9 Steps to Buying a Home

From browsing Zillow to closing on your dream home, we've got you covered!

From browsing Zillow to closing on your dream home, we've got you covered!

There’s no manual when it comes to buying a home. At times it can feel like crawling through an obstacle course, with so many twists, turns, and traps.

At Lemonade, we’ve seen first-hand how confusing the process can be for our homeowners insurance policyholders. What’s a home inspection all about, and what might it turn up? How do you deal with the bank, which will be loaning you a pretty intimidating sum of cash?

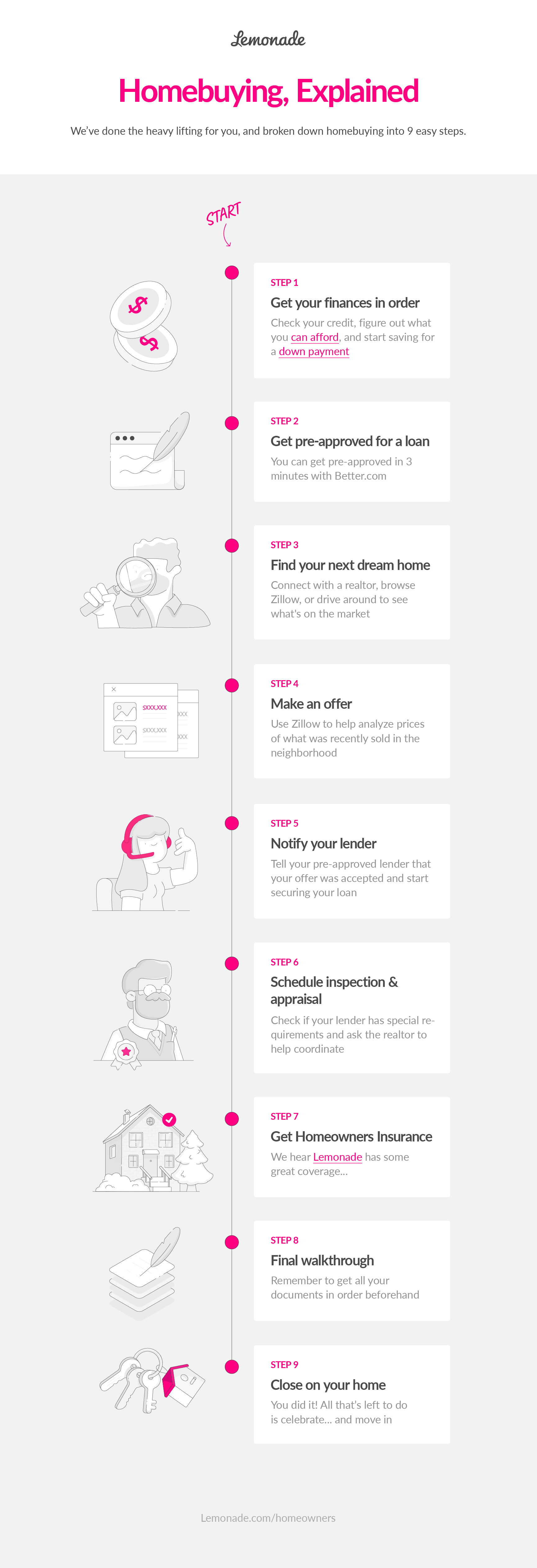

While every home buying journey is unique, there are 9 major steps to keep in mind. We’ll break them down below-including in the form of a handy graphic that you’re free to print out and frame, naturally.

So you’ve decided it’s time to buy!

Before you start your hunt, you should always make sure you’ve been through a credit check. You’ll also want to have a good idea of what sort of down payment you’ll be able to put down.

Getting pre-approved for a loan gives you a clearer picture of how much house you can afford. Our friends over at Better.com can help you get pre-approved in mere minutes.

Now comes the fun part-actually browsing for your dream home. Start with Zillow and narrow down your search based on location, price range, and other features (condo VS apartment or townhome, number of bedrooms, and so on). Realtor.com and Trulia offer similar services (and there are also sites that focus on foreclosed properties).

Alternatively, you can get a real estate agent on board. Either way, you’ll want to do some research and get an idea of how much the type of home you want is selling for in your chosen location.

Now might be a good time to figure out how many other potential buyers there are to help you determine how much to offer. If you’ve been reading the real estate news in 2020 and 2021, you’ll know that it’s a pretty hot and competitive market out there. You can either ask your real estate agent to find out, or inquire with the listing broker.

You’ll also want to decide on your earnest money, which acts as an escrow during the home buying process.

Okay, so your offer was accepted by the seller! It’s all looking very… real.

But before moving any further, it’s time to notify your lender. Tell them your offer was accepted, and now it’s time to move forward with your home loan. You’ve already been pre-approved, which is great, but that was essentially hypothetical. Now your lender has to approve the actual mortgage amount you need to borrow for a specific property… and this is just the start.

At this stage, your lender will want you to book a home appraisal. Before the bank gives you a loan, they will want to make sure the price you agreed to pay for the house is close enough to its actual worth. Fair enough.

If the appraisal price is equal to or higher than the price you agreed to pay, you’re on the road to homeownership!

But if the appraisal comes in significantly lower than what you planned to pay for the house, your bank will have some questions.

The bank or lending service is investing in your new home, in a way. If they think they are investing too much in a property, they could lose money down the line-if the property forecloses, for example. If your appraisal is lower than what you’re planning to pay, you’ll probably want to speak with the owner and try to negotiate the property price down.

Once you’re done with the home appraisal, you’ll need to schedule a home inspection. This is as much for the lender as it is for you. It’s imperative you make sure your future abode is structurally sound and has no major, sneaky issues that could come back to haunt you.

It’s easy to get confused about when to get homeowners insurance: You know you need it, but there’s a small window where you can actually buy it.

Homeowners insurance is part of your lender’s condition to grant you a mortgage, because it offers them extra protection if anything happens to the property. But it’s also smart for you, and your wallet.

Homeowners insurance can help cover the costs of expensive damage in and around your property-here’s more info about the specifics, in plain English. Lemonade makes it extremely easy to get coverage tailored to your specific needs-just click the button below to get your quote started in minutes.

You’re on the home stretch! Before you head out make sure you bring with you your final contract, inspection summary, and any other relevant documents.

Now’s your chance to take a last look around before closing. This is usually done by the buyer (i.e., you) and the real estate agent. Make sure everything is in order, and that the buyers did everything they said they would-whether it’s repairs or slapping on a new coat of paint. If there are any issues, now’s the time to get them sorted, so don’t be shy. Speak now, or forever hold your peace (and, you know, suffer pesky roof leaks).

The day you’ve been working towards has finally arrived. Closing day is when you get the keys and legally own your home. This day will be listed on your purchase agreement contract and it’s also the day your home insurance will come into effect.

On closing day, you’ll pay any remaining closing costs, and sign a mortgage or deed of trust securing your mortgage, and the seller will sign documents to transfer property ownership.

Welcome home! Now you just have to unpack-and wouldn’t you know that we’ve got a whole move-in checklist for that, too…

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.