How to Switch Car Insurance in Five Easy Steps

Unhappy with your current insurer? Good news: You're not stuck.

Unhappy with your current insurer? Good news: You're not stuck.

Switching your car insurance policy is easy and can be done at any time—either at renewals or mid-policy term—by contacting your current insurer.

Read on for five straightforward steps to make the switch smoothly and ensure you’re covered when you get behind the wheel.

Because sometimes the grass actually is greener on the other side.

TL;DR

TL;DR

Here’s five easy steps to switch car insurance providers.

A Forbes Advisor survey found that for 58% of drivers, the main reason for switching car insurance companies was to save money. But smart shoppers know to focus on more than just getting the cheapest car insurance premium.

Good car insurance combines the coverage options you need with a rate, deductibles, and limits you can afford. But to go from good to great, look for an insurer who offers a seamless experience. (Did we mention that Lemonade offers super fast claims resolution, and a mobile app—where you can easily customize and manage your Lemonade policies?)

Take the time to research and compare car insurance options with the help of our complete guide here.

Once you’ve done your homework, it’s time to make the switch.

Buy your new policy before canceling your old one to avoid a lapse in coverage. And more importantly, make sure the date that your new policy goes effective is the same day that your current policy’s coverage ends.

We get it, breakups can be hard. (Tell your ex-insurer you can still be friends.) But really, don’t forget to cancel with your current insurance company.

Car insurance providers often require you to cancel your policy over the phone. But in some cases you can mail in a cancellation letter, or speak with your insurance agent in person. Request a cancellation letter from your current insurer, so you don’t wind up having your old policy—and payment requirements—renew.

Keep in mind that depending on your insurer and payment plan, you might not get fully reimbursed for the remainder of your policy if you cancel mid-term, and might even have to pay a cancellation fee.

FYI: At Lemonade Car, you can easily cancel your policy at any time on the Lemonade app, and you’ll get reimbursed for your unused premium, without fees.

In nearly every state in the US you’re required to carry up-to-date proof of insurance coverage to get behind the wheel. So once you make the switch, make sure to also switch out your proof of insurance by the time your new policy starts.

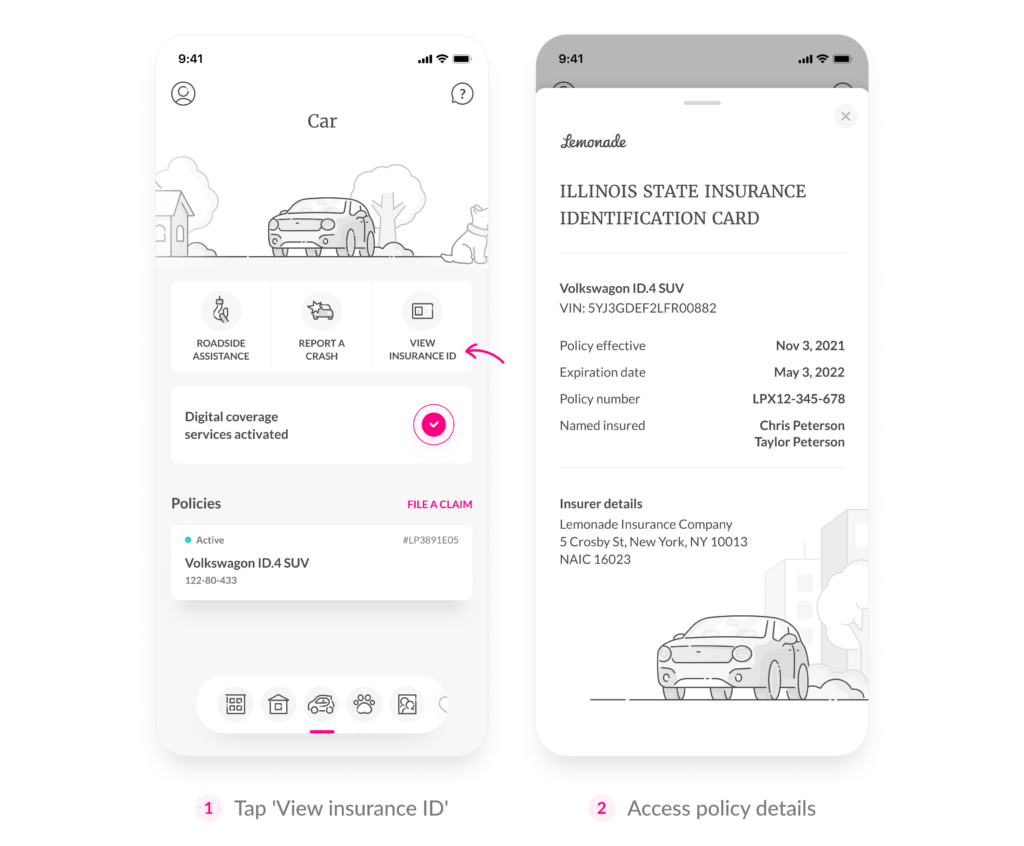

Your new car insurance company will most likely send you proof of insurance for your new policy in the form of an ID card, either by mail, email, or on a mobile app.

When you buy a Lemonade Car policy, you can access your insurance ID card digitally on the Lemonade app. The law doesn’t require a hard copy, but if you want to print a copy of your insurance ID card, you can do that via our app.

Do you have a loan on your car, or a lease? If so, you’ll need to share proof of your new car insurance coverage—or ask your new car insurance provider to—with your car’s lienholder or leasing company.

When you buy a Lemonade Car policy, we’ll automatically notify your lienholder or leasing company, without any hassle. Keep in mind that you’ll likely need to include both comprehensive and collision coverage on your policy—usually with a required minimum deductible—if you have a loan or lease on your car.

As your life changes, what you’re looking for in a car insurance company might, too. There are so many reasons—besides simply looking for better rates—to consider switching from your current policy, including:

You can switch any time! There’s no need to wait until policy renewals come around. And if you’re switching from another insurer to Lemonade, you can usually set your Lemonade Car policy’s effective date to start as early as the following day.

No matter what date you schedule your new policy’s coverage to start: Set a reminder, and make sure your current coverage is effective until then to avoid a lapse in coverage, which can have major legal and financial repercussions.

Glad you asked! Getting your free quote is easy, and coverage starts at just $30/month.

Lemonade Car protects you, your car, and your wallet, while connecting your coverage to causes that matter. When you get your first policy, you choose a cause you care about, and Lemonade donates to nonprofits supporting those causes. We also offset carbon emissions from your driving through our tree-planting program.

Did you know that we also offer Homeowners, Renters, Pet, and Life Insurance? You’ll become eligible for our bundling discounts, and have the power to customize and manage each of your Lemonade policies through the same app you use for Lemonade Car.

Let’s drive.

To switch your car insurance, you will need your driver’s license, current policy details, and proof of insurance. Having these documents ready and available will streamline the process.

Switching car insurance typically does not affect your credit score. However, some insurers may perform a soft credit check when providing you with a quote.

Changes in your driving record can impact your new car insurance premiums. You need to ensure your new provider knows about any recent changes.

Your new car insurance policy can often become effective the next day after purchase. You will need to confirm the start date with your new provider to avoid any gaps in coverage.

Another thing to keep in mind is an open claim can be a part of your claims history. This means that your new provider may factor this into your premium, leaving you with a higher car insurance rate.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage and discounts may not be available in all states.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.