Cell Phone Insurance - Here’s What You Need To Know

Because phone theft is the last thing you should worry about.

Because phone theft is the last thing you should worry about.

TL;DR

TL;DR

Here’s an all-too-common situation: You’re finishing up happy hour with a friend, and call an Uber home. It arrives much earlier than you thought, so you scramble your stuff together and jump in the car. When you’re all settled in your seat, you reach to grab your phone, and realize it isn’t in your bag.

In panic mode, you sign into Find my iPhone, only to find your precious phone is already halfway across the city. “It must have fallen out of my bag on my way to the car, and someone picked it up,” you realize.

Will you have to shell out $800 for a replacement phone? Well, that depends on whether you have phone insurance, and what kind you have.

Getting coverage for your cell phone is probably one of the last things you want to deal with-because phone theft happens to everyone else except for you, right? But it only takes one snatch to make you wish you had the right coverage.

Considering whether to get cell phone insurance raises tons of questions. Is it worth getting phone insurance for things like screen cracks? What about water damage? And which plan is right for you?

We’re here to answer your biggest questions around phone insurance.

Phone insurance can take a number of forms-either as a standalone policy or as part of your renters or homeowners insurance (more on that below). Broadly speaking, phone insurance covers damaged, stolen, or lost phones-but what’s covered and what isn’t will depend on the type of policy you have.

Most people don’t realize this, but renters and homeowners insurance do cover your phone in certain specific circumstances. These insurance policies generally automatically cover your phone (and other stuff) for things like theft, vandalism, fire, and other damages (‘perils,’ in insurance speak). You generally won’t be covered for accidental damage or just because you misplaced and lost your phone, though.

But if a thief snatches your new phone was snatched while you’re dancing at a concert, or pickpockets you while you’re traveling abroad, your home or renters insurance will generally cover you.

When Lemonader Phil W. was traveling in Italy, his phone, backpack, and camera equipment were stolen from the trunk of his car:

“The lock on the car was popped, and everything was stolen- including all of the footage from my trip. My travel insurance denied the claim, but my Lemonade renters insurance came through and reimbursed me for everything that was lost, including my phone.”

But understanding when your home or renters insurance kicks in, and when what’s called ‘mobile phone insurance’ would, is crucial.

In addition to any coverage you’d have from your homeowners or renters insurance, there are specific, third-party plans that are just meant to cover your phone. The standalone plans might be available through your phone’s retailer (like Apple), while others are purchased via your carrier (AT&T, Verizon, etc.)

There are a few consistent differences between these specific phone protection plans and how your renters or homeowners policy would cover your cell phone.

First off, nearly all of these plans available from your carrier or retailer would cover accidental damage (such as cracked screens or liquid damage), while renters insurance does not.

On the other hand, retailers (such as AppleCare+) don’t provide insurance for phone theft in their base plan, while renters or homeowners insurance policies would protect you if your iPhone or Android is stolen.

That said, some retailer- or carrier-provided insurance plans might protect your phone against accidental loss or theft. Make sure you ask for the details of your specific policy.

Insurance provided by your cell phone carrier or manufacturer can also provide coverage for other devices as well. That’s why, in the biz, this coverage is often called “Phone & Device Insurance”.

Other gadgets that you can potentially get coverage on include:

If you’re looking to get more coverage on your gadgets, you can also look into purchasing a scheduled personal property endorsement (called Extra Coverage here at Lemonade) through your renters or homeowners insurance policy.

Renters insurance is typically more affordable than phone protection plans offered by retailers or carriers. While the price of Lemonade renters insurance start at $5/mo, mobile carrier insurance starts at $9/mo, and retailer-provided insurance starts at $11/mo. That said, to protect yourself against many possible phone-related accidents and snafus, you might want to carry both types of insurance.

Here are a few other key differences to consider:

Choosing a plan really depends on your lifestyle, habits, and how much you could pay upfront if you needed to get a replacement phone. Again, if you tend to have bad luck when it comes to your phone, you might want to have both renters or homeowners insurance and a phone-specific insurance policy from your carrier or retailer. It’s up to you.

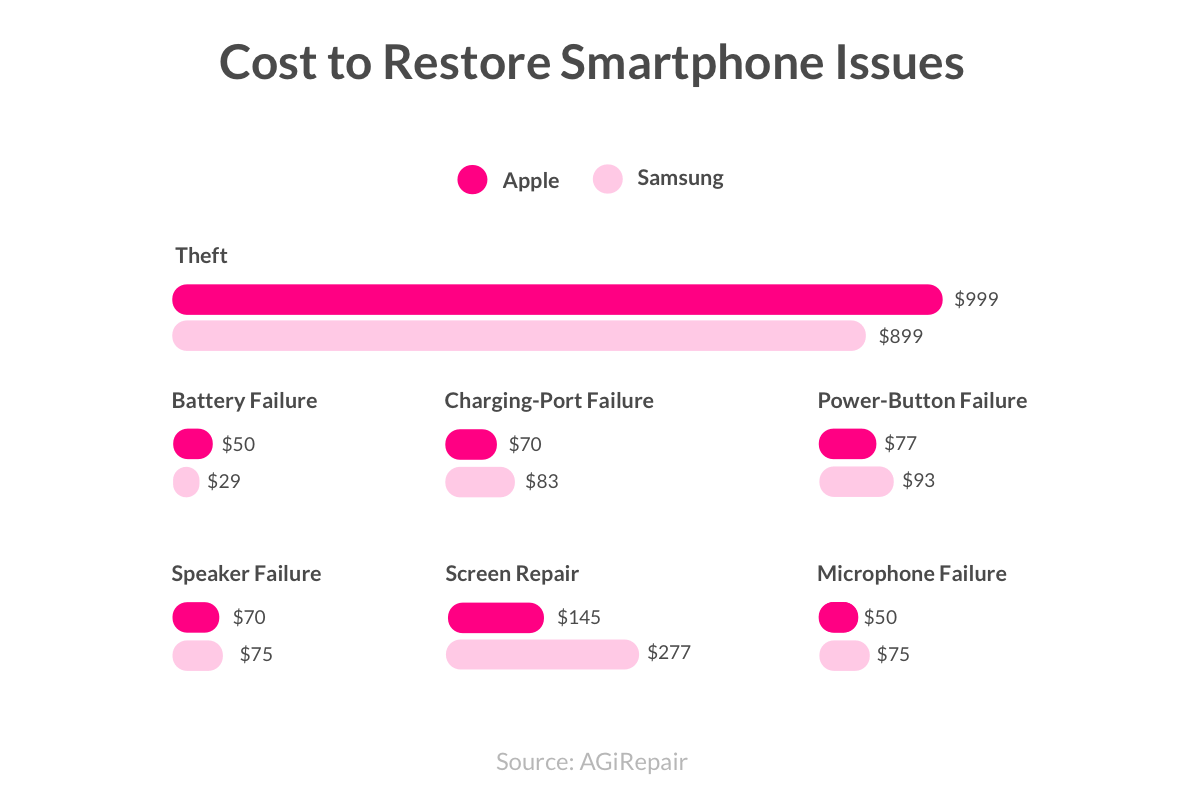

Different loss or damage types have different costs, and replacing a stolen smartphone is much more costly than fixing a smartphone screen.

So as you decide which plan is right for you, ask yourself these questions:

Bottom line: If you’d like to cover all of your stuff, including your phone, at a lower price, renters insurance is the way to go. But, if you’d like to protect just your phone against multiple incidences of accidental damage (ie cracked screen), adding on additional coverage through your phone carrier makes the most sense.

In addition to renters insurance and specific device protection plans offered by your carrier or retailer, most manufacturers also provide a phone warranty that covers mechanical or electrical problems with your phone.

If you buy a new smartphone with a two-year warranty, only to see it go kaput in six months through no fault of your own, you have the right to demand that your phone be repaired, replaced, or refunded.

An extended warranty is, well, just what it sounds like. To extend the warranty on your mobile device, you’ll want to check with your provider about the terms and conditions for applying.

Needless to say, a phone warranty isn’t the same thing as cell phone insurance. As we mentioned, your renters insurance company will cover your phone in the event of a covered peril like theft, a fire, and other damages. By contrast, your phone warranty covers only mechanical or electrical defects. It won’t cover a stolen smartphone, however-that’s where insurance comes in.

If you decide to protect your phone (and the rest of your stuff) with renters insurance, getting a policy with Lemonade is easy!

All you need to do is get a basic insurance policy, which takes less than 2 minutes: Download the Lemonade app, answer a few questions about your home, and get insured in seconds.

To make sure you’re getting enough coverage for your phone (and everything else), double check your ‘personal property coverage’ (insurance speak for coverage for your stuff) is sufficient. Otherwise, you could be left high and dry when disaster strikes.

Here’s how to estimate the value of your stuff:

1. Take 2 minutes, walk around your apartment, and take a video (or pics) of everything you care about

2. Make a list of the stuff of everything you just filmed/snapped and estimate how much each item costs

– If you have receipts, keep a pic in case you ever have to replace the stuff under warranty or have to make a claim

– For electronics and more expensive items, it’s important to know the make and model as well as when and where you bought them

3. For shoes, non-electronic kitchen items, and other stuff in bulk, just estimate what it would cost all together

4. Add this up and voilà, that’s the value of your stuff (i.e. how much personal property coverage you’ll need)

Best practice is rounding up to the nearest $10K. So if your laptop ($1,250), phone ($1,000), bike ($1,000), furniture ($5,000), and clothing ($7,000) add up to $15,250, you’ll want to get at least $20k in personal property coverage.

Phones are expensive, and after shelling out serious $$ for your sidekick, the last thing you’ll want to do is replace it if things go sour. As Lemonader Phil told us:

“When my phone and other gear was stolen, Lemonade came through with a fantastic human-driven service process, and the claim was resolved in 48 hours. That’s why I’ll always have renters insurance through Lemonade.”

Take Lemonade for a spin – it’ll take you less than 2 minutes.

Renters insurance typically doesn’t cover the cost of data recovery if your smartphone is damaged or stolen. While your policy may help with replacing or repairing the device itself, you’ll need to manage data recovery separately. To protect your valuable phone data, consider exploring data backup and protection services-like iCloud for iPhones, Backblaze, and Google Drive.

Renters insurance generally doesn’t have specific limitations on covering smartphones based on their age. Keep in mind: Older smartphones might have a lower value compared to newer models, which could affect how much you get reimbursed in the case of a covered claim, especially depending on your deductible.

Renters insurance typically does not cover the cost of identity theft protection if your personal information is compromised due to a stolen smartphone. While your policy may help with replacing or repairing the device, identity theft protection generally requires a separate service. Consider investing in a platform like LifeLock or Aura to safeguard your identity and provide additional protection.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.