8 (Little Known) Reasons You Need Renters Insurance

Here's why you might actually need renters insurance.

Here's why you might actually need renters insurance.

With inflation sending prices soaring, millions of renters are weighing which expenses are truly essential. Renters insurance is one worth keeping. Many landlords and property managers require it, but even when it’s not mandatory, the case for coverage is strong.

Here’s eight reasons why.

The average cost of renters insurance is around $23 per month as of 2026, with Lemonade’s renters policies starting as low as $5 a month. For that, you get personal property coverage, liability protection, and more – all in one policy.

Real-world example: Marcus pays $12 a month for his Lemonade renters insurance policy. In October, his apartment is broken into and his gaming console and other gear are stolen. He files a claim through the Lemonade app and gets reimbursed after his deductible. Without renters insurance, the entire loss would have come out of his own pocket – more than eight years’ worth of premiums, gone in one incident.

| Who | Marcus, renter in a mid-size city |

| What happened | Apartment break-in, gaming console and gear stolen |

| Monthly premium | $12/mo |

| Deductible | $250 |

| Claim payout | $950 |

| Annual premium cost | $144 |

| Outcome | Covered. Nearly 8x his annual premium recovered in a single claim |

Most renters don’t realize their personal property coverage travels with them. If your phone is stolen from a coffee shop or your laptop goes missing from a co-working space, your policy covers it. The same applies if your kitchen catches fire or your sprinklers flood your apartment.

Real-world example: Maya, a graphic designer, leaves her laptop at a co-working space while grabbing lunch. When she returns, it’s gone. Because her renters insurance includes off-premises personal property coverage, she files a claim and gets reimbursed for the replacement cost minus her deductible. Most renters don’t realize they’re covered outside the home until it happens to them.

| Who | Maya, graphic designer |

| What happened | Laptop stolen from co-working space |

| Item value | $1,800 |

| Where it happened | Off-premises (co-working space) |

| Covered? | Yes, off-premises theft is a named peril |

| Out of pocket | Deductible only |

The average two-bedroom apartment in the US contains about $30,000 worth of electronics, clothing, jewelry, bikes, and more, according to US News. If a fire, lightning strike, windstorm, theft, or vandalism wipes out your belongings, personal property coverage covers the cost of replacing them. Without it, you’re paying out of pocket.

Once you decide to get covered, take a quick inventory of your stuff to choose the right coverage amount. Lemonade makes it easy to view and adjust your limits through the app or website.

Real-world example: Jordan never thought much about the value of his stuff until he listed it out. When a pipe burst and damaged most of it, his personal property coverage covered the replacement costs. What renters insurance pays for in situations like this is exactly what most renters assume they’ll never need — until they do.

| Item | Estimated value |

|---|---|

| MacBook | $1,500 |

| Camera equipment | $800 |

| Clothes and shoes | $600 |

| TV | $400 |

| Bike | $300 |

| Total | $3,600+ |

| Outcome | Covered under personal property after burst pipe |

Landlord insurance and renters insurance cover different things. Your landlord’s policy protects the building and any property they own, not your belongings. If a fire or flood damages your furniture, electronics, or clothes, that’s on you unless you have your own policy.

Real-world example: A fire broke out in Priya’s building due to faulty wiring in a neighboring unit. The landlord’s policy covered structural repairs — but not a single item Priya owned. Her neighbor, uninsured, replaced everything out of pocket.

| Priya (insured) | Neighbor (uninsured) | |

|---|---|---|

| What happened | Building fire from neighboring unit | Same |

| Landlord’s insurance covered | Building structure | Building structure |

| Personal property covered? | Yes, via renters insurance | No |

| Out of pocket | Deductible only | ~$8,000 |

If your dog bites someone, your renters insurance liability coverage has you covered – whether the incident happens at home or at the park. There are two exceptions: your dog has a documented bite history, or is classified as a high-risk breed.

Real-world example: Sam’s dog Biscuit nipped a guest hard enough to draw blood. The guest went to urgent care. Sam’s liability coverage paid the full bill – Biscuit had no prior bite history and wasn’t a high-risk breed. Sam paid nothing out of pocket.

| Who | Sam and Biscuit |

| What happened | Dog bite, guest required urgent care |

| Medical bill | $1,800 |

| Bite history | None |

| High-risk breed? | No |

| Covered? | Yes, liability coverage applied |

| Out of pocket | $0 |

If a covered event, like a kitchen fire or a flood from a neighbor’s unit makes your apartment uninhabitable, your policy may cover loss of use. That means temporary housing and basic living expenses until you can move back in.

Real-world example: The tenant upstairs left their bathtub running while on vacation. The resulting flood made the apartment below uninhabitable for three weeks. Loss of use coverage covered the hotel stay and additional meal costs in full.

| What happened | Upstairs neighbor flooded the unit |

| Temporary housing | Extended-stay hotel, $120/night |

| Displacement period | 3 weeks |

| Hotel total | $2,520 |

| Additional meal expenses | Covered above normal budget |

| Covered? | Yes, loss of use coverage applied |

| Out of pocket | $0 (beyond deductible) |

If a guest gets hurt at your place, your policy can help. For smaller claims (under $5,000), your medical payments to others coverage kicks in without any liability determination needed. If the situation escalates to a lawsuit, your liability coverage steps in. More on that below.

Real-world example: During a dinner party, a guest slipped on a wet kitchen floor and sprained her ankle badly enough to need an ER visit and specialist follow-up. Because the bill came in under the medical payments limit, it was covered without any lawsuit or liability determination required.

| What happened | Guest slipped on wet kitchen floor |

| Total medical bill | $3,200 |

| Coverage type | Medical payments to others |

| Coverage limit | $5,000 |

| Lawsuit filed? | No |

| Covered? | Yes, in full |

| Host’s out of pocket | $0 |

Liability coverage protects you if someone claims to be injured due to your actions or negligence. It covers legal fees if you need a lawyer and pays damages you’re found liable for. Coverage typically starts at $100,000 – which can make a significant difference when legal and medical bills start adding up.

Not sure how much renters insurance you need? Your lifestyle is a good place to start. Consider your risk exposure, profession, and whether you frequently have guests.

Real-world example: A friend trips over a rug, fractures their wrist, and incurs $8,000 in medical bills. After medical payments coverage handles the first $5,000, they file a civil lawsuit for the rest plus pain and suffering. Liability coverage steps in to cover legal defense and the settlement.

| What happened | Guest tripped, fractured wrist |

| Total medical bills | $8,000 |

| Medical payments coverage | $5,000 (applied first) |

| Lawsuit filed? | Yes, for remainder plus damages |

| Liability coverage limit | $100,000 |

| Covered? | Yes, legal fees and settlement covered |

| Out of pocket | $0 |

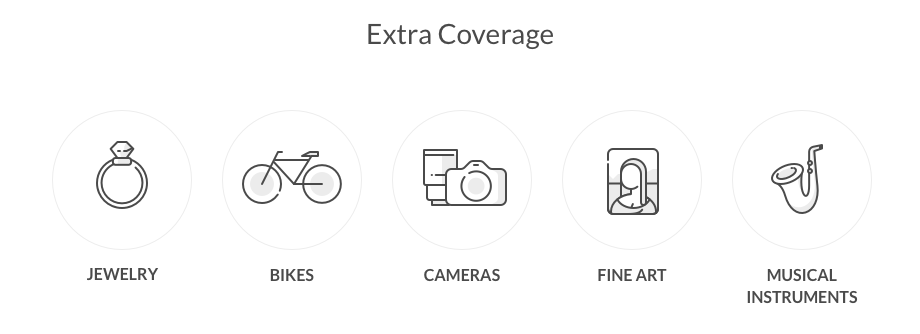

Your base policy covers a lot, but some of your most valuable items and common household risks need a little extra.

Extra Coverage (scheduled personal property): High-value items like cameras, jewelry, and fine art can be added to your policy as scheduled items. This coverage protects them from almost anything, including accidental loss – something a standard policy doesn’t cover. It typically costs just a few extra dollars a month.

Real-world example (Extra Coverage): A photographer schedules a $3,000 camera lens as a separate item under Extra Coverage. When it’s stolen from her car, she receives the full $3,000 back with no deductible. A standard policy alone may not have covered the full replacement cost.

| Item | Camera lens |

| Value | $3,000 |

| What happened | Stolen from car |

| Coverage type | Scheduled personal property (Extra Coverage) |

| Covered? | Yes, in full |

| Deductible | $0 |

Equipment Breakdown Coverage: A standard renters policy covers your electronics and appliances against named perils like fire and theft, but not mechanical or electrical failure. Equipment Breakdown Coverage fills that gap.

Adding people to your policy: A standard policy automatically covers household members related by blood, marriage, or adoption. Significant others need to be added as an additional insured — there’s a charge for this, so it’s sometimes more cost-effective for each person to get their own policy. Roommates are not covered under your policy and need to get their own.

Real-world example (Equipment Breakdown): Tom’s in-unit washing machine stops mid-cycle. A technician diagnoses an electrical motor failure — not a named peril, so not covered under a standard policy. But Tom had added Equipment Breakdown Coverage, and the repair was covered in full.

| Item | In-unit washing machine |

| What happened | Electrical motor failure |

| Covered by standard policy? | No, not a named peril |

| Coverage type | Equipment Breakdown Coverage (add-on) |

| Repair cost | $600 |

| Covered? | Yes |

Landlords and property managers can require renters insurance as a condition of your lease. Even when it’s not required, carrying a policy protects you from significant out-of-pocket costs after a covered loss – whether it’s a burst pipe, a kitchen fire, or a stolen phone.

There’s no one-size-fits-all answer. You’ll want to think carefully about your needs across personal property, loss of use, medical payments, and liability coverage. For high-value items, it’s worth exploring your Extra Coverage options.

Getting covered takes just minutes with Lemonade’s online sign-up.

Renters insurance is not required by federal or state law, but many landlords and property managers include it as a mandatory condition in lease agreements. Even when it’s not required, carrying a policy protects you from significant out-of-pocket costs after a covered loss.

A standard renters insurance policy covers personal property against theft, fire, vandalism, and certain water damage; liability if someone is injured in your home; medical payments to injured guests; and loss of use if your apartment becomes uninhabitable due to a covered event.

Yes. Most renters insurance policies cover personal property theft that occurs away from your home, including items stolen from your car, a coffee shop, or while traveling. Coverage limits may apply depending on your policy.

The national average cost of renters insurance is around $23 per month as of 2026. Lemonade’s renters insurance policies start as low as $5 per month, making it one of the most affordable forms of personal insurance available.

Yes. Renters insurance liability coverage typically covers dog bite incidents whether they occur at home or in a public space. Coverage may be excluded if the dog has a documented bite history or is classified as a high-risk breed.

Loss of use coverage, also called additional living expenses (ALE) coverage, pays for temporary housing and basic living costs if your rental unit becomes uninhabitable due to a covered event such as a fire or flooding caused by a neighbor.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.