4 Expert Tips on Saving for Your First Home

How to save up for a house, according to the experts.

How to save up for a house, according to the experts.

When you were younger, what did you want to be when you grow up?

Whether it was an astronaut, teacher, skydiver, or NBA star, that dream may have included your very own home. (And, if you’re like us, a gigantic trampoline and massive tree house.)

But the thing is, your 9-year-old self probably didn’t realize how hard it is to save for this first house. And now that the time has finally come (!!), chances are it’s more daunting than you thought.

Buying your very own home is something everyone dreams of, but with the rising cost of living, and monthly student loans; how on earth are you expected to start saving for your first home? It’s no help that headlines are calling out millennials for struggling to buy homes. But the truth is, millennials aren’t the only ones – every human wrestles with the idea of saving for a home, or any other big purchase far down the line.

Why? As humans, we’re not very good at prioritizing our future selves. “If given the opportunity to spend a thousand dollars now or wait until it grows larger in the future, most people will choose to spend that money now,” said Garrett Meccariello, a behavioral scientist.

It’s no wonder saving up for a home poses such a challenge, and the biggest regret among millennial homeowners is not saving more money before buying. (Nerdwallet)

To get to the bottom of how to save for your first house, we met with experts: graduates of UPenn’s Behavioral and Decision Sciences Masters Program (MBDS). They spent a year studying how to apply behavioral sciences to improve the lives of others.

So if you have questions about saving up for your first home, we have the answers — sourced straight from the experts.

Let’s get down to business: How much do you really need for a house deposit?

Ideally, you’d want to pay pretty big chunk of money upfront so you’re not left paying off your mortgage for the next 30 years. But really, who has a big lump of money hanging around?

So if you plan to put down a house deposit, there’s an unofficial rule that you should put down 20% of the value of the house – but in reality, you can also put down less.

Take note that if you decide to put down a 15% or even 10% deposit, you’ll have to pay private mortgage insurance, which is a loan made by a private business or lender as opposed to a bank.

Here are a few advantages to paying a 20% deposit or more:

1. Lower monthly payments

2. Some lenders will offer lower interest rates

3. House sellers tend to make offers for those with larger down payments

Truth is, it’s hard to save without a concrete goal in mind. In fact, studies show that if you have a savings goal without a concrete vision, it’ll soon become wishful thinking.

So a crucial first step to saving for your first home is figuring out how much you’ll need to set aside each month. How? It’s tough to know the exact number, but this’ll help you get close:

1. Research the average price of a home in your dream neighborhood, and take 20% of that number. This is your hypothetical down payment.

2. Decide roughly when you’d like to sign the dotted line. Is it 12, 24, or 34 months from now? Divide your down payment by that number.

That number is your new monthly savings goal for your home. Now that you have this goal, Garrett Meccariello advises:

“Take your future goal, and write it down somewhere visible, say, on a post-it-note. Do this often. When you see your goals in front of you, you’ll be reminded of what you want to accomplish, and it’ll be seared into your subconscious.”

So write your monthly savings goals down on a few post-its, and place them wherever you feel comfortable: on your laptop, bathroom mirror, front door, or even on your milk carton! You’ll see instant results.

This might sound like an ambitious feat, but with some financial discipline, saving up for a deposit on a house within a few years is an achievable goal.

How? First, take a good look at your finances and figure out how much you can save. The easiest way to save money is to do so automatically, according to behavioral economics. Because the truth is, many of us would rather splurge on a sushi dinner than save that money for the future. To combat this bias, MBDS alum Sakshi Ghai suggests:

“Develop a habit that’ll help you attain your future house. Push yourself to start saving every month. How do you do that? Put dollars into your bank account automatically. I find commitment devices are the most practical ways to save.”

Exhibit A: People who deposit their money in ‘commitment accounts’ end up with considerable more savings than people who spend their money freely, according to a behavioral economics study.

The trick here is to allocate a flat percentage (10%, 15%, or 20%) of your salary to your savings account the day you get your salary, rather than at the end of the month. Why? If you spend first and save second, you might run out of money before you have the chance to save.

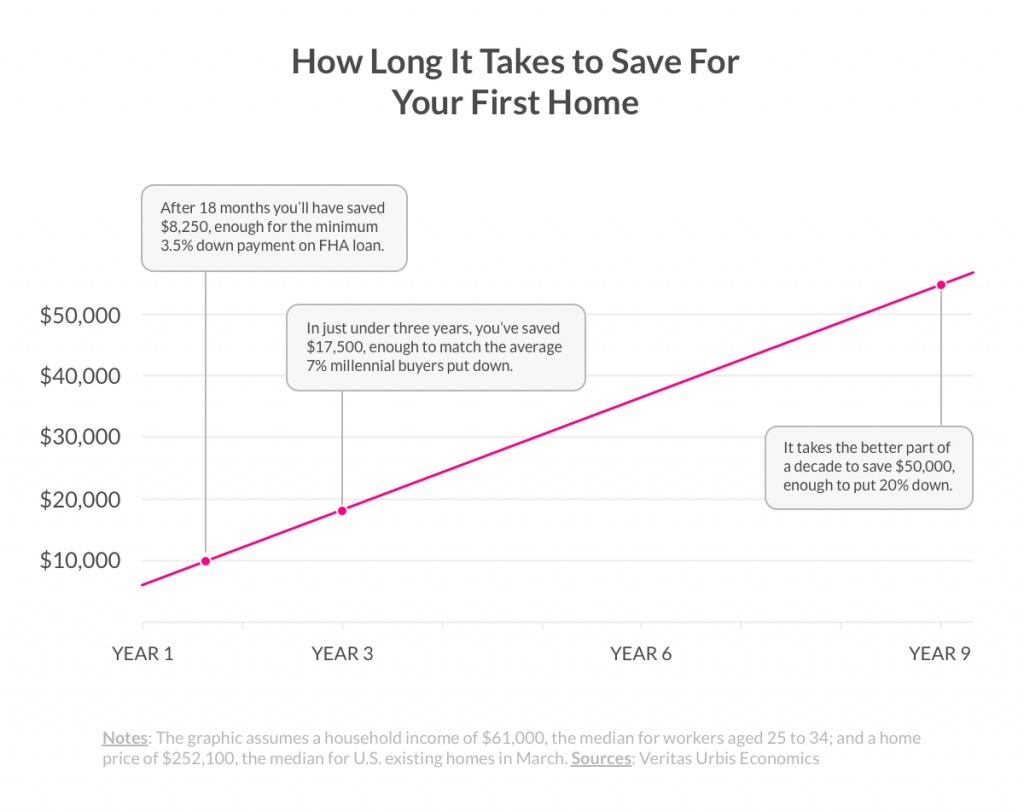

Follow this habit to a tee, and you could have enough for your down payment on a home in less than 2 years, according to Veritas Urbis Economics.

Buying a house will be one of the biggest purchases of your life. In addition to monthly mortgage payments, how are you supposed to save money after buying a house?

Being realistic here, it’s difficult (and even unproductive) to tell yourself, ‘I’m going to cut back on my spending.’ Remember what we said about needing a concrete goal? That applies to spending, also.

“If you need to cut back on your lifestyle, we find that in general, it’s easier for people to just cut things off as a category,” our Chief Behavioral Officer Dan Ariely told us.

If you tell yourself you’ll stop spending money on a single category, it’ll eliminate your need to choose on a daily basis. The decision will have already been made for you.

“Rather than allow yourself to shop unnecessarily, you should stop that behavior before it happens,” advised Garrett.

So what should you cut back on?

The best approach is to understand which activity you can give up without impacting your happiness. Is it shoe shopping, going out to dinner, or taking Lyfts?

To figure it out, take a look at your most recent bank statement, and rate your purchases on a scale of 1 to 10 (1 being, ‘I wish I never bought this,’ and 10 being ‘best purchase I made all year!’). Sort your purchases into categories, and determine which category led to the highest amount of regret. That’s your sweet spot of where you can stop spending, without compromising your lifestyle.

If you struggle with committing to this, follow Sakshi’s hack:

“Every time you save, reward yourself to give your brain an incentive to change. Be creative! This could be as simple as treating yourself to an ice cream, or your most sinful food. All you have to do is repeat this loop of saving and then rewarding yourself, and suddenly, you have a habit.”

Wrapping it all up, here’s the TL;DR of the hacks that’ll make saving for a house a bit less painful:

1. Figure out how much you can put down for a deposit on a house.

2. Calculate how much you need to save each month, write that number on post-its, and stick them everywhere.

3. When you get your monthly paycheck, automatically allocate and send a percentage of it to your savings account.

4. Cut one category of splurge purchases off entirely to financially recover after buying a house.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.