- Why you should budget in the first place

- How much rent can you afford?

- What other housing costs you need to consider

- One-time fees

- Recurring expenses, aka the stuff you’ll have to pay on the reg

- How to save more money

- Share your space with roommates

- Get your furniture from friendly sources

- Cut the cord

- Save on electricity

- How to budget your income and expenses

- FAQs

Whether you’re moving out of your parents’ place into your first rental apartment or you’re getting ready to sign your umpteenth lease agreement, figuring out how much apartment you can afford can be daunting.

We all know that scary feeling at the end of the month when your account hovers dangerously close to $0 and those dreaded overdraft fees loom large.

Follow our lead to manage your apartment expenses like a pro and never see your account reach $0 again.

Why you should budget in the first place

Signing an apartment you can’t afford is risky, but it’s more common than you think, and the current economic climate can be particularly tricky for renters to navigate. Nationwide, median rents have surged 25% in the past five years, outpacing inflation, which went up 16% during the same period.

Calculating exactly how much you can spend on rent will allow you to begin saving money for your financial goals instead of living paycheck-to-paycheck. It can also help you decide when to start looking for an apartment, based on how financially prepared you are to take the leap.

How much rent can you afford?

The big question surrounding apartment expenses is: How much of your monthly income should you spend on rent?

Ask a traditional financial advisor, and they’ll probably tell you that 30% of your gross income is how much you should spend (gross income is the amount of money you make before deductions like state and federal taxes).

And they’re not the only ones. A quick Google search will reveal a long list of sources telling you to only put down between 25% to 30% of your income on rent. Enter the 30% rule.

Long story short, the 30% mark has its roots in the National Housing Act of 1937. Over the decades, 30% became the general rule for spending on rent, regardless of economic downturns, changes in purchasing power, or national increases in personal debt—rendering it a relatively arbitrary figure.

While 30% may feel like a good rule of thumb, it’s by no means a hard and fast standard. Your financial situation is unique, and what works for someone else won’t necessarily work for you. The rule doesn’t consider permanent expenses and other financial obligations you may have like student loan debt or car loan payments.

Nor does the rule consider the variable costs of living. The amount you’ll pay for a one-bedroom in the hustle-and-bustle of NYC may have you living like a king in a more affordable place like Portland, Oregon.

All this raises the question: if not 30%, how much of your income should you budget on rent?

The short answer – it depends. (Not what you wanted to hear, we know.)

Your rent budget should be contingent upon your financial goals and the amount of money you’ll have after taxes and fixed expenses, something we like to call cash in hand.

So how can you figure out what’s right for you? Start by calculating how much cash in hand you’ll realistically have at the end of the month. Once you get a number, think long and hard about your long-term goals.

Are you aiming to put a lot of money away for the future or live in the moment? Do you plan to buy your own place within the next few years, or are you likely to remain a renter? Either way, there’s a lot you can do to build your nest egg, but you’ll want to think carefully about your unique situation and long-term goals.

No matter what your decision, do not sign on to an apartment that’ll cost you more than the amount of cash in hand you’ll have available at month’s end. It’ll just lead to a situation where you’re overextending yourself, and you’ll wind up in financial trouble.

For more on how to split your earnings between expenses, savings, and leisure, jump to the 50/30/20 rule below.

Btw, to help ensure that you’re paying a reasonable price every month, follow these tips for negotiating your rent.

What other housing costs you need to consider

The bulk of your living expenses will come from your monthly rent check, but there are a handful of additional expenses to consider when creating a budget for your apartment. It’s important to know what to ask when renting an apartment.

One-time fees

- Agent or broker fees: Moving to the big city? If so, you may be surprised at how difficult it is to find an apartment. A real estate agent may help you get a leg-up on the competition – but they don’t come cheap. Clarify the broker’s fee and carefully consider costs before signing on with an agent.

- Moving: Unless you have hordes of friends and family who are willing to move your stuff for free, you’ll need to set some money aside to help finance this endeavor. Start with a moving checklist, decide exactly what you’ll bring to your new digs, and calculate how much it’ll cost to transport everything. Renting a van or truck may seem like a good idea, but if you’re moving heavy furniture or easily-damaged appliances, it may be worth the extra cash to pay professional movers. But, you’ll have to pay for gas and mileage if you go the DIY route, a cost that is often overlooked.

- Security deposit: Most landlords will require some sort of guarantee that you’ll take good care of their apartment in the form of a security deposit. Traditionally, it’s a full month’s rent paid via check, but that’s changing. Some landlords may require you to fork over two months’ rent, especially in big cities like New York and Los Angeles. Here’s your full guide to your renters’ rights, including your obligations with your security deposit.

Recurring expenses, aka the stuff you’ll have to pay on the reg

- Utilities: Factor in costs like electricity, heat, gas, internet, and cable. If you’re a first-time renter, Ask friends and family how much they pay to estimate your utility expenses for the month. If you’re moving to a new city, start by budgeting at least $200 a month for utilities. Check out our complete guide on how to set up utilities when renting.

- Groceries: You’ll have to eat, and food costs money. The USDA publishes average costs of groceries for different populations to help you budget, but account for around $200 to $250 per month to start.

- Public transportation: Assuming you don’t have a car, you’ll need to budget between $80 and $120 for a monthly public transportation pass in major cities.

- Renters insurance: You’ll be stashing lots of stuff you care about (think: laptop, TV, camera, etc.) in your apartment, so it’s smart to protect it from theft, fire, or other bad things – in insurance lingo, called perils – that could happen. Plus, renters insurance coverage helps out with other things like temporary living expenses if your place becomes unlivable, as well as personal liability and medical bills. You can get a policy for as low as $5/mo – worth it!

How to save more money

Any business owner can tell you cutting expenses can have a significant impact on the company’s bottom line. Your bank account is no different; think of your account as its own business entity with an income stream (your salary) and expenses (utilities, rent, food, etc.) that need to be paid.

You can increase the amount of dough left in your account at the end of the month by cutting back and reducing those expenses. Here are some places where you can easily pinch a penny:

Share your space with roommates

The most obvious way to save is by sharing your place with roommates. In most major cities, sharing a two-bedroom apartment with a buddy will be friendlier on your pocketbook than paying for a one-bedroom apartment all to yourself.

Love it or hate it, roommates may be a financial necessity. If you fall into the “hate it” camp, living with other people can be really tough, so we’ve compiled some tips to help you boost your roommate relationship.

Get your furniture from friendly sources

Before rushing to fill your new place with that brand-new couch, complete with a throw pillow and coffee table, take your time and only buy the essentials to start. You likely have less space in your apartment than you think, so if you can avoid the initial temptation to buy that complete IKEA set, you’ll thank yourself afterward.

Slowly acquire furniture that’s functional, serves a purpose, and matches your feng shui. Use your friends and family to source unwanted pieces of furniture they’re willing to get rid of. You’d be surprised at the goodies you can find hidden in basements and attics.

Cut the cord

Cable TV is expensive. Ask yourself if it’s really worth the extra money to pay for cable news, sports, and other channels that you don’t necessarily watch.

Instead, invest in streaming services like Netflix, Hulu, or Amazon Prime. They are significantly cheaper and have a great selection of movies, TV shows, and original content.

When it comes to internet access, it’s common to overpay. Telecom companies are keen on selling you more bandwidth than you actually need, or your building’s infrastructure can really handle. Only pay for the MBs you use.

Pro tip: Buy your wireless router online instead of renting it from the cable company. You’ll get a few good years’ use out of it, which will save you big bucks over time.

Save on electricity

Not paying for electricity isn’t an option (unless you’re ready to give up on just about everything), but there are a few things you can do to lower your bill.

Take practical steps to insulate and winterize your apartment. This will drastically cut your cooling or heating bill since your aircon or heater won’t have to work as hard to keep the temperature comfortable. To take it a step further, look into implementing renewable energy in your apartment.

You should also avoid peak hours when running energy-intensive appliances like your washing machine, dishwasher, or dryer. Instead, use them at night when the electric company has discounted rates for the electricity you use.

How to budget your income and expenses

Once you found a place and settled in, the next pressing question is how to budget for everyday life in your new apartment.

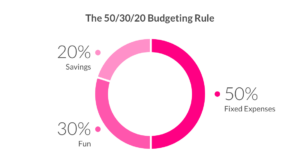

A great rule of thumb is the 50/30/20 rule (not to be confused with the 30% rule above). You can budget your hard-earned income as follows:

- 50% for fixed expenses. This includes rent, bills, insurance, and any loan and debt payments you need to make.

- 30% for fun! This is everything you want but don’t necessarily need, like eating out, going to bars, buying clothes, etc.

- 20% towards savings. It could be contributions to your 401(k) or IRA, or simple deposits into a separate savings account. Anyone say adulting?

To make saving easier, set up recurring transfers from your checking to savings account twice per month (immediately after you get paid). This little trick will force you to budget with your remaining paycheck, and the 20% will feel less significant.

Sidenote: That 20% savings can add up fast, thanks to the wonders of compound interest. If you focus on saving with every paycheck, you’ll have a solid pot of cash by the time you reach retirement age.

The best part about budgeting in 2018 is the ability to keep close tabs on exactly how and where you’re spending your money. All banks and credit card providers can provide a detailed digital statement you can download as a spreadsheet containing all the credits and debits in your account.

Use the spreadsheet to deep-dive into your spending every 30 days, preferably at the end of the month. Sort your expenses into categories and see if you’re spending within the 50/30/20 rule. If you’re not quite hitting the mark, figure out where you need to adjust.

Have spreadsheet-phobia? Don’t fret. There are tons of budgeting apps like Mint, You Need a Budget, and Pocket Guard that make budgeting easy on your smartphone. Some will even link directly to your bank account and help you automatically save and invest.

If you’re looking for other ways on how to split expenses with roommates, try opening a joint bank account or credit card. Use it to pay all of the expenses related to your apartment, including utilities and essentials like cleaning supplies. This way, you can forget chasing down receipts and bills at the end of the month; instead, just pay off the shared credit card since all expenses will be concentrated in one location.

Budgeting is more of an art than a science, and there’s no one right way to manage your money. The key is knowing what you want to get out of your finances and putting your cash to work to meet your goals.

Our number one piece of advice? Don’t overdo yourself. Stay within your limits and don’t overspend. It’s easier to live with less than to struggle to make ends meet because you bit off more than you could chew.

Most importantly, enjoy your new pad and all that comes with moving into your apartment.

FAQs

What percentage of my salary should I spend on rent?

A popular budgeting method is the 50/30/20 rule: spend 50% of your take-home pay on needs, including rent. Ideally, you should keep rent under 30% of your income. However, this can vary by person. To find the amount that is best for you, you can look at your monthly income, subtract fixed expenses like loans and car payments, and use the rest to figure out a reasonable rent amount. If you have a stable job and little debt, you might be able to spend a bit more on rent.

What's a realistic grocery budget for one person?

For one person, a good grocery budget is usually between $200 and $400 per month. This depends on where you live, what you eat, and how you shop. Cooking at home and choosing less expensive items can help keep costs down.

How can I reduce my monthly housing costs?

To save on housing, you can get a roommate, move to a cheaper area, or find a smaller place. Renting out extra space, doing tasks for your landlord, or joining a home-sharing program can also help lower your costs.

Should I factor in renter's insurance when budgeting for housing?

Yes, you should include renter’s insurance in your budget. It’s usually affordable (around $10-$30 per month) and protects your belongings and liability in case of theft, fire, or damage.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage and discounts may not be available in all states.

Share