30 to $34 |

| Illinois | $40 to $44 |

| Indiana | $30 to $34 |

| Iowa | $25 to $29 |

| Louisiana | $21 to $36 |

| Maryland | $40 to $44 |

| Massachusetts | $40 to $44 |

| Michigan | $30 to $34 |

| Minnesota | $23 to $47 |

| Mississippi | $25 to $29 |

| Missouri | $30 to $34 |

| Montana | $30 to $34 |

| Nebraska | $30 to $34 |

| Nevada | $30 to $34 |

| New Hampshire | $45 to $49 |

| New Jersey | $35 to $39 |

| New Mexico | $25 to $29 |

| New York | $40 to $44 |

| North Carolina | $35 to $39 |

| North Dakota | $25 to $29 |

| Ohio | $30 to $34 |

| Oklahoma | $20 to $24 |

| Oregon | $40 to $44 |

| Pennsylvania | $30 to $34 |

| Rhode Island | $25 to $29 |

| South Carolina | $30 to $34 |

| Tennessee | $30 to $34 |

| Texas | $30 to $34 |

| Utah | $30 to $34 |

| Virginia | $40 to $44 |

| Washington | $35 to 39 |

| Wisconsin | $35 to $39 |

Several factors impact your pet insurance quote:

Cats are usually cheaper to insure than dogs because medical costs are generally cheaper for cats. Cats live longer than dogs, and while both will require vaccinations and exam fees throughout their lives, cats tend to have fewer health problems. Many cats stay inside, so they’re less exposed to risks that could lead to an accident or an illness than a dog is. Dogs are also more prone to hereditary conditions like hip dysplasia or issues with a cruciate ligament.

Like older people, older pets tend to need more healthcare. When you purchase pet insurance your pet’s age will impact your monthly premium.

Certain dog breeds and cat breeds are naturally more costly to take care of than others. So if you know your cat is more likely to develop a hereditary condition like asthma because she’s a Siamese, should you assume it will be considered a pre-existing condition? Not exactly.

Your pet may not show signs of these medical conditions at birth, or in the first few years of their life. But if you wait until they develop symptoms to get insured, the condition probably won’t be covered by your policy. If you insure your pet when they’re still young and symptom-free, though, pet insurance could help cover the vet bills to treat their chronic condition-which could be a real game changer.

Your pet insurance rate can also change depending on where you live, since vet care is more expensive in some states than others. For example, medical costs in California are higher than they are in Tennessee.

That could also mean you’re being charged more for a vet visit. While this wouldn’t affect your monthly premium, it may affect how quickly you reach your annual limit, so make sure you customize your pet insurance policy so it’s worth it for you.

Wondering if pet insurance is worth it? Check out how much pet parents of dogs and cats have saved on vet bills by signing their fur baby up for pet insurance.

You might be able to lower your monthly cost by adjusting your co-insurance, deductible, and annual limit on your pet insurance policy. In most states*, you can request coverage downgrades such as increasing your deductible or decreasing your co-insurance at any time during the policy period. We bet you’d appreciate an explanation of what those things all are, and the available options:

Co-insurance (which is not the same thing as a co-pay) is the percentage of the total cost your insurance company will pay on a claim. So if the co-insurance you chose is 80%, then the company pays for 80% of covered costs when your pet gets veterinary care, and you pay the other 20%.

Keep in mind that this is applied to every claim. With Lemonade pet insurance, for example, you can pick either a 70%, 80%, or 90% co-insurance.

Another way you participate in the cost of your claim is your deductible. You choose this amount-at Lemonade, it’s either $100, $250, $500, and $750.

The higher your deductible, the lower your monthly premium will be. Keep in mind: If you increase your deductible, it increases the amount you are responsible to pay out-of-pocket in the future. So before choosing a deductible, ask yourself-What amount of my pet’s medical expenses could I cover myself before I need help from my insurance company?

Your pet insurance policy has an annual deductible, which means you can exhaust it in one big claim, or use it up over multiple claims throughout the course of a year.

Most pet insurance providers have a limit to the payouts they can provide, but the good news is, you get to pick what that limit is. At Lemonade, you can choose an annual limit anywhere between $5,000 and $100,000. Your medical bills for your fur fam can add up quickly, so make sure your insurance coverage is the right fit for your budget and your pet.

You might be able to lower your premium by 10% or 15% by making one of these changes, but don’t forget that while adjusting these reimbursement levels can help lower your monthly payments, it’ll mean you’re covered for less when an expensive vet bill rolls in.

To explore your coverage options, shoot us an email at [email protected]. If you’d rather chat over the phone, give us a call at 1-844-733-8666, we’ll be happy to help!

*Not available in New Hampshire or California

Still confused about what actually happens when you file a claim? We’ve got you. Let’s walk through an example, nice and slow.

Here’s how your claim payment would be calculated:

($6,000 x 80%) – $250 = $4,550

Since your insurance company would pay $4,550 towards this claim, you and Mogley would be responsible for the remainder-in this case, $1,450 (that amount includes the $250 deductible).

Now let’s say a few months later you have to file another claim, after Mogley swallows a mysterious object. The resulting procedure costs $1,500. Since you already paid your deductible for the year, here’s what your claim calculation would be:

($1,500 x 80%) – $0 = $1,200

You’d only need to pay $300 for the procedure (the $1,500 bill minus the $1,200 your insurance company contributes). This is how your claims would work for the rest of the year until you reach your annual limit.

Since Lemonade Pet works on a reimbursement basis, you can take your pet to any vet you’d like in the U.S., as long as they’re licensed to provide veterinary care in the state they operate in.

You’d pay the bill for your pet’s care or treatment upfront, then submit those receipts to us in the Lemonade mobile app for reimbursement. Our claims team will review to make sure the situation you’re claiming is covered under your policy, and reimburse you for the amount you’re eligible for on the claim.

Having pet insurance means you can avoid having to ask yourself whether you can afford the treatment out-of-pocket that your pet needs to live their best life.

A standard pet insurance policy will help cover the costs of diagnostics, procedures, and medications to treat your dog or cat’s eligible accidents and illnesses.

That means something like a broken leg or an injury from a car accident could be covered, as could a mysterious stomach bug. If your pet experiences an injury, vomiting, diarrhea, infections, cancer, or many other illnesses that we hope never plague them, a basic policy will help cover the costs of:

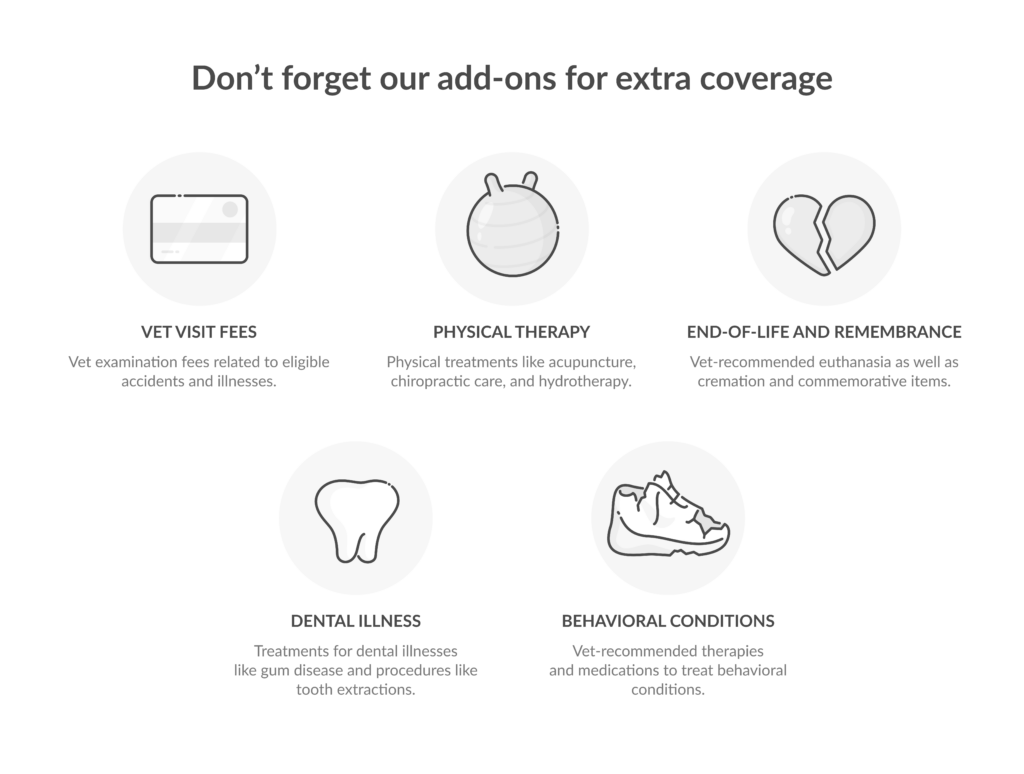

A basic policy will cover you for a lot of your pet’s health-related expenses, but not everything. That’s why pet insurance companies offer add-ons.

If you want to maximize your coverage, Lemonade offers comprehensive preventative care options, with specific coverage depending on your state, that can help with your pet’s needs from puppyhood through their senior years.

Preventative care can include coverage for procedures like spaying/neutering, microchipping, and heartworm and flea medication that help set your pet up for a healthy life.

In addition, Lemonade Pet offers optional add-ons that you can mix and match on your policy. Here’s what they can help cover:

Pet insurance can cover A LOT, but of course there are some exclusions to keep in mind. For example, your pet insurance won’t cover:

The truth is, pet insurance isn’t cheap, but neither is the cost of keeping your pet healthy.

If you’re not sure whether pet insurance is worth it, imagine the worst-case scenario-and whether you’d have the money put aside to cover the medical costs.

Lemonade’s pet insurance policies are customizable for a reason. If you can’t pay $90 every month for a policy with 90% co-insurance, that’s OK. We’ve made it so you can change your coverage to set a monthly price that suits your budget.

In our unpredictable world, it’s even more important to protect the ones you love-so you don’t have to make a tough decision down the road.

When picking the best plan for your furry friend, it’s important to ask yourself both what your pet may need and what you’re ready to pay. Don’t want to pay as much for your pet insurance? Adjust your coverages and get a lower premium. But keep in mind that, while this might save you cash in the short term, it could cause you grief in the long run. With less coverage, one accident or illness can leave you to face a difficult, painful financial decision. Picking your policy is all about balance.

It depends on how much co-insurance you opt for. Typically, policyholders get 80% co-insurance, which means your insurance pays 80%, and you’re responsible for the other 20% of your pet’s medical expenses. But the right co-insurance percentage for you depends on how much you can pay out-of-pocket if you file a claim, and how much you’re willing to pay for your insurance policy itself. Keep in mind too that co-insurance payouts are subject to deductibles and coverage limits. Deductibles (aka your contribution to the claim) are paid out annually and can either be exhausted in one big claim or met over multiple claims over the course of the year. Your claim amount will also need to fall within your annual coverage limit for your co-insurance to kick in.

Yes, the cost of pet insurance typically increases as your pet ages. Older pets are more prone to health issues and chronic conditions, which can lead to higher veterinary costs. As a result, we sometimes need to change premium prices to ensure that your pet still gets the same great coverage. And remember that filing claims will never result in a rate change to your Lemonade Pet policy.

Although it depends on your pet’s specific circumstances, pet insurance can cover your furry friend for a number of unexpected accidents and illnesses, offering you and your wallet some serious peace of mind. However, there are still some things pet insurance doesn’t cover. For instance, if your pup has a pre-existing condition before you sign up, no policy will cover any expenses associated with care for that condition. When deciding whether or not pet insurance is right for you, you should consider whether or not you’d be able to cover the out-of-pocket costs needed to protect your pet in the event of a medical emergency.

Monthly costs vary based on your pet’s species, breed, age, location, and the coverage options you choose. Our base accident and illness policies start around $10 per month, but this can vary by breed and state.

Yes, cat insurance is usually less expensive. Dogs tend to have higher premiums because they’re more accident-prone, need more emergency surgeries, and generally have costlier vet bills than cats.

Several factors affect your premium: your pet’s breed and age, your location and state, the coverage options you choose (deductible amount, co-insurance percentage, annual limits), any add-ons you select, and available discounts like multi-pet, bundle, or annual payment discounts.

You have several options to reduce your premium: choose a higher deductible ($100, $250, $500, $750, or $1,000 options), select a lower annual coverage limit, opt for a higher co-insurance percentage, or skip optional add-ons. Lemonade also offers discounts if you pay annually instead of monthly, insure multiple pets for a multi-pet discount, or bundle with other Lemonade policies.

Even young, healthy pets can face unexpected accidents or sudden illnesses that result in expensive vet bills. Pet insurance gives you financial protection and peace of mind, knowing you won’t have to choose between your budget and your pet’s health. Plus, enrolling while your pet is young and healthy means you’ll avoid pre-existing condition exclusions that could develop later. With flexible coverage options, discounts, and preventative care add-ons available, you can find a plan that fits both your pet’s needs and your budget.

No, Lemonade pet insurance doesn’t cover pre-existing conditions, any health issue your pet showed signs of, received treatment for, or had medical advice about before your policy started or during waiting periods. However, some pet insurance companies, including Lemonade, offer coverage for curable pre-existing conditions. At Lemoande, curable conditions are temporary illnesses or injuries that can become eligible for future coverage if they remain completely resolved without recurrent signs, symptoms, or continued treatment for at least 12 consecutive months.

Pet insurance costs vary widely based on your pet’s age, breed, location, and coverage choices. Lemonade starts at just $10/month for basic accident and illness coverage. You can add wellness coverage, adjust your deductible and reimbursement percentage, and get discounts for bundling with renters or home insurance. Get a quote in as little as 90-seconds to see your specific pricing. Read the full thread on Reddit

Yes, pet insurance is often worth it since one emergency can easily cost thousands. Lemonade Pet insurance starts at just $10/month and pays 50% of eligible claims instantly, so you get fast reimbursement when you need it most. You can customize coverage with wellness add-ons and choose deductibles that fit your budget. Read the full thread on Reddit

Pet insurance costs vary, Lemonade Pet insurance policies start as low as $10/month for basic coverage, with the ability to customize based on your pet’s needs. We pay 50% of eligible claims instantly through AI, offer bundle discounts, and let you add wellness coverage for routine care. Your exact cost depends on factors like your pet’s age and breed, but you can get a personalized quote in as little as 90 seconds. Read the full thread on Reddit

Dog insurance premiums vary widely depending on your pup’s age, breed, and where you live, but Lemonade policies start at just $10/month. Read the full thread on Reddit

Pet insurance premiums vary widely depending on your pet’s age, breed, and where you live. However, Lemonade Pet insurance starts at just $10/month for basic accident and illness coverage. Many pet parents customize their policies with wellness add-ons, dental coverage, or higher reimbursement percentages based on their budget and pet’s needs. Read the full thread on Reddit

Alabama, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, Florida, Georgia, Hawaii, Illinois, Indiana, Iowa, Louisiana, Maryland, Massachusetts, Michigan, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, New York, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina, Tennessee, Texas, Utah, Virginia, Washington, Washington, D.C. (not a state… yet), and Wisconsin.

*Lemonade Insurance analyzed policy rates to calculate average pet premiums as of October, 2024. This analysis is based on Lemonade’s internal data and is meant for illustrative purposes only; quotes may vary depending on individual circumstances. For states where no Lemonade data was available, the average premium was supplemented with data from https://www.insuranceopedia.com/pet-insurance/how-much-is-pet-insurance accessed March, 2025.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.