How Much Is Renters Insurance in 2026?

Hint: Renters insurance costs much less than you think.

Hint: Renters insurance costs much less than you think.

The average cost of Lemonade renters insurance across the U.S. is around $16/month with prices starting as low as $5/month, as of January 2026.*

Meanwhile, the average cost of renters insurance in the U.S. is around $23/month* as of 2026.

Although the cost of renters insurance is generally quite affordable, prices can vary depending on a number of factors, including your rental’s location, your deductible, and your coverage and limits.

TL;DR

TL;DR

Here are some average renters insurance prices across the U.S., as of 2026. These include rates from various insurers, not Lemonade specifically.

| State | Average renters insurance price per month in 2026 |

|---|---|

| Alabama | $31 |

| Alaska | $22 |

| Arizona | $27 |

| Arkansas | $35 |

| California | $19 |

| Colorado | $24 |

| Connecticut | $18 |

| Delaware | $18 |

| Florida | $27 |

| Georgia | $33 |

| Hawaii | $22 |

| Idaho | $20 |

| Illinois | $23 |

| Indiana | $25 |

| Iowa | $21 |

| Kansas | $24 |

| Kentucky | $24 |

| Louisiana | $36 |

| Maine | $17 |

| Maryland | $23 |

| Massachusetts | $18 |

| Michigan | $30 |

| Minnesota | $20 |

| Mississippi | $32 |

| Missouri | $28 |

| Montana | $16 |

| Nebraska | $21 |

| Nevada | $22 |

| New Hampshire | $17 |

| New Jersey | $18 |

| New Mexico | $22 |

| New York | $19 |

| North Carolina | $17 |

| North Dakota | $16 |

| Ohio | $28 |

| Oklahoma | $31 |

| Oregon | $21 |

| Pennsylvania | $21 |

| Rhode Island | $20 |

| South Carolina | $20 |

| South Dakota | $21 |

| Tennessee | $24 |

| Texas | $25 |

| Utah | $24 |

| Vermont | $17 |

| Virginia | $20 |

| Washington | $17 |

| West Virginia | $19 |

| Wisconsin | $20 |

| Wyoming | $16 |

Here are the factors that can determine how much you pay for renters insurance.

The state, city, and even neighborhood you reside in may affect your renters insurance rate. If you live on the coast, you may be more likely to encounter extreme weather and appear riskier to your insurer. The same goes if you live in an area with higher rates of theft, burglary, vandalism, or other covered perils. As an insurance rule-of-thumb, the more likely you are to file a claim, the more your renters insurance will cost.

But your location could also help lower your price! For example, living around the corner from a fire station could help bring costs back down.

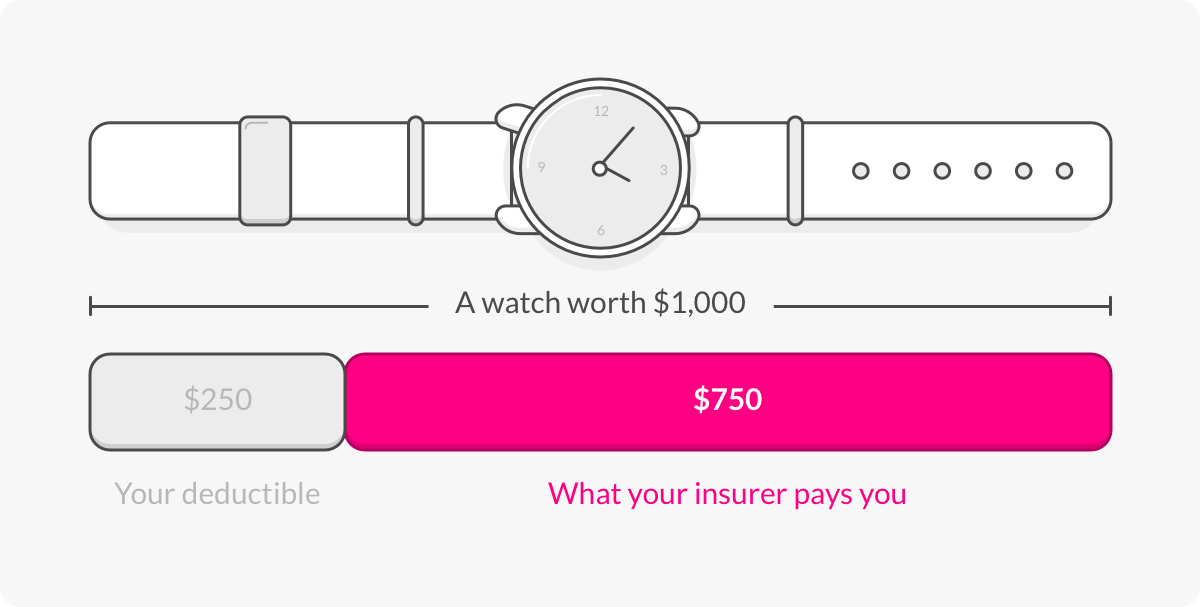

An insurance deductible is the part of the claim that the policyholder retains responsibility for that will be subtracted from any future claims payouts. So if your $1,000 watch were stolen, and you had a $250 deductible, your insurance company would pay you $750.

Think of a deductible as your participation in a covered loss. You’re saying, “I commit X dollars to any claim, and my insurance company will pay the rest of the covered amount.”

Generally speaking, the higher your deductible, the lower your premium. But keep in mind that a higher deductible also means you’ll pay a lot more out of pocket in the event of a claim. At the end of the day, it depends on how much you’re comfortable with paying out of pocket in the event of a claim.

If your claims history is pretty extensive, your premium could be higher since people who’ve filed a lot of claims in the past are statistically more likely to file more claims in the future.

Lower credit scores are also statistically linked to more claims, so, depending on the laws and regulations where you live, a lower credit score could lead to a higher premium. On the other hand, good credit could help you land a better rate by demonstrating to your insurer that you’re a lower risk.

The amount of coverage you choose in each category-like loss of use, personal property, and liability coverage- impacts the final price of your premium.

At Lemonade, a basic renters insurance policy starts at $5/month and includes $10,000 of personal property coverage. However, the $5 minimum will vary depending on the state and risk characteristics where you live. But if, for instance, you decide that your personal belongings are worth closer to $30,000, then you’ll pay more than if your stuff were worth just $10,000.

Different providers will offer different coverages, deductibles and rates, so it’s best to shop around and compare quotes before settling on a policy. While it might be tempting to go with the lowest rate, you also want to pick a provider that meets all of your unique coverage needs. Here are some tips for finding the best renters insurance for your circumstances and your budget:

Even though renters insurance premiums are already quite affordable, there are still some ways to make yours even lower. Let’s look at some options.

If your apartment has some basic security devices, like a fire alarm and a burglar alarm, be sure to let your insurer know. Since these devices mitigate the possibility of future losses, you could qualify for a discount.

Some insurers might offer you a discount if you choose to buy more than one insurance policy with them. Bundling your renters policy with other Lemonade products, such as pet insurance or car insurance, could save you money on your insurance costs.

As we mentioned above, you have may have the ability to adjust your premium based on the deductible and coverage amounts you opt for. Increasing your deductible and reducing your coverage amount are straightforward ways to lower your premium. However, we recommend that you proceed with caution before making any drastic changes. You don’t want to end up in a situation where you’re denied coverage for something essential, like the costly replacement of your furniture in the event of an apartment fire.

And, if you opt for a higher deductible, just make sure that it’s still an amount you’re comfortable paying out of pocket in the event of a claim. (BTW, here are some handy tips for choosing a deductible on your renters insurance.)

Don’t forget: You can make any changes to your policy directly through the Lemonade app without doing any paperwork.

As we already mentioned, a typical renters insurance policy covers three main areas:

If you want to take a deeper dive into the topic, here’s more on what renters insurance does and doesn’t cover.

In order to determine how much renters insurance you need, you should weigh how much you think you need in terms of your belongings and lifestyle against how much you think you can pay monthly. Picking a higher coverage amount will push up your monthly premiums slightly, but on the other hand, you don’t want to be left without the right amount of coverage in the worst-case scenario.

If you’re not sure how much your stuff (ie., your personal property) is worth, look around your apartment, and mentally calculate the value of everything. Think about clothing, furniture, and electronics, but don’t forget about the stuff outside of your home, like your bicycle or that old box of stuff you keep forgetting to clear out of your car.

| Min | Max | |

|---|---|---|

| Personal property | $10,000 | $250,000 |

| Personal liability | $100,000 | $500,000 |

| Loss of use | $3,000 | $200,000 |

| Medical payments | $1,000 | $5,000 |

As you tally, think about the value of your stuff in increments of $10,000 since those are the increments of our coverage limits. So, if you have $18,000 worth of items, you should pick around $20,000 of personal property coverage.

Standard policies start with $10,000 of personal property coverage. But you should decide based on the value of your own stuff.

Keep in mind too that if you have any high-ticket items, like a diamond ring or a Sony a7S III camera, you might want to purchase additional coverage for each item. This is known as scheduled personal property coverage, or ‘Extra Coverage,’ as we call it at Lemonade.

Still not sure what coverage amount is right for you? Check out our easy guide to figuring out how much renters insurance you need.

While the average price of renters insurance across the U.S. is $23/month, Lemonade renters insurance rates are quite competitive at an average of just $16/month.

But let’s be clear: Affordable doesn’t have to mean cheap or unreliable. We’re able to offer such reasonable rates at Lemonade because we use AI and machine learning. AI Maya handles all of our basic customer inquiries, which means we have lowered overhead. But our use of AI doesn’t mean we’ve lost the human touch or forgotten the value of personalized interactions. With Maya taking the lead on the easy stuff, our (human) support team is free to handle your trickier insurance questions, like how to replace a lost engagement ring.

Renters insurance generally costs less than home insurance because it only covers the personal belongings and liability of renters, not the structure itself. Home insurance, on the other hand, includes coverage for the home’s structure in addition to personal property and liability, which makes it more expensive.

The cost of renters insurance varies by state due to factors such as regional risk levels, local crime rates, weather patterns, and overall cost of living. States with higher risks of natural disasters or higher property values typically have higher insurance costs.

Yes, because they require higher coverage limits to fully protect them. Adding Extra Coverage (aka scheduling personal property) for these valuable items will raise your premium to ensure they are adequately covered.

A lower credit score may lead to a higher renters insurance premium because it’s associated with a higher risk of claims. Conversely, a higher credit score can help reduce your premium by demonstrating lower risk

Yes! Lemonade offers discounts when you bundle renters insurance with other policies. You can save by combining renters and car insurance into one convenient package, or add pet insurance to protect your furry family members. Bundling not only saves you money but makes managing your coverage way simpler.

Renters insurance can start as low as $5/month, but your actual rate depends on where you live, how much coverage you want, your deductible, and your claims history. A renter in rural Ohio pays less than someone in a Manhattan high-rise. The only way to know your real number is to get a quote. At Lemonade, getting a quote can take as little as 90 seconds and gives you an actual figure instead of a guess. Read the full thread on Reddit

It varies a lot. A basic policy in a small city costs less than a higher-limit policy in NYC or LA. What your neighbor pays tells you almost nothing about what you’d pay. At Lemonade, getting your own quote can take as little as 90 seconds. It’s the only number that actually matters for your situation. Read the full thread on Reddit

For personal property, most renters find that somewhere between $15K and $50K covers most typical personal belongings.¹ Think through what it would actually cost to replace your furniture, clothes, electronics, and other covered property. For liability, $300K is a common starting point,² and higher limits usually don’t cost much more while giving you significantly better protection if someone gets hurt and sues. Your deductible is typically subtracted from most claim payouts, so it’s worth factoring in when you’re choosing your limits. At Lemonade, you can adjust both during the quote to find what fits your situation. ¹ Based on typical personal property coverage ranges recommended for renters. Your actual coverage needs may vary. ² $300K is a commonly recommended liability limit for renters. Your individual needs may differ. Read the full thread on Reddit

NYC rates vary a lot. A Manhattan high-rise looks different from a Brooklyn walk-up. Your building’s age, security features, neighborhood, and coverage limits all factor in. What someone else pays in NYC tells you almost nothing about what you’d pay. At Lemonade, getting a quote for your specific address can take as little as 90 seconds for an actual number. Read the full thread on Reddit

Most renters go with $300K. It doesn’t cost much more than $100K, but if someone gets seriously hurt and decides to sue, medical bills and legal fees add up fast. The extra coverage is usually worth the small premium difference. At Lemonade, bumping up your liability limit is a quick adjustment during the quote process. ² $300K is a commonly recommended liability limit for renters. Your individual needs may differ based on your personal circumstances and risk profile. Read the full thread on Reddit

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.