- Does having a trampoline make you ineligible for homeowners or renters insurance coverage?

- Does renters or homeowners insurance cover trampolines?

- What part of the insurance policy applies to your trampoline?

- What are some ways to prevent trampoline injuries?

- Okay, you convinced me. I’m getting rid of this trampoline. But now I’m sad.

- Which states currently offer homeowners insurance?

So, you have homeowners or renters insurance, and you also have something fun but potentially dangerous: a trampoline!

Perhaps you’ve got kids who love jumping, flipping, and goofing off on a summer day. Perhaps you have nostalgic memories of your own childhood aerial antics, and find that it’s an excellent form of stress relief during these pandemic days. But how can having a trampoline on your property affect your policy? And is there even such a thing as trampoline insurance?

After all, part of your policy includes liability coverage if there’s an accident in your home or on your property… but depending on your insurer and where you live, having a trampoline on the premises might create some small complications.

Let’s jump right in, shall we?

Does having a trampoline make you ineligible for homeowners or renters insurance coverage?

Not necessarily. But in certain cases, it might be one factor (of several) that leads underwriting to a decline decision.

Even if your trampoline doesn’t prohibit you from acquiring a home or renters insurance policy, it’s possible that certain losses pertaining to it might not be covered. We call this a ‘trampoline exclusion.’

Does renters or homeowners insurance cover trampolines?

At Lemonade, we generally remove liability coverage as it pertains to trampolines, based on the inherent danger and high risk involved. (FYI, the same rule of thumb applies to other entertaining-but-dicey contraptions like bounce houses and inflatable slides.) What does that mean? Well, in most cases, if someone breaks a leg while trampolining, or otherwise damages their belongings, it will not be covered.

If your trampoline is unsecured and a strong wind sends it flying into your neighbor’s yard, where it smashes into their Volvo… sorry, you’d be out of luck. In this regard, consider it to be a classic case of TAYOR (Trampoline At Your Own Risk).

This doesn’t mean, though, that your trampoline itself isn’t covered, as a piece of property that you own. So if an oak tree in your backyard collapses during a storm, and smashes the trampoline into pieces—your policy would likely compensate you for those damages.

Different insurance companies likely have different policies, though—so if you’re not sure, just ask your insurer. And as always, take the time to carefully and closely read your own policy!

(And hey, if you’re curious about coverages in general, we’ve got a lot more info about what renters insurance does and doesn’t cover, as well as a similar recap of what home insurance covers.)

What part of the insurance policy applies to your trampoline?

Even if your trampoline is enormous and seems like a permanent structure, it’s not considered as part of “Other Structures”—that pertains to things like in-ground swimming pools or free-standing garages.

Your trampoline would be included under the umbrella of personal property coverage, aka Coverage C. That means it’s protected against specific named perils—things like fire, lightning, windstorms, vandalism, and theft.

What are some ways to prevent trampoline injuries?

The easiest way to prevent trampoline injuries is to avoid jumping on a trampoline. (Thanks, mom.)

But if you just can’t get enough of that bouncy, bouncy goodness—even if it might mean an unexpected trip to the emergency room—there are certainly a few best practices to follow.

First of all, strap the trampoline down securely to the ground so it can’t shift unsafely or become unmoored. Install a safety net around the trampoline, and put a lock on the net. Don’t mess around with any additions that will make the trampoline more exciting, but also much less safe (trampoline sprinklers look like a blast, but…please).

Don’t situate the trampoline anywhere near a pool, no matter how fun it might seem to launch yourself into the deep-end after one too many White Claws. (WHAT WOULD YOUR MOTHER SAY?!).

Trampoline safety isn’t just about you and your immediate family, either. Consider having a proper locking gate around the trampoline, like you should have around any in-ground or above-ground swimming pool.

That way, your trampoline won’t become an attractive nuisance—a tempting and dangerous thing that thrill-seeking neighborhood youths are powerless to avoid, like tree houses or diving boards. The more safety precautions you put in place around your trampoline, the fewer medical bills and trampoline accidents you’ll have on your hands.

Okay, you convinced me. I’m getting rid of this trampoline. But now I’m sad.

We hate to be a buzzkill, we really do. We live for thrills! Some of us grew up going to Action Park every summer, and it’s amazing we’re still here to tell the tale!

If you or your kids are jonesing for an occasional hit of trampoline, see if there’s a trampoline park in your area. It might not guarantee that you won’t have trampoline accidents, but at least you’ll be jumping in a somewhat controlled environment.

Or you can always play it super, super safe, and live vicariously through the world of extreme trampolining on Instagram. Zero emergency room visits, zero stress, and zero safety precautions required! Your insurer (and your pediatric doctor) will thank you.

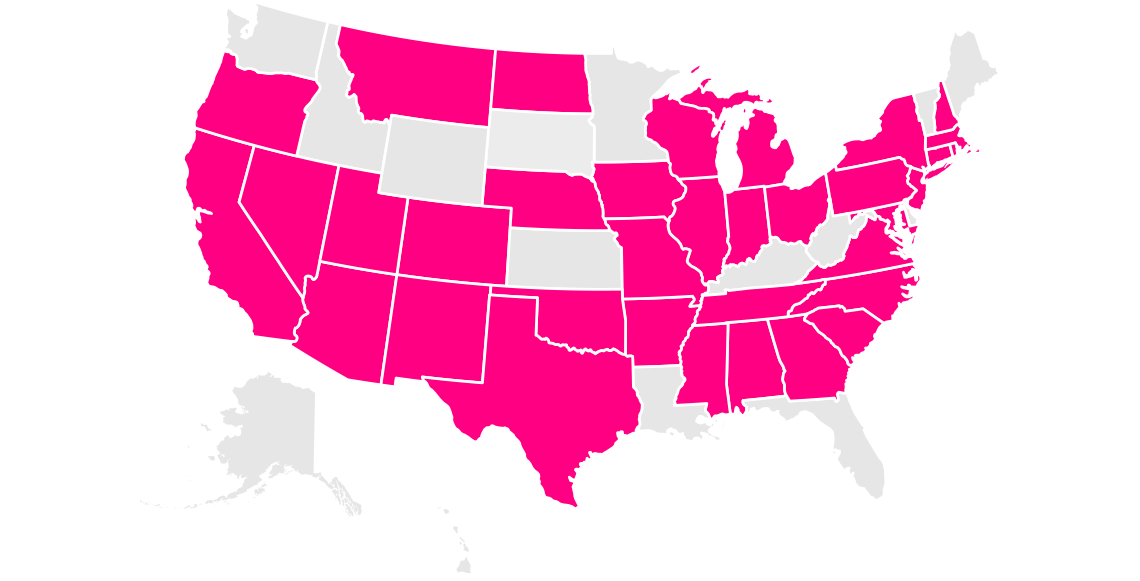

Which states currently offer homeowners insurance?

Arizona, California, Colorado, Connecticut, Georgia, Illinois, Indiana, Iowa, Maryland, Massachusetts, Michigan, Missouri, Nevada, New Jersey, New York, Ohio, Oklahoma, Oregon, Pennsylvania, Tennessee, Texas, Virginia, Washington, D.C. (not a state…yet), and Wisconsin.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage and discounts may not be available in all states.

Share