Ready to hit the road? One thing’s for sure – you need car insurance before you get behind the wheel. In fact, it’s legally required in most states.

New drivers, with little to no driving history, often face higher premiums. But that changes over time. The more years you spend on the road, the more your record can work in your favor.

Here’s everything you need to know about car insurance as a new driver.

TL;DR

TL;DR

- New drivers often face higher insurance premiums because they have little to no driving history, which can make them a higher risk on the road.

- The longer you have your license, you can build your driving record which can decrease your premium if you are a safe driver.

- New drivers should look for discounts and opportunities for saving when purchasing car insurance for the first time-like bundle discounts, low-mileage discounts, and savings for safe driving habits, depending on their state.

- At Lemonade, new drivers have the opportunity to lower their premiums by practicing safe driving habits, depending on their state.

How much is car insurance for a new driver?

The average annual cost of a full coverage car insurance policy (which includes a combination of liability, comprehensive, and collision coverages) for a brand new driver can be as high as $5,900 annually, according to MarketWatch

Check out the average annual cost of minimum coverage car insurance and “full coverage” car insurance below, based on the years a driver has been licensed:

| Age | Average annual cost for minimum coverage |

|---|---|

| 16 | $2,893 |

| 17 | $2,502 |

| 18 | $2,215 |

| 19 | $1,730 |

| 20 | $1,473 |

| 21 | $1,253 |

| 22 | $1,149 |

| 25 | $893 |

| Age | Average annual cost for full coverage |

|---|---|

| 16 | $5,858 |

| 17 | $5,482 |

| 18 | $5,109 |

| 19 | $4,624 |

| 20 | $3,994 |

| 21 | $3,722 |

| 22 | $3,475 |

| 25 | $2,809 |

That said, how long you’ve been licensed is just one piece of the puzzle. Other factors that affect what you pay include:

- Your vehicle type

- Your location

- Your driving habits

- Your credit score

- Your annual mileage

- Opting for extra coverage

For example, living in an area with heavy traffic or higher crime rates can push your costs up, since the chances of an accident or claim are greater there.

How can I get car insurance for the first time?

Getting car insurance for the first time is more straightforward than it sounds. Here are the steps to figure out what you need and find the right coverage for your situation and budget:

1. Determine your coverage needs

Start by thinking through the basics:

- Your car’s value

- Your driving habits

- Your budget for monthly or annual premiums

- How much you could realistically pay out of pocket if your car gets damaged

- Your state’s minimum insurance requirements

2. Research insurance companies

Look for companies with solid reputations and real customer reviews on sites like Trustpilot or the Better Business Bureau.

3. Gather personal information

You’ll typically need to have the following handy:

- Your driver’s license

- Your car’s make and model

- Your car’s VIN number

- Your driving history (if you have one)

4. Compare rates

Get quotes from a few different providers and compare them on cost, coverage limits, and what’s actually included.

Pro tip: Use the same coverage limits across every quote so you’re actually comparing apples to apples.

5. Look for the extras

Most insurers offer similar core coverages, but some go further in ways that actually make a difference.

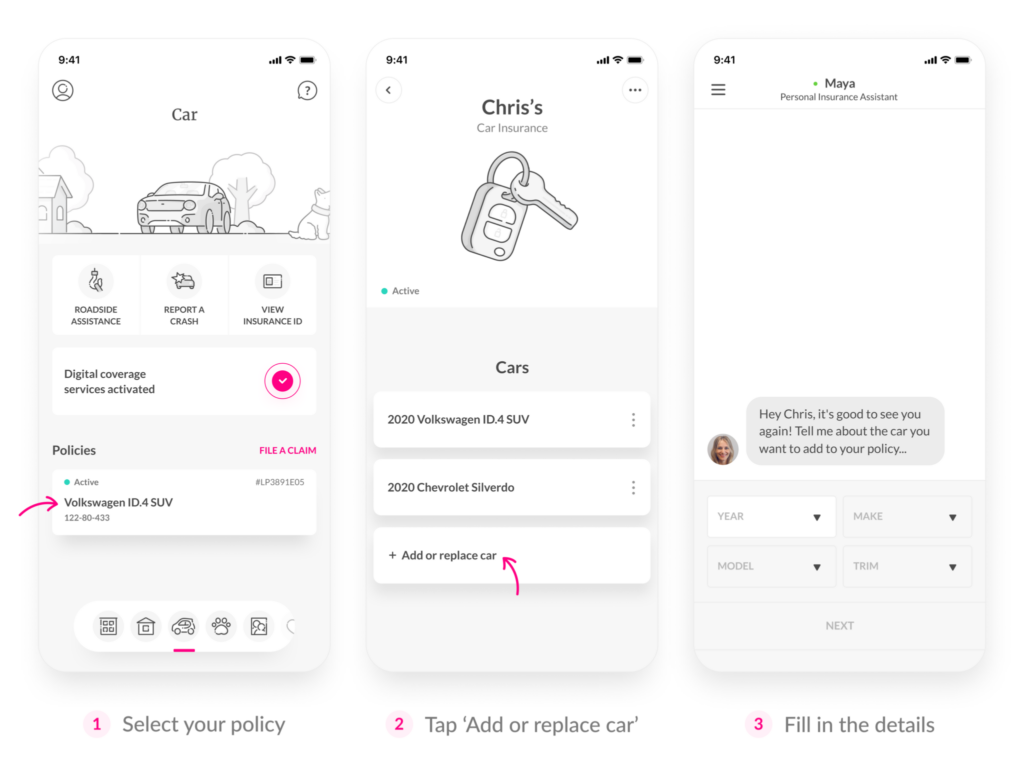

For instance, Lemonade Car offers bundle discounts – so you could save by pairing your car policy with renters, homeowners, or pet insurance.

And whether you need to update your coverage limits or file a claim, you can do it all from the Lemonade app – no hold music required.

6. Buy a policy

Once you’ve found the right fit, go ahead and make your purchase. Just double-check that your coverage limits are correct and that you know exactly when your policy kicks in.

It might feel like a lot at first, but following these steps makes it manageable. Review your policy carefully, keep a clean driving record, and look for discounts – those habits add up over time.

Why can car insurance for new drivers be so expensive?

First-time drivers usually face higher car insurance rates because insurers tend to see them as a greater risk than drivers with more experience. That might feel frustrating, especially if you’re already a careful driver.

The thing is, without a driving history to point to, there’s no track record for an insurer to go off of. So until you build one, you’re priced based on the group you’re in – not who you actually are behind the wheel.

That’s where Lemonade Car can help. When new drivers use the Lemonade app, they start building an internal record of their driving habits right away – depending on your state – which could positively affect the price you pay down the line (if you’re driving safely).

Say you just passed your road test and got your license. You don’t have years of driving history yet – but you’re starting to build it.

As you rack up experience as an insured driver using the Lemonade app, you could become eligible for discounts based on your actual driving behavior. And once that kicks in, it can bring down your average cost of coverage.

Who’s considered a new driver?

A new driver is someone getting their license for the first time – someone with limited driving experience, or possibly none at all. Without an established record, insurers don’t have much to work with yet.

New drivers typically fall into one of these groups:

- Teenagers getting a driver’s license after reaching legal driving age

- Adults who start driving later in life – like someone moving from a city to the suburbs

- International drivers who may have plenty of experience elsewhere, but are new to driving in the US

So, what’s the best car insurance company for new drivers?

We’re a little biased, but there are some real reasons why Lemonade Car is worth a look for new drivers – starting with the fact that there are multiple ways to bring your rates down from the start.

When Lemonade drivers use the app, it tracks how they actually drive – not just how people their age tend to drive. That means your premium reflects your behavior, not just a statistic.

That data feeds into your Lemonade Safety Score – a rating from 0 to 10 based on your driving habits over six-month periods. Things like harsh braking and using your phone while driving will pull your score down. Smooth, responsible driving will push it up.

Here are a few other reasons a Lemonade Car policy might be the right fit.

Low-mileage savings

If you’re mostly running short errands around town and not logging long commutes, you’re probably not driving all that much.

Your premium reflects a lot of factors – including how much and how well everyone on your policy drives. So having low-mileage drivers on your policy (especially new ones) can help keep rates more manageable. See how much you could save.

Driving behavior discounts can come later as you build your record. But even early on, driving less is a simple way to save.

Multi-car discount

If other people in your household also drive, you might be added to their existing policy – or bring your own car into the mix. Once a second car is added to a policy, everyone becomes eligible for a multi-car discount.

With Lemonade Car, that discount gets applied automatically to each car on the policy – including the first one – as soon as the second car is added.

One thing to keep in mind: all cars on your policy need to be registered under your name or your spouse’s name, and every car needs to be garaged in the state where you hold the policy.

Discounts for bundling policies

Bundle a Lemonade Car policy with another Lemonade product – like renters, homeowners, or pet insurance – and you could save on each of your premiums.

Covering your family’s cat and your 2015 Mazda3 under Lemonade? That bundle discount can take some of the sting out of the higher rates that often come with being a new driver.

More ways to save

No driving history doesn’t mean you’re stuck paying full price forever. There are other ways to bring the cost of car insurance down.

With Lemonade Car, it’s easy to adjust your coverages, limits, and deductibles to find a setup that works for your budget.

You can see in real time how different coverage choices affect your premium, so you can strike the right balance between being covered and staying within your budget.

Just keep in mind: lowering your limits or raising your deductible might save money on your premium now, but it could mean paying more out of pocket if you ever need to file a claim.

Caring about the environment

One thing we’re genuinely proud of: Lemonade Car has an environmental initiative built right in. When you enable location services on the app, we calculate how many trees to plant based on the miles everyone on your policy drives. It’s a small way of doing something good while you go about your day.

And if someone on your policy drives a hybrid or electric car, you’ll get a discount on your Lemonade Car policy. Lower emissions, lower costs – and less spent at the pump.

When your choice of car insurance can actually help the planet, that’s worth something.

Roadside assistance, on us

When you drive with the Lemonade app and enable permissions and location services, you’ll be eligible for roadside assistance at no extra charge for each car on your policy.

Lemonade’s Roadside Assistance is available anywhere in the United States or Canada.

Dead battery on a cold morning? Locked your keys inside? We’ll send help. It’s there when you need it most.

Keep in mind: you’re eligible for up to 3 services per car, at no charge, during a 6-month policy term. After that, you can still request help – it’ll just come at your own expense.

Ready to ride…

Starting out as a new driver with Lemonade Car means access to discounts, a way to build your record from day one, and coverage that can grow with you – plus a small contribution to a greener planet every time you drive.

And the “new driver” label won’t stick around forever. The more experience you build, the more your record can work in your favor – so keep those hands at 10 and 2.

Get your free quote below and see what Lemonade Car can do for you.

FAQs

What's the best insurance for a new driver?

The best insurance for a new driver often offers features like usage-based discounts, flexible coverage options, and good customer support. For example, Lemonade uses the app to track driving habits for potential discounts, which can be especially helpful when you’re just getting started.

What are some common mistakes new drivers make when getting insurance?

Common mistakes include underestimating how much coverage you actually need, skipping the step of comparing quotes from multiple providers, and missing out on discounts – like bundling your car insurance with renters insurance you already have. The good news? Reading this puts you ahead of the curve.

Can a 17-year-old get their own car insurance?

Generally, yes – but most providers require a parent or guardian to co-sign the policy. Premiums for solo teen drivers tend to be higher, so being added to a parent’s existing policy is often the more affordable route.

How can I prove I'm a safe driver to lower my premiums?

Building your driving history over time is the most reliable way. With Lemonade, you can use the app to track habits like speed, braking, and phone usage – all of which factor into your Safety Score and could help lower your premium down the line.

What documentation do I need to get car insurance as a new driver?

You’ll generally need your driver’s license or learner’s permit, vehicle registration, and a valid form of personal identification – along with details about your driving history (even if it’s limited) and the car you plan to insure.

Reddit asked, we answered

What is a car insurance card and why do I need it?

Your insurance card is legal proof you carry required coverage. You must have it while driving. Police, the DMV, and repair shops will ask for it. It shows your policy number, coverage dates, and insurer information. Most states now accept digital cards on your phone as valid proof. Read the full thread on Reddit

How do I get proof of car insurance for my North Carolina driver's license?

North Carolina requires proof of insurance to register vehicles and maintain your license. Your insurance card or a letter from your insurer serves as valid proof. You’ll need it at the DMV and when stopped by police. Digital cards are accepted throughout the state. Read the full thread on Reddit

What's the process to get car insurance?

Getting insured involves getting quotes from multiple companies, comparing coverage and prices, choosing a policy, providing required information (license, vehicle details, driving history), making your first payment, and receiving your insurance cards. The full process can take as little as a few minutes online. Coverage requirements vary by state. Read the full thread on Reddit

Do I really get 30 days of grace period after buying a car?

Most insurers automatically extend coverage to a newly purchased vehicle for 14-30 days, but the length varies by company and state. The new car typically receives the same coverage as your existing vehicle during that period. Don’t assume you’re covered. Notify your insurer promptly after purchase and confirm the details of your specific grace period. Read the full thread on Reddit

Can I get car insurance with just a learner's permit?

Yes. Permit holders can typically be added to a parent’s or guardian’s existing policy, and some insurers offer standalone policies for permit holders. You’ll generally need insurance before taking your driving test. Requirements and options vary by state, so check with insurers in your area for what’s available. Read the full thread on Reddit

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share