Mortgage Insurance vs. Homeowners Insurance: What's the Difference?

Does you lender require both? Let's unpack what that means

Does you lender require both? Let's unpack what that means

You’ve scraped together a down payment, found a place that you can call your own, and done the math to check you can afford the mortgage repayments, but then your mortgage provider tells you that in addition to homeowners insurance, you’ll also need private mortgage insurance.

However, it’s pretty common for mortgage lenders to require both home insurance and private mortgage insurance (PMI), particularly if you’re making a down payment below 20%.

Although the same lender might require you to purchase both mortgage insurance and homeowners insurance, they are different types of insurance and they have different purposes.

Here’s the lowdown about the differences between the two, and why you might need them both.

The difference between mortgage insurance and home insurance boils down to who’s getting protected. In the case of mortgage insurance, it’s the mortgage company; for the home insurance, it’s the homebuyer.

| Mortgage Insurance | Home Insurance | |

|---|---|---|

| Who’s protected? | Mortgage lender | Homeowner |

| When is it required? | For homes purchased with a down payment below 20%, and homes purchased with FHA or USDA loans | To secure a mortgage loan (but it’s vital even if you don’t have a mortgage!) |

| Average cost | 0.46% to 1.5% of your loan amount each year | $2,151 per year |

| What’s covered? | Covers your mortgage lender in case you can’t make your mortgage payments | Protects your home against named perils and covers your personal liability |

| Who pays? | Homeowner | Homeowner |

Mortgage insurance protects your lender in case you’re not able to afford your monthly mortgage payments and have to default on the loan.

If you get a conventional loan from a bank or other lender, it’s up to them to decide if you need it. If your down payment is very small (less than 20%), you’ll usually have to get PMI. If you finance your home purchase with an FHA loan or a USDA loan, mortgage insurance is always required.

When it comes to making your mortgage insurance payments, you’ll either pay monthly payments like other insurance products, or you can pay it off in a lump sum as part of your closing costs.

If your PMI is part of a loan from the Federal Housing Administration, it has two parts. You’ll pay an upfront premium when you complete the mortgage, and you’ll also make monthly payments along with your mortgage premium. That’s because FHA borrowers either have very low down payments, or lower credit scores, or both, making them a higher risk for defaulting on loans.

Have more questions about financing your home? Then check out our handy guide to mortgage interest rates.

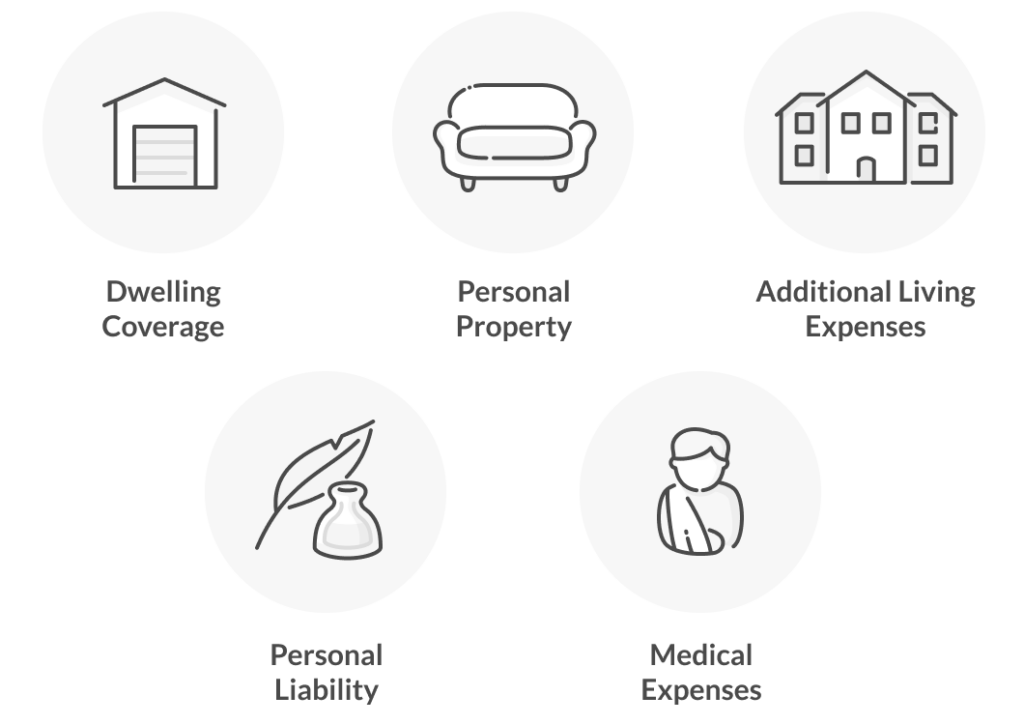

Homeowners insurance is there to protect you in case your home or your possessions are damaged, your home becomes unlivable, or you’re held liable after someone gets injured on your property.

Your home insurance is primarily for your own benefit, so that you won’t have to bear all the costs associated with these worst-case scenarios, which is why it’s a good idea to get insured even if you don’t have a mortgage and aren’t technically required to carry coverage.

Most mortgage lenders require you to get homeowners insurance, even if you have a big down payment, because if your home is destroyed or damaged, you might not be able to afford to repay your mortgage debt.

Home insurance is paid through monthly premiums. Should you need to file a claim, your insurer will help foot the bill for a covered loss, after you’ve paid your deductible.

Once your loan-to-value ratio reaches 80% (meaning you’ve paid the equivalent of 20% of your home equity), you can ask your lender to cancel your PMI loan.

The lender has to automatically end your PMI when you get to a loan-to-value ratio of 78%, or when you reach the halfway point for your mortgage loan, even if you didn’t yet get to 78% of the value of your home. So if you have a 30-year mortgage, the longest you’d have to make PMI payments is 15 years.

But that doesn’t apply to FHA loans. If you had a down payment of 10% or more, you’ll usually have to pay PMI for 11 years, but if it’s under 10% you’ll be paying PMI till you sell your home, pay off the loan entirely, or refinance to a non-FHA loan.

Another option is mortgage refinancing, either with a different lender that doesn’t require PMI, or because you’ve saved up enough to make a bigger down payment this time.Just remember that you should never stop paying homeowners insurance, even when you own your own home without any kind of home loan, because it helps you with the financial loss if you experience property damage.

Private mortgage insurance covers the cost of paying off your mortgage each month, just in case you can’t afford the payments in the future.

Exactly what your homeowners insurance covers depends on the insurance company, but in general it includes the cost of repairs to or rebuilding your home, and the loss of your personal belongings.

Each homeowners policy can cover different types of hazards, feature different limits for claims payments, and include a different deductible that you have to pay before the insurance pays out, so read it carefully. It might replace personal property for its original cash value, or for replacement cost.

Most home insurance policies include:

A homeowners policy also usually lists exactly which situations are covered by the insurance–called covered losses, hazards, or perils. The most common hazards include:

Homeowners insurance usually will not cover damage from earthquakes, floods, sinkholes, and natural events, or something you could have prevented like a sewer overflow.

Once you’ve paid at least 20% of your home equity, you don’t need mortgage insurance anymore. And since homeowners insurance is required as a condition of a mortgage, it follows that you don’t need it once you’ve paid your mortgage off, right? Not quite.

A home that’s 100% yours is great, but it isn’t immune from the named perils homeowners insurance covers, so unless you want to find yourself on the hook for 100% of the costs for anything that could happen to you or your place, you’ll want to stay covered.

Your mortgage insurance costs depend on your credit score, the size of your down payment, and the amount you are borrowing.

Typically, PMI payments are 0.46% to 1.5% of your loan amount each year, so you’d be paying about $30-$70 each month for every $100,000 you borrow. Home insurance costs depend on a number of things, including where you live, what condition your home is in, how much coverage you choose, and how big a deductible you have (the higher the deductible, the lower the monthly premium). The average cost of homeowners insurance in the US is $2,151 per year, or $179 per month.

Mortgage insurance and homeowners insurance each have their part to play in helping you step onto that ladder of homeownership.

Ready to make it happen? You can get homeowners insurance online in just a few minutes with Lemonade. Click below for a quote on an easily customizable policy.

Mortgage insurance and homeowners insurance are completely different products that serve completely different purposes. Mortgage insurance (PMI or MIP) protects your lender if you default on your loan. It does nothing for you. Homeowners insurance protects your property and covers your liability. Lenders require both if applicable: mortgage insurance when your down payment is under 20%, and homeowners insurance always. Don’t confuse them since you need homeowners insurance regardless of whether PMI applies to your loan. Read the full thread on Reddit

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.