Landlords: Here’s Why Your Tenants Should Get Renters Insurance

And why you should include it as part of your lease!

And why you should include it as part of your lease!

Renting out your property to tenants can be a hassle, and often involves thorough screening of potential renters and checking off tasks on a never-ending to-do list. The phone calls, back and forth paperwork, and overall bureaucracy involved with leasing out your place to temporary tenants is a minor headache, at best.

That’s why making sure your tenants are fully protected with their own HO4 insurance policy is a no-brainer. In fact, you probably should make your tenants’ insurance mandatory in your leasing agreement – that way, you can increase the coverage on your rental, and lower your costs in the long term. Think of it as another line of defense when there’s an emergency situation.

When your tenants have their own insurance policy, it’s an additional layer of protection for you, the landlord. When unfortunate things like fire cause damage to your place, their renters insurance policy can help repair the damage, reducing the amount you or your insurance company have to pay.

This keeps your own policy premium lower by reducing the claims on your insurance, and helps you avoid costly legal fees. And not to mention, it saves you a ton of time!

In addition, renters insurance will help keep your relationship with your tenants healthy, especially when a major damage or loss occurs. With renters insurance, you can avoid disputes over who has to cover costs of damages.

Oh, and one more perk: Tenants with renters insurance are less likely to sue you to compensate them for a loss. In fact, a survey by Joshua Tree Consulting estimated that landlords in large properties juggle eight ‘nuisance’ insurance claims per property each year.

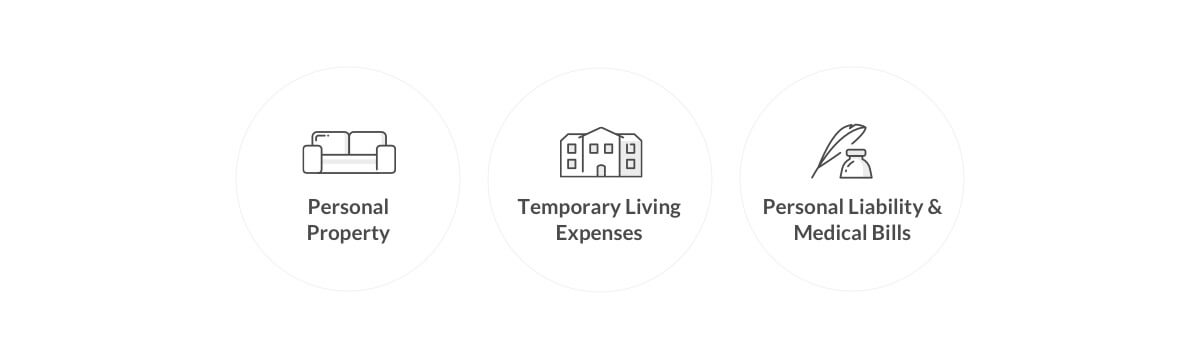

If your tenants choose to purchase a renters insurance policy, they will get three main coverages: personal property, temporary living expenses (also called ‘loss of use’), and personal liability & medical bills.

We’ll break down what each of these coverages mean for you, and your tenant.

Tenants tend to think that since they don’t own the place, they don’t need extra protection for their stuff. That’s a very common mistake, and it’s important the tenants know they won’t be covered if a kitchen fire damages their stuff, or their laptop is stolen. Your landlord insurance doesn’t cover the tenant, or the tenant’s stuff.

Imagine this: a mysterious fire causes extensive damage to your building, displacing your tenants and damaging their stuff. Not only would this cost your uninsured tenants serious $$, but they would also likely need to blame someone for this incident, and that blame may fall on you.

In cases like these, your tenants’ renters insurance policies can come to your rescue. It can help pay for your tenants’ temporary living expenses, reimburse them for their lost items, and reshift the focus from you, to your tenants’ insurer.

Let’s be real: There are many situations where personal liability coverage for tenants comes in handy – say, your tenant hosts a party and someone slips and falls, or their neighbor comes over to help make dinner and cuts their finger while chopping the salad. According to the Insurance Information Institute, average renters liability claims range from $15,000 to $30,000, and serious accidents can easily surpass $100,000.

Renters insurance policies include liability and medical payments to others, so if someone claims to be injured due to your tenant’s actions or negligence, their renters insurance may cover legal fees and may also pay to cover damages they’re found liable for.

If it’s something small (read: under $5,000), their medical payments to others coverage will kick in, but if someone decides to take some unfriendly steps and sues your tenant, their personal liability coverage will have their back.

Liability coverage can make a huge difference when legal bills and medical fees start racking up! So if your tenant unfortunately caused damage not only to your home, but to other units in the building, they’ll be in a costly bind.

No one wants a bunch of insurance companies chasing them for damages they caused. Your tenant will thank you for making them get their own tenant liability insurance.

Making renters insurance mandatory for your tenants doesn’t have to be a deal-breaker.

Here are some of the benefits of renters insurance you should make sure your tenant understands:

A common misconception about renters insurance is that it’s pricey, so communicate to your tenants that the average cost of renters insurance is probably lower than expected and that a very basic renters insurance policy can cost as little as $5 a month (thanks to the help of AI)! Most policies allow you to customize your coverages to fit your lifestyle needs, so renters insurance doesn’t have to be a significant out-of-pocket expense.

For example, if you have Lemonade, you can adjust this amount at any time with the Live Policy feature, and choose how much coverage you’d like, which in turn will influence your monthly premium (the amount you pay each month for your renters insurance policy).

A renters policy may cover others living with your tenant, too! If your tenant is living with anyone related to them by blood, marriage, or adoption, they’ll automatically be covered by the tenant’s renters insurance policy. They’ll just have to make sure to get enough coverage for everyone.

They can determine just how much coverage they need when they add other people to their policy. If they’re living with their significant other, they’ll need to be added to the policy as what’s called an ‘additional insured.’

FYI – roommates aren’t covered by a typical renters insurance policy. You’ll have to tell them to get their own!

If your tenant has a dog, and you were wondering, “does renters insurance cover dog bites?” you’re in luck. If your tenants’ dog bites someone, their policy has them covered.

The cool thing about this one is it applies both when they are at home or at the park. There are two exceptions though: They’re typically not covered if the dog has a history of biting, or if the dog is categorized as high-risk or “vicious.”

And that’s just a part of the benefits of renters insurance for your tenants. You can be an even better landlord if you help them figure out how much renters insurance costs. Everyone’s lifestyle is different, so be sure to help ‘em figure out what kind of coverages their lifestyle requires.

Part of figuring out how much coverage your tenants need is determining how much their stuff is worth. It’ll help them ensure their coverage amounts reflect the real value of their stuff.

Some states allow you, the landlord, to require tenants to purchase renters insurance as long as this requirement is in place for all tenants. A national survey conducted by Satisfacts found that nearly 85% of the owners requiring insurance described the impact as positive or neutral, and 91% said the administrative burden has been “easy” or “manageable.”

What’s even easier at Lemonade is that your tenant can seamlessly add your email address to the policy, and you’ll be automatically notified if their policy ends for any reason.

And to take it a notch further: As a landlord, you can pay your tenants’ policy for them, and include the cost of it in their rent. That way, everyone is 100% covered.

But if you’re not up to making it mandatory in the rental agreement, try to explain why renters insurance is always a good idea.

Often, it’ll be a decision that will be postponed time and again – turns out, our brain rationalizes this by saying, “I don’t really need it now.” But that rationalization often changes when disaster strikes – in other words, when it’s too late to get covered.

Knowing how our brain rationalizes insurance decisions will help us understand why we should protect ourselves now for something that may or may not happen later.

Having both the landlord and tenant insured with the same insurance carrier could make your life easier. With Lemonade, your tenants can get insured in seconds, change and update their coverages instantly through the Lemonade app, and get their claims handled in minutes. And you, the landlord, can get a rental property insurance policy (also referred to as a landlord insurance policy). It’s currently available for condo/co-op owners in NY, IL, PA, DC, and NJ, who rent out their property less than 5 times a year.

Your tenants will thank you, their landlord, and you’ll have your own peace of mind.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.