The Mortgage Guide for the First-Time Buyer

A no-nonsense guide for those taking the plunge.

A no-nonsense guide for those taking the plunge.

If you don’t know what a closed-mortgage is, you’re not alone. But understanding the ins and outs of mortgages doesn’t need to be overly complicated. As long as you do some homework, you’ll know what to expect from the process and get the best deal for your new home.

A mortgage, also commonly referred to as a home loan, is a contract to borrow a sum of money from a lender so you can afford a house, apartment, condo, or other kinds of property.

A mortgage is a great way to get a home you can’t afford in one cash payment. But just because you’re getting a loan doesn’t mean you should plan to buy a mansion. That loan will be repaid in monthly payments, so be realistic about how much you can afford. Don’t forget that on top of mortgage payments, you will be responsible for other costs of being a homeowner, like homeowners insurance, property tax, and utilities.

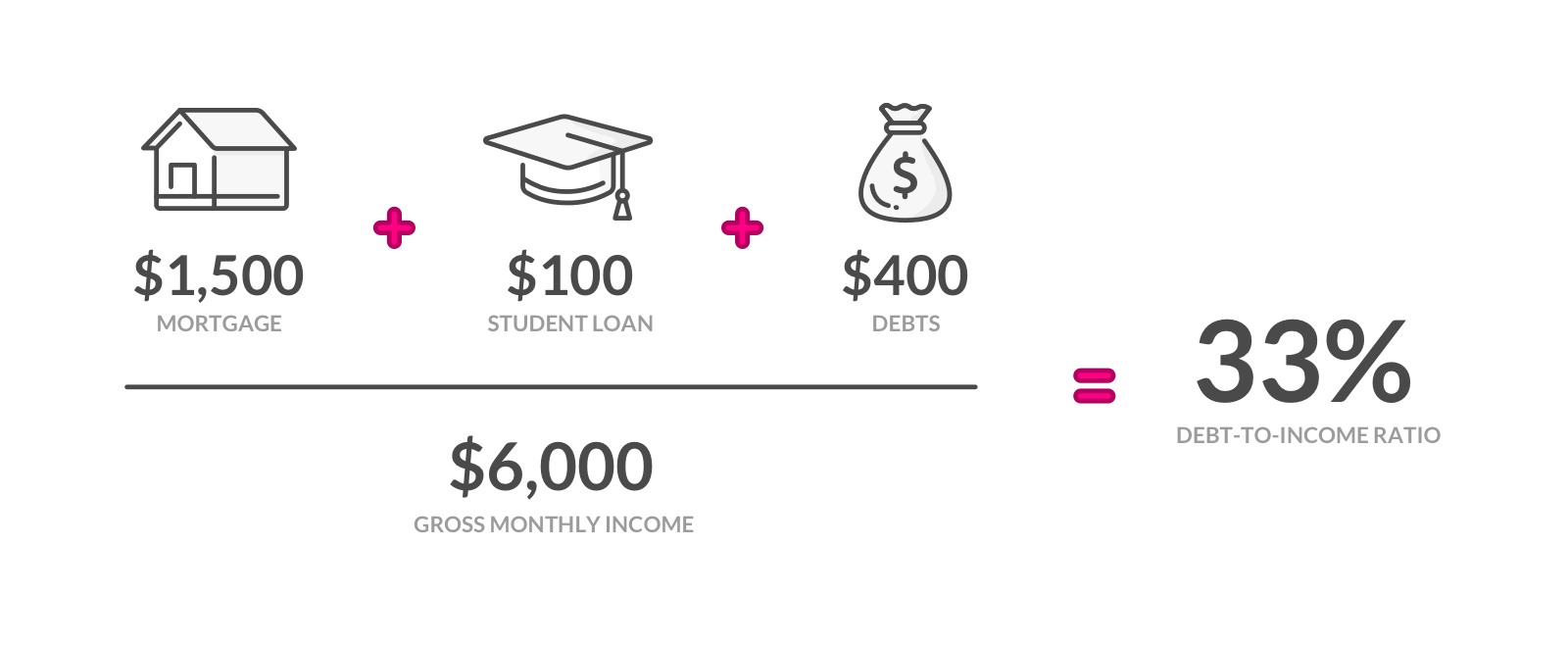

If you’re not sure how much mortgage you can afford, go for the trusted debt-to-income (DTI) ratio. This is a snapshot of your monthly debt payments divided by your gross monthly income. Lenders use this ratio to figure out whether you’ll be able to make the monthly payments needed to repay the money you plan to borrow.

So if you pay $1,500 a month for your mortgage and another $100 a month against your student loans, and $400 a month for the rest of your debts, your monthly debt payments equal $2,000. If your gross monthly income is $6,000 then your DTI ratio is 33 percent.

A debt-to-income ratio of 43 percent is typically the highest mortgage lenders will accept for a mortgage. Each lender will set its own debt-to-income ratio requirement; a 20 percent ratio is considered low, whereas the Federal Reserve considers anything above 40 percent a sign of financial stress. If math wasn’t your favorite subject in school, this DTI calculator will help you work out your own ratio.

Another way to figure out what your future monthly payments will look like is to use a mortgage calculator. It will also help you figure out how much you can afford for your down payment. Don’t feel under pressure if you can’t make a 20 percent down payment. While most lenders require a 20 percent on your mortgage, some loans (FHA loans, for example) only require 3.5 percent. Most (72 percent) first-time homeowners who took out a mortgage in 2018 made a down payment of 6 percent or less, according to SmartAsset.

Should you put down less than 20%, you’ll need mortgage insurance, which protects your lender in case you can’t make your loan payments.

If you’re wondering how much of your savings you should spend on a down payment, online mortgage broker Morty advises not to spend every cent of your savings on a down payment, to make sure you can utilize that leftover cash elsewhere.

Not to be confused with getting pre-qualified, a pre-approval is a formal offer from a lender that tells you how much they can loan you. The offer usually expires after 90 days. Getting pre-qualified, on the other hand, is a more informal process and a good alternative if you’re not ready to go through the pre-approval process.

In both cases, you approach a lender and give them documentation about your credit, debt, income, and assets. The lender then decides whether or not you qualify for a loan. If you qualify, they’ll provide you with an estimate of what they think you can afford for a mortgage. With a pre-approval, the lender will have officially verified all your documentation, so it’s more valuable than a pre-qualification.

Just because you got pre-approved from one lender doesn’t mean you have to stick with them. Online brokers such as Morty have made it super easy to get quotes from multiple lenders with relative ease-so you can compare several offers online to make sure you’re making the best choice.

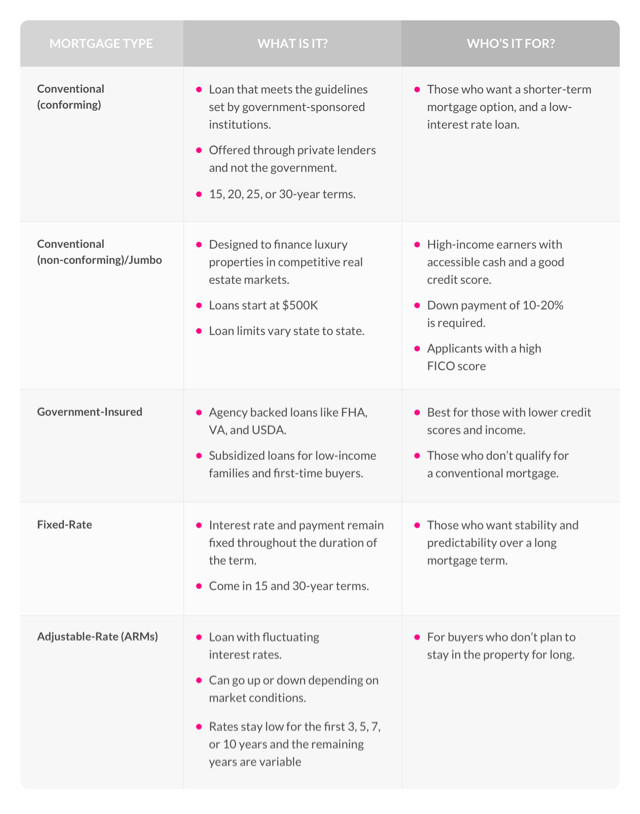

Once you sit down with a lender, you’ll have to work out the details, like choosing a fixed-rate or adjustable-rate loan.

Some people want to pay the same amount each month, while others want to make sure they pay as little as possible over the lifetime of the loan. And there will be other buyers who care about paying as little as possible up front since it’s their first home and they don’t have a lot of equity built up yet.

So, if you plan to stay in your house for the rest of your life and want to pay the same price every month, go for a 30-year, fixed-rate loan. Alternatively, if you intend for your first place to be more of a starter home and you’re prepared to pay more to get a lower overall interest rate, an adjustable-rate loan is the way to go.

Once you decide how to structure your mortgage and give your lender the green light, they’ll start a process called underwriting. They’ll gather all of your relevant financial info, send an appraiser to your home, and make sure the down payment has been deposited in an escrow account.

Btw- a mortgage lender is not the same as a mortgage broker. A lender is a bank, or financial company providing the loan, and a broker acts as an intermediary helping you to shop around for the best lender.

Shopping for the right mortgage is no small feat, but don’t be discouraged to find out that you’re still at the beginning of the process. Now you need to start the mortgage application process.

Seeking out at least three alternative quotes for a mortgage can save you thousands of dollars through lower interest rates and lower bank fees, which differ from lender to lender.

Applications will ask about your assets, employment, finances, and debt – expect it to be easier than your college applications.

There’s no impact on your credit score if you’re submitting more than one application, as long as you complete them all within a 45-day window.

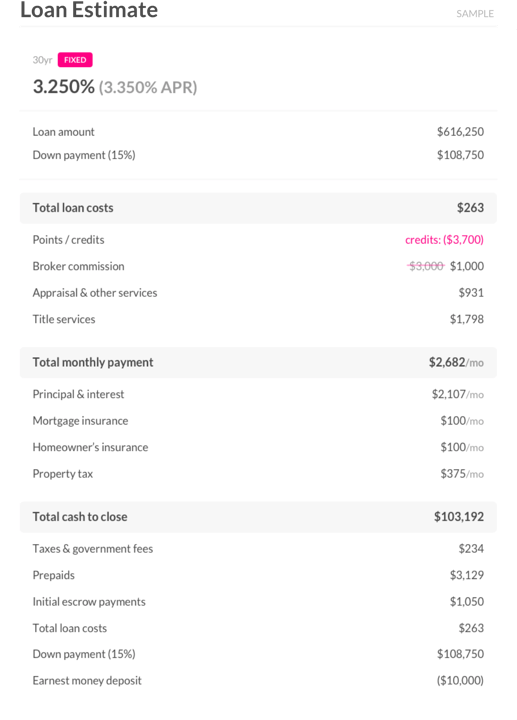

Once you’ve submitted your application and your potential lender or mortgage broker gets access to your credit score, you’ll be presented with a loan estimate. This may take them a few days to process.

The loan estimate will break down your costs, including what needs to be paid to third parties, the down payment, taxes, insurance, and lender fees, and lumps them into one figure called “cash-to-close.”

If you’re not sure what to compare to figure out which loan estimate is best, check out page three of your estimate where you’ll find the annual percentage rate (APR) and loan costs.

After you’ve compared each loan estimate, select a lender you trust. If you’re seeking more direction check out the National Mortgage Licensing System (NMLS), a database with all licensed and registered mortgage lenders. You can also check their company website for a Better Business Bureau accreditation, or look for ratings on Zillow.

Your lender will ask for a credit report, which usually costs you about $12, and an appraisal generally costing $400-$500. The bank will coordinate these for you, but you’ll be responsible for the payments.

It will take two to three weeks for your mortgage application to process, and you might be asked to provide some extra documents. Any questions you answer will be double-checked against tax records and pay stubs. Your lender will then start the underwriting process. The underwriter assesses the risk of lending you money for your property. They want to make sure you’ll make the monthly mortgage payments on time, and that your credit score checks out.

Clear to close are the magic words you’ll want to hear from your lender. It means everything checked out and your mortgage has been officially granted. Congrats!

Three days before your closing date, expect to receive the closing disclosure, which will show your closing costs (some additional costs beyond those listed in your loan estimate). Once you’ve decided to go ahead and sign the contract, it’s time to start the closing process. This involves a bunch of paperwork so have a checklist handy so you don’t forget anything.

Closing checklist:

The whole mortgage process can be lengthy and full of bureaucracy, but you got this! Comparing different mortgages and a number of quotes from lenders can make all the difference in how much you pay long-term.

If you’re at the end of the mortgage process, you deserve a well-earned break. Buying a home is one of the biggest investments you’ll ever make, but ensuring your mortgage fits your lifestyle and budget will pay-off long term.

Now all that’s left is figuring out which DIY hacks you want to use to maximize your space, and maybe consider applying for Lemonade’s no medical exam term life insurance offering–and cover your home and your family, no matter what happens.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.