What You Might Be Getting Wrong About Your Homeowners Insurance

We clear up some of the most common misunderstandings around homeowners insurance, so that you can sail into the future with confidence.

We clear up some of the most common misunderstandings around homeowners insurance, so that you can sail into the future with confidence.

You managed to afford a down payment, get approved by a lender, and find someone willing to sell you a home. And you successfully navigated the sign-up process for homeowners insurance.. but that doesn’t mean that you’re automatically an expert about what your policy entails.

Homeowners insurance is a contract between you and your insurance company that covers you in a bunch of different situations. Your policy also covers temporary additional living expenses if your place becomes unlivable due to a covered loss.

But beyond those basic facts, insurance can be confusing, and you’re not alone with your questions.

In fact, we hear a lot of the same ones over and over again from smart homeowners like you all the time. So we asked our favorite experts-the humans of Team Lemonade-to demystify the most commonly misunderstood parts of a homeowners insurance policy.

Here’s what we learned.

If a thunderstorm sends a favorite tree on your property crashing through your bedroom window, your policy will cover the damage. But if you buy a policy after that accident, expecting it to help? No dice.

The good news, though, is that being a proactive homeowner and taking steps to curb the risk of tree damage to your property, you can prevent such an accident from happening.

It seems obvious, but don’t forget: Your policy only covers you for losses that occur after policy’s start date. Which means you can’t buy one after something happens-you have to have a policy in place ahead of time, for exactly these types of situations.

There are a few different types of coverage options for when something bad happens. When it comes to Dwelling Coverage (Coverage A) and Other Structures (Coverage B), most homeowners have what’s known as an ‘open perils policy.’

This simply means that, unless something is explicitly excluded in your policy, it’s covered. Pretty sweet, right? So if a freak accident causes damage to your home’s roof, that would be covered under Coverage A. If some other random mishap ripped apart a fence on your property-as long as whatever caused the damage isn’t specifically excluded in your policy-then you’d also be covered (under ‘Other Structures,’ Coverage B).

The alternative to ‘open perils’ are ‘named perils,’ which refers to a list of 16 specific perils that are covered by your insurer. These types of perils include fire, explosions, smoke, and theft. If something isn’t specifically listed as a covered peril, well… it isn’t covered.

Under your HO3 policy, the actual stuff you own, like furniture or electronics or a vinyl collection-aka your Personal Property (Coverage C)-is covered under named perils.

How does this work in practice? If a small kitchen fire destroys everything plugged into your outlet, you might be left with hundreds of dollars of food spoilage because your fridge won’t work. The good news is you’re covered, since fire is a peril specifically named on your policy!

What happens if your fridge breaks unrelated to a covered peril? Sorry, but you’re out of luck. An appliance that is simply faulty, or breaks down, isn’t a peril, so it isn’t covered by your homeowners policy (although it may be worth checking with the manufacturer to see if you’re covered under their warranty).

Speaking of your appliances, don’t forget that your homeowners insurance is not a maintenance policy…

But, if you want to add on extra protections, you can purchase Equipment Breakdown Coverage (EBC). Also known as Appliance Coverage, this is an endorsement to complement and enhance your homeowners insurance and provide coverage for many other types of damage. So, if there’s a mechanical or electrical breakdown, EBC may provide up to $100,000 in coverage on almost any home appliance.

The same way you get regular oil changes for your car, you should get your plumbing and appliances checked to make sure they’re in good working order.

Homeowners insurance covers not only damage to your stuff, but also offers reimbursements for temporary living costs if a covered loss displaces you from your home while repairs take place. This type of coverage is known as Loss of Use, and it may even cover the extra $$ you have to spend on food and laundry. Homeowners insurance, to the rescue!

So if a kitchen fire means you can’t live in your home for some time, you’re covered. (But if you’re claiming loss of use because your neighbors party too hard, we can’t help you, since ‘proximity to bad dance music’ isn’t going to be covered under any policy. Sorry.)

Sorry, what? ‘Bailee’ is just a fancy word to describe a person or company who’s in temporary possession of things you own. In other words, you still own the property, but someone else is in charge of keeping it safe for the moment.

‘No benefit to bailee’ means your insurance won’t cover damages that happen when your property is in the possession of a third party, like an airline or a moving company.

So if your iPad gets damaged or stolen while your movers load it onto their truck, you won’t be able to file a claim with your insurance company. The good news is, airlines and moving companies usually have their own policies that will cover damages to your property while it’s under their care.

Here’s the plain truth about earthquake and flood insurance: It’s not included in your homeowners policy. In most states, you can get it as an add-on to your policy, and buy it from a carrier that specializes in those specific coverages.

Your base homeowners insurance policy doesn’t cover earthquakes, landslides, or really any kind of damage that occurs directly due to earth movement. You might not need it-it depends on where you live and what the structure of your home is like. Even in the state of California, where insurance regulators mandate that insurance companies provide an add-on, only 13% of residents purchase earthquake insurance.

As for flood insurance, it also depends on where you live. FEMA can let you know if your state requires flood insurance by law.

An insurance deductible is an amount of money you choose when purchasing a policy that will be subtracted from any future claims payouts.

Think of a deductible as your participation in the damage or loss. You’re saying, “I commit X dollars to any claim on future losses or damages, and my insurance company will cover the rest.”

When signing up for a homeowners insurance policy, you’ll be asked to choose a deductible. For a homeowners policy, these typically range from $1,000 to $2,500. What you’re choosing here is your participation (the amount subtracted from a claim) in the event that something happens to your stuff.

Here’s how that works if you file a claim:

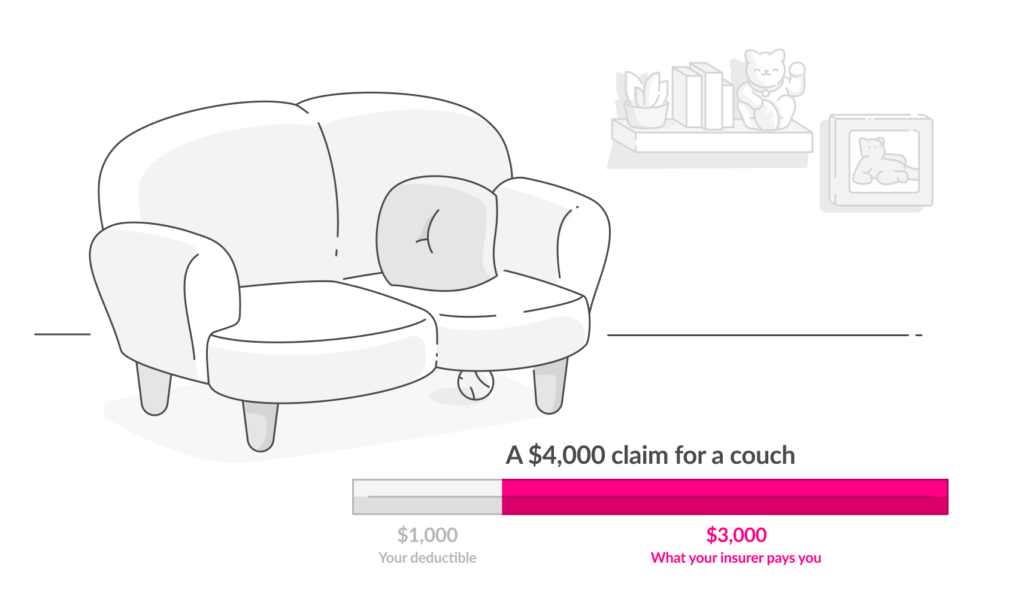

1. You chose a deductible of $1,000 when you bought your policy

2. Later on, you file a $4,000 claim for a stolen couch

3. If the claim is approved, your insurer will pay you $3,000 ($4,000 minus your $1,000 deductible) – if you don’t replace it, your insurer will likely pay you the actual cash value of your couch, which reflects its depreciated worth

4. Keep in mind, this isn’t an annual deductible that you meet-it applies to each claim you file.

The natural follow-up question to this deductible business is: If you’re already paying a monthly premium, why do you still have to participate in the claim? Well, deductibles exist to make you be a bit more careful with your stuff, and keep the cost of policies low for everyone.

So when your claim is approved but you notice there’s $1,000 “missing,” remember, that’s your contribution. You cover the deductible, and the insurance company covers the rest.

Still not feeling like an insurance pro? Don’t worry, you don’t need to be an expert on all things insurance when you have a team of experts you can rely on.

If you want to learn more, check out our ultimate guide to homeowners insurance.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.